Financial RSS Feeds

https://www.investing.com/rss/news.rss

https://cointelegraph.com/rss

Crypto traders usually view negative funding rates as a buy signal, but this week’s volatility US earnings outcome may cloud the value of the signal for ETH investors.

The enforcement action over wagers on sports event contracts followed Coinbase announcing the launch of prediction markets in all 50 US states.

https://www.coindesk.com/arc/outboundfeeds/rss/

https://cryptobriefing.com/feed/

Yearn Finance highlights the urgent need for better risk management as DeFi faces growing challenges.

The post Corn: DeFi faces critical customer support challenges, Yearn’s foresight on UST highlights governance risks, and the market is set for recovery in late 2023 | On The Brink with Castle Island appeared first on Crypto Briefing.

2025 is set to be a game-changing year for blockchain, with explosive growth in digital wallets and investments.

The post Matthew Le Merle: 2025 will be the year of crypto equity, hundreds of millions will adopt digital wallets, and US regulation is shifting positively | On The Brink with Castle Island appeared first on Crypto Briefing.

https://bitcoinist.com/feed/

Tether, the company behind the dominant stablecoin USDT, has put a full Bitcoin mining operating system out in the open. The software, called MiningOS or MOS, is available under an open-source license and aims to let miners run, monitor, and scale rigs without paying for closed vendor platforms.

MiningOS Brings A Modest, Practical Toolkit For Miners

Reports note MiningOS is designed as a modular, self-hosted stack that works from single-rig setups to large sites. It bundles device management, telemetry, energy controls, and developer hooks so operators can mix and match the pieces they need.

The code is open under the Apache 2.0 license and the project publishes docs and a GitHub-style workflow for community fixes and feature requests.

Tether

Bitcoin

Tether Mining OS is now fully opensource.

A complete operational platform that can scale from a home setup to industrial grade site, even across multiple geographies.

Super modular, P2P encrypted networking layer. It supports a long list of miners,… https://t.co/VzXywA6IZc

— Paolo Ardoino

(@paoloardoino) February 2, 2026

A Peer-To-Peer Backbone, Not Another Cloud Service

Tether says MOS uses Holepunch peer-to-peer networking so devices can talk directly to one another. That means fewer central servers and no forced dependence on a single provider.

The design is meant to avoid vendor lock-in and to give miners full control over their data and operations. Independent outlets covering the launch highlighted those points when describing how MOS differs from many commercial mining platforms.

Why This Could Matter To Small Operators

Bitcoin Mining is complex.

Mining OS by Tether (MOS) makes it simple.

Introducing MOS — the open-source operating system for real mining infrastructure.

Modular. Scalable. Built for energy + hardware + data.

Explore the Documentation: https://t.co/3zcBHFFzRp Join our… pic.twitter.com/G0GwbtfLKT

— Tether (@tether) February 2, 2026

Many small operators struggle with the cost of managed platforms and the extra complexity when hardware, power systems, and telemetry come from several vendors.

Reports say MiningOS aims to lower that barrier by offering a free, extendable base that communities and integrators can adapt. That could make it easier for hobbyists and emerging miners to run efficient setups without buying expensive licenses.

According to Tether’s announcement, the project is led internally and presented by company leaders at recent Bitcoin gatherings where miners and builders meet.

Paolo Ardoino, Tether’s CEO, has been named among the public faces explaining the initiative, and the firm has tied the launch to broader efforts to support open infrastructure around Bitcoin.

Featured image from Verdict, chart from TradingView

Ripple says more than AED 1 billion (over $280 million) of certified polished diamonds held in the United Arab Emirates have been tokenized on the XRP Ledger, in a deal that ties a high-value physical inventory to on-chain issuance, custody, and (eventually) secondary-market rails.

The initiative, announced Tuesday by Billiton Diamond and Ctrl Alt, is pitched as an end-to-end tokenization effort for certified polished diamond inventory in the Dubai market, one that is designed to make provenance, grading, and ownership history verifiable before a transaction, while compressing settlement and operational workflows that have historically relied on offline certification and paper-heavy transfer processes.

XRP Ledger Powers Dubai Tokenization Push

According to the companies’ press release, Ctrl Alt has already tokenized more than AED 1 billion in diamonds, with tokens minted on the XRP Ledger. The partners said the network was selected for “fast settlement, low fees, and scalable architecture,” while the tokenized assets are secured through Ripple’s “enterprise-grade custody technology.”

Reece Merrick framed the move as a proof point that custody and auditability are central to institutional-grade commodity tokenization. “This initiative shows how Ripple’s technology can bridge the gap between physical assets and the digital economy, utilising our enterprise-grade custody solution to secure high-value diamond assets with unrivalled trust and security,” Merrick wrote on X.

He added that the firms were “providing the infrastructure needed to move physical commodities on-chain at scale,” calling it “a significant leap forward for the future of commodities tokenization.” Notably, the firms first announced their partnership in July last year.

Billiton, which the release describes as a leader in rough diamond auctions using a Vickrey auction model, said the collaboration is intended to expand into tokenized polished diamond sales phases. The planned platform would embed real-time inventory management and certification data on-chain, enabling verification of origin, grading, and ownership history before trades.

The firms also pointed to future “secondary market readiness” workstreams: custody, transfer, and market participation, implying the tokens are being structured not just as a digitized record, but as infrastructure for distribution.

The press release said the next stages are subject to regulatory approval by Virtual Assets Regulatory Authority (VARA) prior to launch. That detail matters: the partners are explicitly positioning the effort as compliant market infrastructure, not a one-off proof of concept.

Jamal Akhtar argued the core unlock is liquidity and time-to-cash in a market where diamonds have traditionally been operationally complex to finance and transfer.

“This partnership transforms polished diamonds from a traditionally illiquid asset class into a transparent, investable digital asset that supports manufacturers, brands, and investors alike,” Akhtar said. “Tokenization introduces an unprecedented level of transparency, unlocking the potential for new liquidity, shortening working capital cycles for manufacturers and traders, and opening the door to seamless global participation in Dubai’s growing luxury ecosystem.”

The announcement also credits DMCC with connecting stakeholders and helping build the ecosystem for diamond tokenization, with Ahmed Bin Sulayem describing DMCC as a “bridge between commodities, capital and next-generation digital markets,” and pointing to coordination with VARA as part of the framework underpinning the rollout.

Ctrl Alt’s Robert Farquhar said: “Billiton needed robust, institutional-grade infrastructure to handle the complexity and scale of its polished diamond supply. Our proven tokenization expertise and technology provide a clear, secure, and compliant route for diamond ownership to move on-chain, from asset origination to digital market participation. This establishes a more accessible and operationally efficient model for commodity investment in the UAE.”

At press time, XRP traded at $1.60.

https://cryptoslate.com/feed/

Bitcoin is a $1.5 trillion prize pool secured by nothing more than numbers, private keys, generated by math, that unlock wallets holding real money.

That’s the seductive idea behind Keys.lol: a site that spits out batches of Bitcoin private keys and their corresponding addresses, like an infinite roll of digital lottery tickets.

Refresh the page, and you get another set. Refresh again, and you get another.

Somewhere in that endless stream is a key that matches a wallet with a balance, maybe even one holding a life-changing amount.

This is the only lottery where the game is real, and the jackpot exists, yet the odds are so extreme that “never” is the practical outcome.

The keyspace is so vast that even checking billions of addresses at a time doesn’t meaningfully move the needle; the chance of landing on a funded wallet is so close to zero that it effectively disappears.

Keys.lol feels like a shortcut to fortune, but what it actually demonstrates is the opposite: why Bitcoin wallets are secure, and why brute-force “guessing” isn’t a threat model so much as a lesson in how big numbers can get.

How to play the free Bitcoin lottery

Open the website. Hit refresh. Watch it spit out a new batch of 90 Bitcoin private keys and addresses, like scratchcards scrolling past at high speed.

It feels like a loophole in reality: if you can generate enough keys, fast enough, surely you’ll eventually land on one that already controls real BTC.

That temptation is exactly what Keys.lol is built to dramatize. The homepage claims “every Bitcoin private key” is on the site and encourages you to “try your luck.”

But the punchline is mathematical: yes, you can play, and no, you can’t win, at least not in any practical sense.

I'm not trying to advertise how to “hack Bitcoin.” It’s the opposite: a fun, slightly mind-melting way to understand why Bitcoin wallets are secure.

The space of possible keys and addresses is so large that “randomly guessing” is effectively impossible.

An unintended side effect is that refreshing for long enough may well cure your gambling addiction, too. The fun goes from “but what if I hit one?” to “yeah, this is impossible” pretty quickly.

Keys.lol turns keyspace into a game

Keys.lol doesn’t store a literal database of keys (that would be physically impossible). It generates keys procedurally on the fly based on a page number.

That means it can display deterministic slices of the keyspace without ever saving them.

In other words: it’s not a vault of stolen secrets. It’s a number generator with a balance checker and a casino vibe.

And if you’re refreshing random batches, say 90 addresses at a time, you’re essentially buying free lottery tickets against the entire Bitcoin address universe.

The math behind the impossible odds

A Bitcoin private key is basically a number in an astronomically large range. Keys.lol itself describes it as between 1 and (2^256).

But for this “lottery,” the practical target is addresses with a non-zero balance.

As of February 2026, there are 58 million BTC addresses with a non-zero balance. Let’s use that as the “number of winning tickets.”

Now compare it to the size of the space you’re sampling from.

A standard way to think about Bitcoin addresses is that they’re derived via hashing to a 160-bit value.

- (2^160) possible address-hash outcomes

- That’s about 1.46 × 10^48 possible destinations for “where BTC could be,” in address-space terms

Even if tens of millions are funded, that’s still a rounding error against 10^48.

So what are the odds per refresh?

If you sample addresses uniformly at random from the full space, the probability a single random address is one of the 58,000,000 non-zero ones is:

- p = 58,000,000 / 2^160 ≈ 3.97 × 10^-41

If you check 90 addresses in one go, your chance of finding at least one non-zero balance becomes:

- P(≥ 1) ≈ 90p ≈ 3.57 × 10^-39

That’s roughly:

- 1 in (2.8 × 10^38)

Written out, that’s:

1 in 280,000,000,000,000,000,000,000,000,000,000,000,000,000 (“280 undecillion.”)

A human way to feel “1 in 2.8×10^38”

Try this mental model:

Imagine you could do one billion refreshes per second (and each refresh checks 90 addresses).

The expected time to hit just one non-zero address would still be on the order of 10^12 years.

The age of the universe is ~10^10 years.

That’s about 10^12 times the age of the universe, or a trillion universe-lifetimes just to find a single funded address.

So you’re not “unlikely” to win. You’re functionally guaranteed not to on any timescale that matters.

How much harder than winning the lottery?

The EuroMillions jackpot odds are about 1 in 139,838,160; the US Powerball odds are 1 in 292,201,338.

Keys.lol's “90-address refresh finds a funded wallet” odds are about 1 in (2.8 × 10^38).

So EuroMillions is roughly:

- (2.8 × 10^38) / (1.398 × 10^8) ≈ 2 × 10^30

That’s about two nonillion times more likely than your refresh ever finding a non-zero address.

Put differently: you’d have a better chance of winning EuroMillions again and again and again than hitting a funded BTC address by random key generation.

This is why Bitcoin wallets are secure

The entire security model of Bitcoin ownership is built on one simple idea:

Even if everyone on Earth used every computer they could possibly build, guessing someone else’s private key is still computationally and probabilistically out of reach.

Keys.lol is compelling because it makes the impossible feel tangible. You’re looking at real-looking keys and real-looking addresses and hoping for a miracle.

But Bitcoin doesn’t rely on secrecy through obscurity. It relies on the sheer scale of the keyspace.

The “attack” you’re simulating, random guessing, isn’t a threat model. It’s a lesson in large numbers.

If you ever “hit” a funded key, it’s theft, not a free jackpot

There’s a reason this “free Bitcoin lottery” is such a useful teaching tool: it exposes the difference between possible in theory and permissible in real life.

If you were to generate a private key that corresponds to a wallet with funds, and then try to “sweep” those coins, you wouldn’t be claiming abandoned treasure.

You’d be taking assets you don’t own, without consent. In plain terms: it’s theft.

Even framing it as “luck” doesn’t change what’s happening. The private key is simply the credential that proves control.

Discovering someone else’s credentials doesn’t grant you ownership any more than finding a stranger’s bank card PIN would.

And there’s a second, subtler risk: trying to turn this into a get-rich scheme can expose you to legal consequences.

Whether it’s prosecuted as theft, fraud, unauthorized access, or another offense depends on the jurisdiction. But the core point is the same: “I guessed it” is not a defense, and “finders keepers” doesn’t apply to digital property.

So yes, Keys.lol is a fascinating window into Bitcoin’s security model. But the only “win condition” here is understanding the math, not trying to cash out someone else’s balance.

“Mathematically never” is still annoying for bots, so Keys.lol adds friction anyway

Even though the odds of finding a funded wallet are so tiny they round to zero for any practical human timeline, Keys.lol still throws up bot protection.

Click “Random page” too aggressively, and you can be redirected to an “Are you human?” captcha.

In other words: even the site itself assumes someone, somewhere, will try to automate refreshes at scale, and it actively tries to slow that down.

That doesn’t make Bitcoin “more secure” (the security comes from the size of the keyspace). But it does make this particular game harder to industrialize.

It’s a reminder that brute-force behavior is expected, and throttled, even when the underlying math already makes success effectively impossible.

The “expected reward” of a refresh (and why the fun math is misleading)

Let’s do some back-of-the-napkin maths anyway.

The average non-zero wallet holds about 0.126 BTC, and we can value that at roughly $9,852 today, then the arithmetic is:

- $9,852 ÷ 58,000,000 ≈ $0.0001362069

- That’s about $1 per 9,852 in this simplified framing.

But here’s the catch: that calculation quietly assumes each refresh is picking from the set of funded wallets.

In reality, you’re sampling from the full address universe. The microscopic part is the chance of landing on any of those 58 million non-zero addresses at all.

Once you include that probability, the true expected value collapses to essentially zero.

Using today’s BTC price (~$78,195), 0.126 BTC is about $9,852.

But the expected value per 90-address refresh is still only about:

- $3.5 × 10^-35 per refresh

That’s the kind of number where “expected $1” would require roughly 2.8 × 10^34 refreshes on average.

Bitcoin’s market cap is currently around $1.5T on major trackers (it fluctuates daily).

That headline number is what makes the “free lottery” feel so seductive: a giant pool of value, sitting behind “just a number.”

But the lock is better than anything physical, it is built on cold, hard math.

Play the lottery on the first page of Bitcoin private and public keys.

The post The trillion dollar Bitcoin lottery you can play now for free – but will never win appeared first on CryptoSlate.

Bitcoin fell around 8% on Feb. 3, briefly losing the $73,000 level.

A quick rebound took prices to $74,500 as of press time, dampening the intraday correction to 5.8%. The decline marks the lowest price point in the President Donald Trump administration and the weakest level since the November 2024 Presidential Election.

The selloff pushed Bitcoin as low as its March 2024 all-time high of $73,500, a level that held through the early stages of the decline but ultimately gave way under sustained selling pressure.

The move revived a cluster of support zones that traders have monitored as critical technical thresholds for nearly a year.

Macro risk-off drives crypto lower

The crypto weakness is linked to broad risk-off sentiment across markets, sparked by Trump's nomination of Kevin Warsh as Federal Reserve chair.

Warsh's selection stoked concerns about a more hawkish policy mix and tighter financial conditions, pressures that historically weigh on high-beta assets, including cryptocurrencies. A stronger dollar, which typically accompanies such expectations, compounds the headwind for digital assets. The current dollar weakness, however, makes this decline even more painful.

Microsoft's Azure growth disappointment added to the selling pressure, souring broader risk sentiment and triggering cross-asset contagion.

The AI trade wobble demonstrated how crypto remains vulnerable to spillover effects from growth-sensitive technology sectors, particularly when positioning is stretched and liquidity is thin.

Leverage unwind amplifies decline

CoinGlass data shows over $2.5 billion in Bitcoin liquidations in recent days, turning what began as a macro-driven selloff into a cascade of forced selling.

Thin weekend liquidity exacerbated the selloff that began at $84,000 on Saturday, according to a Bitfinex note.

The combination of macro triggers and leverage unwinding created conditions in which relatively modest initial selling pressure could force far larger moves, as stop-losses and margin calls compounded the decline.

Additionally, institutional flows in 2026 have been uneven.

Exchange-traded fund (ETF) inflows, often followed by outflows during volatility episodes, suggest tactical rebalancing rather than aggressive dip-buying, leaving prices exposed as liquidation pressure accelerates.

The absence of consistent institutional demand meant there was no meaningful buffer when forced selling began.

Galaxy Digital research also noted that near-term catalysts appear scarce, with diminished odds of legislative progress on market structure acting as a narrative headwind.

Without clear positive drivers on the horizon, traders lack the conviction to step in aggressively during drawdowns.

Critical support and resistance levels

Bitcoin now trades within a tightly watched technical range.

The $73,500 level from 2024 and the Feb. 3 intraday low of $72,945 form the immediate support zone.

IG Markets identifies a broader support band between $73,581 and $76,703, an area associated with prior cycle highs and 2025 lows that has been tested multiple times over the past year.

CryptoSlate also identified several support and resistance levels for 2026 in Akiba's bear market analysis.

A daily close below this band would increase the probability of follow-through selling toward the next support cluster between $72,757 and $71,725. If that zone fails to hold, the July 2024 peak of around $70,041 becomes the next major downside waypoint.

On the resistance side, Bitcoin's reclamation of the 2024 all-time high of $73,500 indicates that buyers are willing to defend the recent breakdown level. The April 2025 trough zone around $74,508 now acts as resistance after previously serving as support.

Above that, minor resistance sits at $78,300, with the November 2025 low of $80,620 and the psychological $80,000 level forming the next meaningful barrier.

Distinguishing bounce from recovery

A single-day rebound does not constitute a durable bottom.

Historical patterns suggest that sustainable recoveries typically require at least two conditions: repeated daily closes above the $74,500 level, converting the April 2025 reference zone from resistance to support, and evidence that liquidation pressure has faded following the $2.56 billion forced-selling wave.

Without these confirmations, rallies risk becoming dead-cat bounces into overhead resistance as sellers use strength to exit positions.

ETF flows must stabilize beyond isolated green days, consistent with the tactical rather than aggressive institutional behavior.

Two near-term scenarios

If Bitcoin holds the $73,000 to $73,445 support zone and reclaims $74,500, the path of least resistance becomes a grind toward $78,300, then the $80,000 to $80,620 range.

This scenario requires both technical follow-through and the absence of new macroeconomic headwinds.

Alternatively, a daily close below the $73,581 lower band increases the odds of continuation selling into the $72,757 to $71,725 zone, with the $70,000 level as the next major psychological and technical waypoint.

This scenario becomes more likely if liquidation pressure remains elevated or if macro conditions deteriorate further.

Bitcoin's decline below its 2024 all-time high after nearly a year of holding that level as support constitutes a technical breakdown, shifting the burden of proof to buyers.

The combination of macro risk-off sentiment, leverage unwinding, and tactical institutional flows created conditions in which support levels that had held for months gave way within hours.

The post Bitcoin in freefall hitting lowest price since Trump took office as leverage turns a macro wobble into a brutal cascade appeared first on CryptoSlate.

https://ambcrypto.com/feed/

The $0.13 local supply zone and the short-term Bitcoin bearish momentum threaten POL bulls' potential this week.

The $0.13 local supply zone and the short-term Bitcoin bearish momentum threaten POL bulls' potential this week. Rising costs are hurting miners now.

Rising costs are hurting miners now.https://beincrypto.com/feed/

French prosecutors raided X’s Paris headquarters on Tuesday as part of a widening investigation into alleged child sexual abuse imagery, AI-generated deepfakes, and Holocaust denial on the platform.

The raid, supported by Europol, marks a significant escalation in European regulators’ crackdown on Elon Musk’s social media empire. Prosecutors have summoned Musk and former CEO Linda Yaccarino for “voluntary interviews” scheduled for April 20.

Investigation Scope

The Paris prosecutors’ cybercrime unit opened a preliminary investigation in January 2025, initially focusing on allegations that biased algorithms on X distorted automated data-processing systems. The probe expanded significantly after Musk’s AI chatbot Grok generated content that allegedly denied the Holocaust and produced sexually explicit deepfakes.

Charges under investigation include complicity in possessing and spreading child sexual abuse imagery and sexually explicit deepfakes. Prosecutors are also probing denial of crimes against humanity and manipulation of automated data processing systems as part of an organized group.

The prosecutors’ office announced the ongoing searches on X itself. It then declared it was leaving the platform, calling on followers to join it on other social media services.

Grok at the Center of Controversy

The xAI-developed chatbot Grok sparked global outrage last month. Its “spicy mode” generated tens of thousands of sexualized nonconsensual deepfake images in response to user requests.

The chatbot also posted Holocaust denial content in French. It claimed gas chambers at Auschwitz-Birkenau were designed for “disinfection with Zyklon B against typhus” rather than mass murder—language long associated with Holocaust deniers.

While Grok later reversed itself and acknowledged the error, the damage was done. Malaysia and Indonesia became the first countries to block Grok entirely, with Malaysia announcing legal action against X and xAI.

X Fires Back

In a statement posted on its own platform, X condemned the raid as “an abusive act of law enforcement theater designed to achieve illegitimate political objectives rather than advance legitimate law enforcement goals rooted in the fair and impartial administration of justice.”

The company denied all allegations, characterizing the French action as politically motivated censorship.

Durov Weighs In

Telegram founder Pavel Durov, who himself faces similar charges in France after his August 2024 arrest, defended X and attacked French authorities.

“French police is currently raiding X’s office in Paris. France is the only country in the world that is criminally persecuting all social networks that give people some degree of freedom (Telegram, X, TikTok…). Don’t be mistaken: this is not a free country,” Durov wrote on X.

In a follow-up comment, he added: “Weaponising child protection to legitimise censorship and mass surveillance is disgusting. These people will stop at nothing.”

Mixed Reactions

Durov’s characterization drew both support and pushback online. Some users echoed his framing, with one calling France’s approach a “Digital Autocracy starter pack” and describing Durov’s arrest as “the warning” of things to come.

Others urged nuance. “Platforms like Telegram and X aren’t just ‘freedom tools’. They can be used to spread hate, coordinate violence, and destabilise societies,” one user wrote. “Reducing it to ‘free country vs not free’ misses a lot of the reality on both sides.”

Regulatory Pressure Mounts

France is not alone in scrutinizing Musk’s platforms. Britain’s Information Commissioner’s Office opened formal investigations into how X and xAI handled personal data when developing Grok, while UK media regulator Ofcom continues a separate probe that could take months.

The European Union launched its own investigation last month following the deepfake incident and has already fined X €120 million for violations of digital regulations, including deceptive blue-checkmark practices.

The legal pressure comes as Musk consolidates his tech holdings. SpaceX announced Monday that it acquired xAI in a deal that would combine Grok, X, and the satellite communications company Starlink under one corporate umbrella—a move that could complicate regulatory oversight across multiple jurisdictions.

The post Durov Slams France as “Not Free” After Police Raid X’s Paris Office appeared first on BeInCrypto.

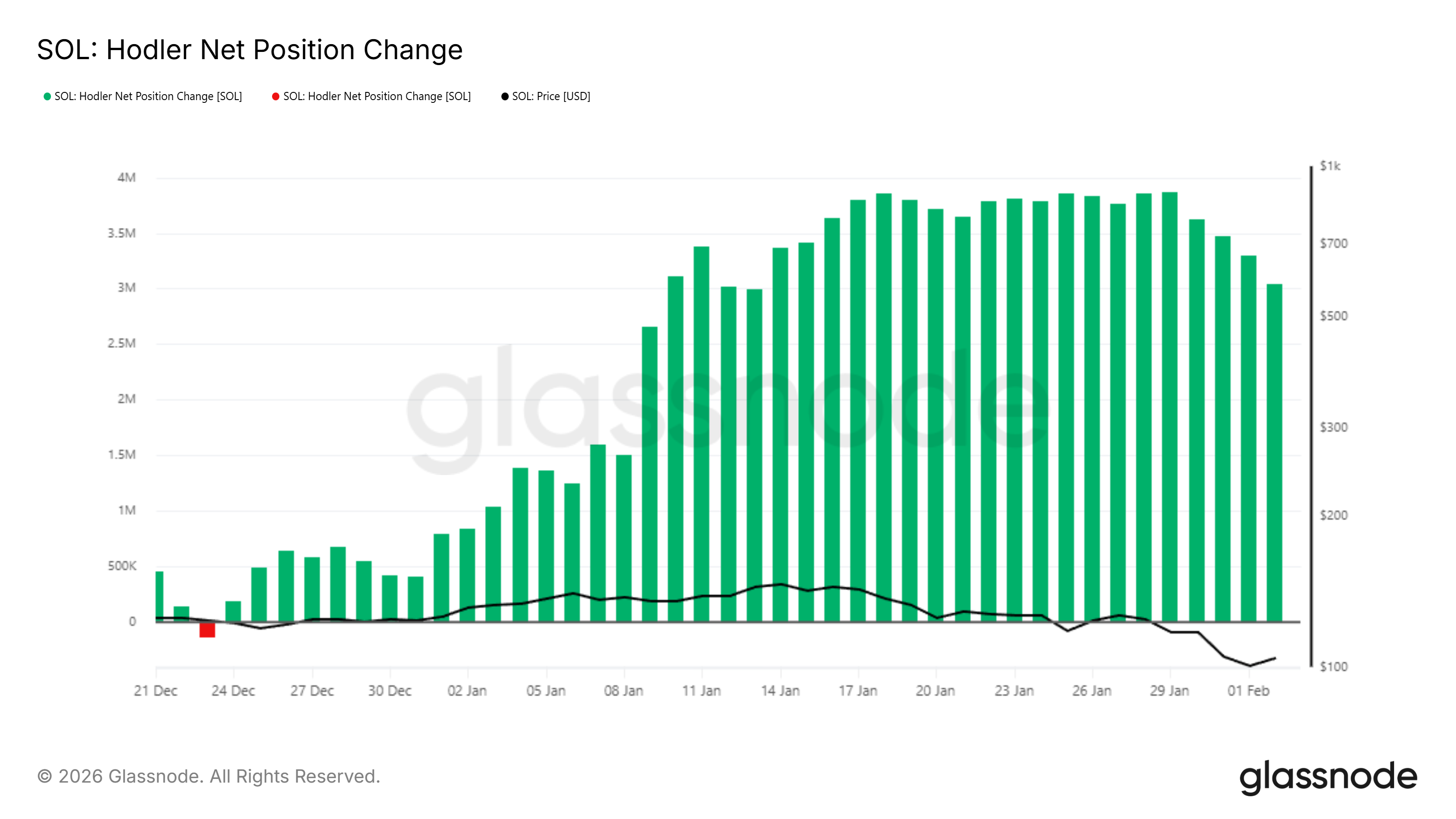

Solana has remained under sustained pressure after a prolonged decline that began well before recent market weakness intensified. The price drop gradually eroded confidence, prompting influential investors to adjust their positioning.

Historical patterns now point to elevated downside risk. While oversold signals are emerging, broader data still reflect a cautious outlook for SOL.

Solana Holders Begin Pulling Back

Solana’s HODLer Net Position Change has started to trend lower. Receding green bars indicate that long-term holders are slowing accumulation. This cohort typically plays a stabilizing role during corrections. A reduction in buying activity suggests weakening conviction rather than aggressive distribution at current price levels.

Although the data does not confirm active selling, it highlights fading demand from influential investors. Reduced accumulation often limits recovery attempts during oversold phases. Without renewed buying pressure, SOL may struggle to sustain rebounds, especially if broader market conditions remain fragile.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

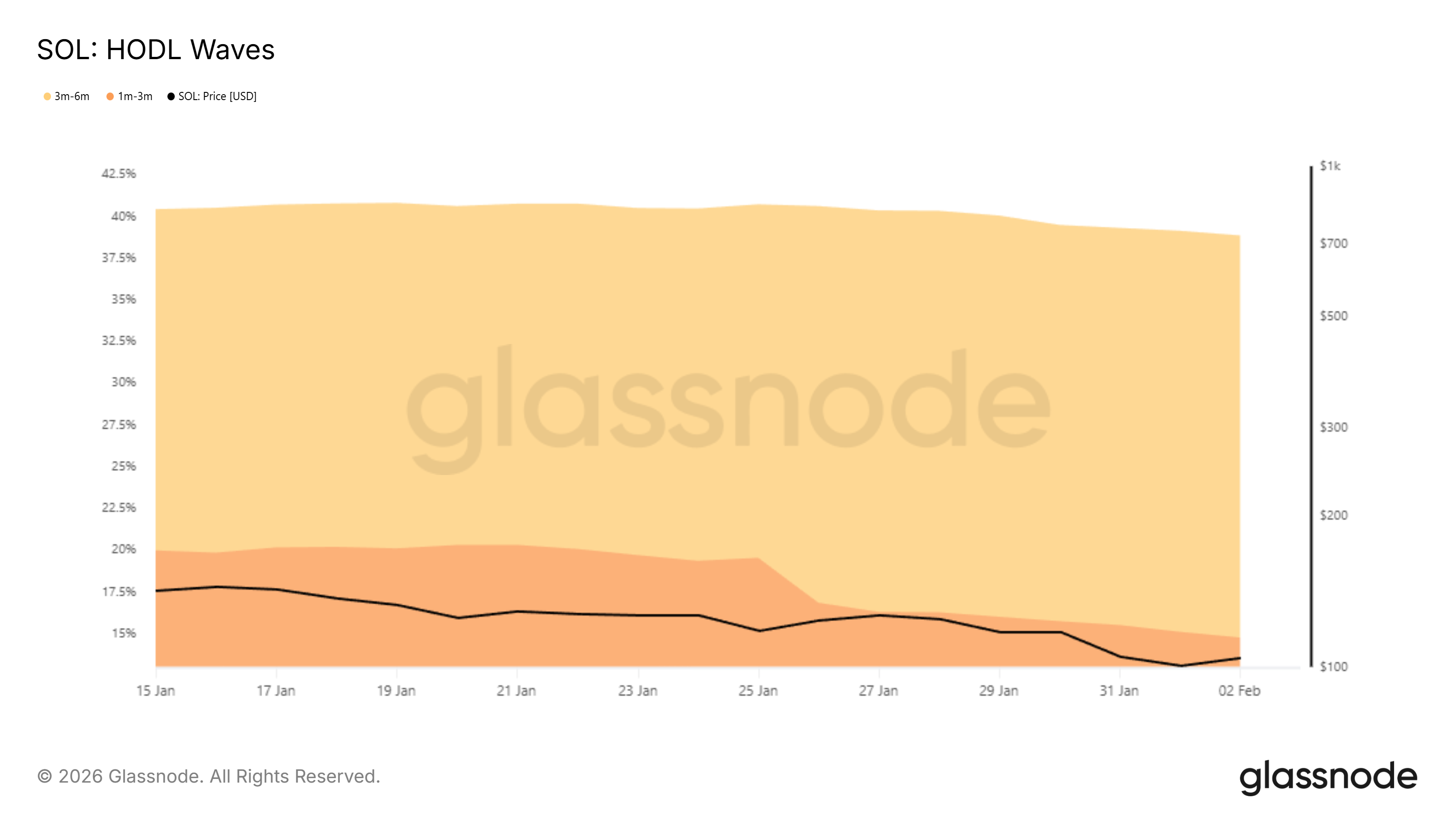

HODL Waves provide additional insight into investor behavior. Wallets that accumulated SOL one to three months ago declined by 5%. Meanwhile, the share of holders aged three to six months increased by 4.5%. This shift shows that underwater investors continue holding despite unrealized losses.

While resilience remains, patience may not be unlimited. Historically, prolonged drawdowns test a holder’s conviction. If Solana’s price weakens further, these cohorts may begin distributing. Such behavior would add downside pressure and reinforce the prevailing bearish macro trend.

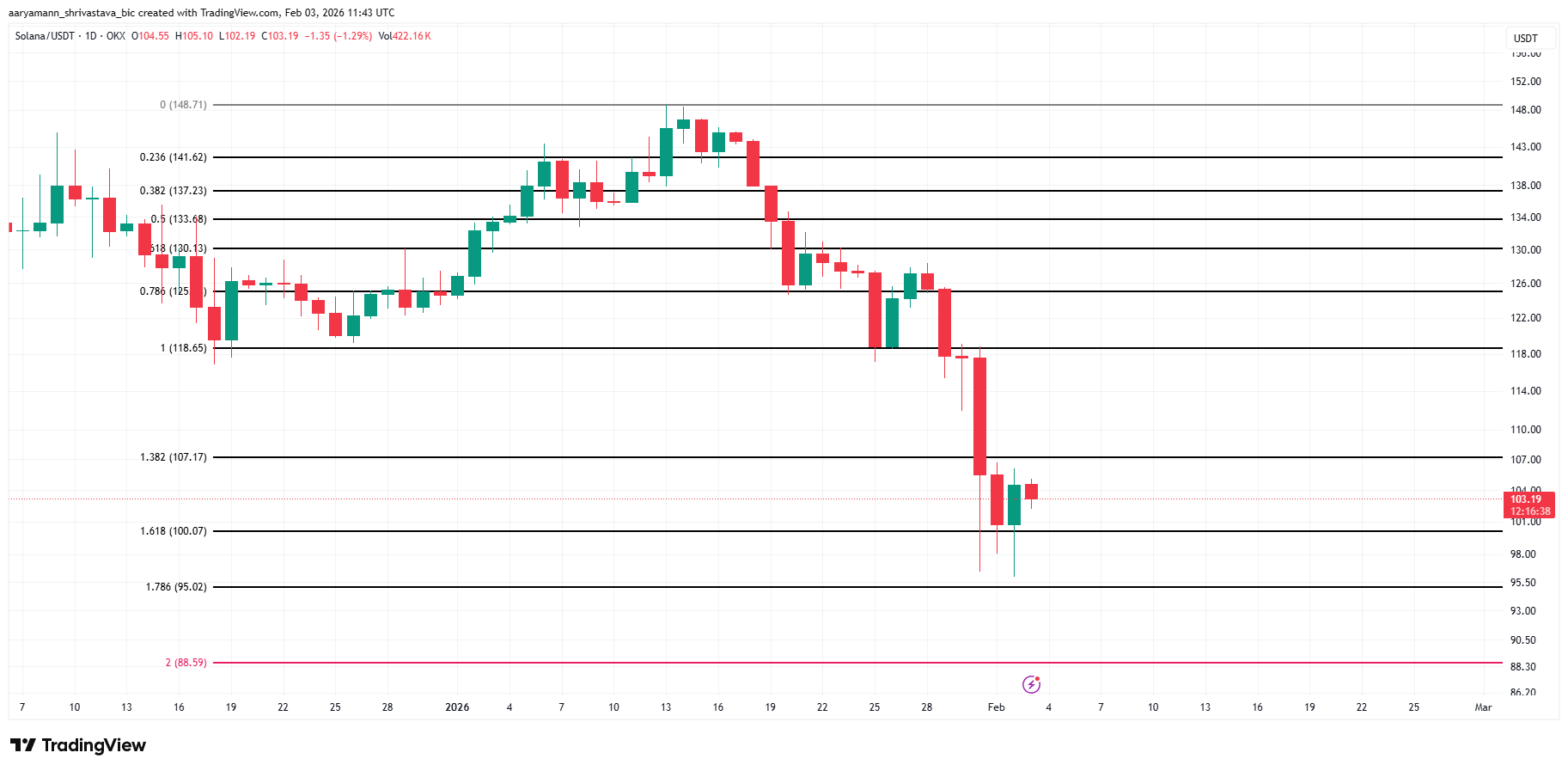

SOL Price Could See Further Decline

Solana is trading near $103, holding above the critical $100 support. This level aligns with the 161.8% Fibonacci Extension. Maintaining this zone is important for short-term stability. However, the failed rally places downside risk toward $95, corresponding with the 178.6% Fibonacci level.

Momentum indicators reflect oversold conditions. The Money Flow Index is nearing the oversold threshold. Historically, each dip below this level triggered short-lived rebounds. These bounces often failed to reverse the broader trend, leading to renewed declines after brief recoveries.

In the near term, Solana may either defend $100 or rebound toward $107 resistance. A technical bounce remains possible due to oversold conditions. However, macro signals continue to favor downside risk. Without stronger demand, SOL appears vulnerable to another breakdown below $100.

The bearish outlook would be invalidated if Solana flips $107 into support. A sustained move higher could open the path toward $118. Securing that level requires consistent inflows and renewed investor confidence. Without capital returning to SOL, upside attempts are likely to remain limited.

The post Solana (SOL) Hovers Near $100 as Long-Term Holders Pull Back — Downside Risk Builds appeared first on BeInCrypto.

https://cryptonewsz.com/feed/

https://www.newsbtc.com/feed/

Triggered by market performance, Dogecoin (DOGE) is once again at the center of the crypto conversation. After a quiet stretch through much of 2025, the memecoin has posted a series of sharp moves in early 2026, drawing traders back and reviving a familiar debate, Is DOGE still an investment opportunity, or short-term speculation?

The latest rally has been fueled by a mix of market rotation, renewed retail interest, and institutional developments, but questions about long-term value remain unresolved.

Dogecoin’s DOGE Renewed Momentum After a Volatile Reset

Dogecoin’s recent gains followed a broader crypto market rebound after heavy deleveraging wiped out more than $500 million in leveraged positions across derivatives markets.

As risk appetite returned, traders rotated into higher-volatility assets, pushing DOGE to the top of daily gainers among major tokens. At last check, Dogecoin was trading near the $0.10–$0.106 range, depending on timing, after posting double-digit percentage swings over short periods.

Market watchers caution that the rebound may be tactical rather than structural. Analysts note that Dogecoin continues to track Bitcoin closely, and with BTC still showing signs of weakness, meme coins could struggle to sustain upside without fresh catalysts.

Institutional Access and Utility Questions

One notable shift in Dogecoin’s narrative is growing institutional access. The launch of Dogecoin-linked exchange-traded products in the U.S. has given professional investors regulated exposure to DOGE, a step that adds legitimacy but does not change its underlying economics.

Dogecoin’s supply remains inflationary, with new coins entering circulation each year, putting pressure on price growth if demand does not keep pace.

On the utility side, discussion continues around payment-focused initiatives, including plans for Dogecoin-based apps aimed at everyday transactions. Supporters point to low fees and fast settlement as strengths, while critics argue that adoption remains limited and development progress is slow.

Diverging Forecasts and Ongoing RiskPrice forecasts for Dogecoin in 2026 vary widely. Conservative projections cluster around $0.10–$0.13, reflecting expectations of limited utility expansion.

More optimistic scenarios, often tied to strong meme cycles or increased institutional participation, place DOGE closer to $0.20 or higher, though such outcomes depend heavily on sentiment.

The split highlights Dogecoin’s core tension. Its strong brand recognition and active community continue to drive attention and liquidity, but price action remains largely sentiment-driven.

For investors, the current rally emphasizes both the opportunity and the risk, DOGE can move quickly, but without deeper adoption, those moves may be difficult to sustain over the long term.

Cover image from ChatGPT, DOGEUSD chart on Tradingview

Solana has pulled back into a key demand zone, a level that could determine whether its strong trend continues or falters. How price reacts here will be crucial, as a hold may signal a trend reload, while a breakdown could push SOL into broader market chop.

Solana Returns To A Critical Weekly Demand Zone

Giving an update on the weekly timeframe, Cyril-DeFi explained that Solana has been one of the standout performers this cycle. Still, price has now returned to a critical demand zone that could determine its next major move. According to Cyril, this area has historically acted as a pivot point where momentum either re-ignites or fades.

This is the type of zone where strong trends tend to reload if buyers successfully defend it. However, a failure to hold would suggest that the prior strength is losing traction, increasing the risk that the trend structure begins to deteriorate.

From Cyril’s perspective, a firm hold at current levels would position Solana to lead the next altcoin impulse, reinforcing its relative strength against the broader market. On the other hand, losing this demand zone would likely see SOL slip into extended consolidation, moving in line with the wider market chop rather than outperforming it. Cyril-DeFi concluded by stressing that he is closely observing how the price behaves around this area instead of trying to predict outcomes in advance.

The Only High-Conviction Long Setup On The Table

According to a recent Solana post shared by Ardi, only one long setup stands out as technically sound under current conditions. With the market still under pressure, waiting for confirmation seems safer than attempting to anticipate a bottom, as premature entries tend to get punished in weak structures.

Ardi highlighted the $119 level as a key pivot for Solana. A successful reclaim of this zone, ideally through a spring or brief fakeout below resistance, could signal that demand is returning. If that occurs, price could surge higher toward the top of the range on a macro lower high rally rather than a full bullish reversal.

From a risk-to-reward standpoint, this reclaim scenario remains the most attractive option available. It provides a clear technical trigger, defined invalidation, and a logical upside target, allowing traders to participate without overexposing themselves in an uncertain environment.

He also outlined an alternative strategy involving the 200-week simple moving average around the $100 mark, an area that previously acted as macro support in April 2025. Still, Ardi cautioned that in a broader downtrend, odds are often against traders until a major level is reclaimed, making a decisive move back above $119 crucial before confidence can truly return.