Financial RSS Feeds

https://www.investing.com/rss/news.rss

https://cointelegraph.com/rss

Bitcoin Bollinger BandWidth plumbed new record lows after printing a classic "green" signal in November that previously saw 40% BTC price upside.

Daily futures wipeouts are surging as leverage builds, with a record unwind in October exposing how deeply derivatives now shape Bitcoin’s market cycle.

https://www.coindesk.com/arc/outboundfeeds/rss/

https://cryptobriefing.com/feed/

This partnership could accelerate institutional adoption of crypto by aligning staking services with traditional finance standards and security.

The post Deutsche Bank-backed Taurus partners with Everstake to enhance institutional crypto staking appeared first on Crypto Briefing.

Tokenization's potential to revolutionize financial systems could reshape market dynamics and investment strategies, impacting global asset management.

The post BlackRock CEO Larry Fink, Brian Armstrong to discuss tokenization at DealBook Summit appeared first on Crypto Briefing.

https://bitcoinist.com/feed/

Bank of America is the latest traditional institution to warm up to Bitcoin, with its investment strategists set to cover four ETFs starting in January.

Bank of America To Begin Endorsing Crypto Exposure

As reported by Yahoo Finance, Bank of America will start recommending its clients a 1% to 4% portfolio allocation to digital assets. Until now, the bank’s wealth advisors couldn’t endorse crypto exposure and clients had to request access to digital asset products if they wanted them in their portfolio.

With this move, Bank of America advisors can begin recommending digital asset exposure to clients across the bank’s Merrill, Bank of America Private Bank, and Merrill Edge Platforms. “Our guidance emphasizes regulated vehicles, thoughtful allocation, and a clear understanding of both the opportunities and risks,” said Chris Hyzy, chief investment officer at Bank of America Private Bank.

Investment strategists will initially cover four Bitcoin exchange-traded funds (ETFs) starting January 5. ETFs are investment vehicles that allow traders to invest into an underlying asset without having to directly own it. Since they trade on traditional platforms and are regulated, institutional entities prefer to invest through them.

The four spot Bitcoin ETFs Bank of America will be focusing on include Bitwise’s BITB, BlackRock’s IBIT, Fidelity’s FBTC, and Grayscale’s BTC.

Bank of America is one of the largest financial institutions in the world, ranking only second behind JPMorgan Chase in market cap and placing sixth largest in terms of total assets. It’s designated as a global systemically important bank (G-SIB) by the Financial Stability Board (FSB), meaning it’s so entrenched in world economy that instability related to it could have widespread consequences.

Even an institution of its size no longer being able to ignore Bitcoin showcases just how far digital asset adoption in traditional finance has come. “This update reflects growing client demand for access to digital assets,” noted Nancy Fahmy, head of Bank of America’s investment solutions group.

The news arrives just a day after Vanguard Group, one of the largest asset managers in the world, opened its doors to crypto ETFs and mutual funds.

Morgan Stanley, another G-SIB, broadened access to crypto exposure for its clients back in October. The financial services institution’s global investment committee suggested 2% to 4% allocation in digital assets.

Bank of America’s recommendation of 1% to 4% is quite similar. “The lower end of this range may be more appropriate for those with a conservative risk profile, while the higher end may suit investors with greater tolerance for overall portfolio risk,” added Hyzy.

Bitcoin Price

Bitcoin has already recovered from its Monday blow as its price has returned to $92,100.

Quick Facts:

Celebrity investor, Kevin O’Leary’s view that Bitcoin can hold up without imminent Fed cuts shifts attention from macro speculation to actual network adoption.

Celebrity investor, Kevin O’Leary’s view that Bitcoin can hold up without imminent Fed cuts shifts attention from macro speculation to actual network adoption.- Bitcoin’s base layer still struggles with throughput, fees, and programmability, pushing real-world DeFi and gaming activity toward faster, smart-contract-ready ecosystems.

- Competing Bitcoin Layer 2s are racing to bring scalable execution to $BTC, utilizing designs ranging from payment channels to roll-ups and modular sidechains.

- Bitcoin Hyper introduces an SVM-powered Bitcoin Layer 2 that targets Solana-level performance while anchoring settlement to $BTC, aiming to unlock programmable, low-fee Bitcoin DeFi.

Kevin O’Leary’s latest stance on Bitcoin is ($BTC) blunt: if the asset’s investment case depends on a single Federal Reserve meeting, it probably wasn’t robust to begin with.

The Canadian businessman and TV personality’s argument that $BTC can hold its own even without near-term rate cuts shifts the spotlight back to adoption, utility, and real transaction demand.

For you as a $BTC holder, that’s a very different conversation from the usual ‘pivot or no pivot’ guessing game. If Bitcoin is going to matter regardless of Fed timing, then the infrastructure that actually lets people pay, trade, and build on top of it becomes the real battleground for upside.

That’s where Bitcoin’s structural limits come roaring back into view.

The base layer still handles roughly seven transactions per second (TPS), with long confirmation times and fee spikes during congestion. That’s fine as a store-of-value ledger, but it’s a non-starter for high-frequency DeFi or gaming.

The base layer still handles roughly seven transactions per second (TPS), with long confirmation times and fee spikes during congestion. That’s fine as a store-of-value ledger, but it’s a non-starter for high-frequency DeFi or gaming.

Bitcoin Hyper ($HYPER) steps into that gap as a high-octane way to express long-term $BTC conviction.

Instead of trying to time macro, it offers a Bitcoin-aligned Layer 2 that uses a Solana Virtual Machine (SVM) execution layer to push performance to and beyond Solana-style speeds, while anchoring settlement and trust back to Bitcoin itself.

Why Macro Fatigue Is Pushing Attention Back to Bitcoin Infrastructure

After two years of ‘will they, won’t they’ on Fed cuts, investor fatigue is real. Bitcoin’s resilience through multiple rate-hike cycles has already tested the original thesis that it’s a levered bet on liquidity. Increasingly, the more durable narrative is that $BTC will survive macro noise if it keeps gaining real-world usage.

At the same time, Bitcoin’s base chain was never designed for modern, smart-contract-heavy workloads. Competing Layer 1s like Solana and Ethereum offer sub-second or low-single-second finality and thousands of transactions per second, with fees often below $0.01.

That’s why you see NFTs, perpetual DEXs, and gaming clusters gravitate there instead of to Bitcoin.

To pull that activity back toward $BTC, a new wave of infrastructure is emerging.

Among the frontrunners, Bitcoin Hyper fits into that broader race as one of several contenders trying to marry Bitcoin’s settlement guarantees with throughput and programmability that can actually host complex DeFi, NFT, and gaming ecosystems at scale.

Learn more about the project in ‘What is Bitcoin Hyper?’

Learn more about the project in ‘What is Bitcoin Hyper?’

How Bitcoin Hyper Turns BTC Conviction Into High-Throughput Utility

Where Bitcoin Hyper differentiates itself is in its preferred execution layer. Rather than inventing yet another VM, it integrates the Solana Virtual Machine directly into a Bitcoin Layer 2.

That means developers can tap SVM’s parallelized execution and high TPS design, while still routing economic value through Bitcoin.

Under the hood, Bitcoin Hyper uses a modular design: Bitcoin Layer 1 acts as the settlement and security anchor, while a real-time SVM Layer 2 handles execution.

A single sequencer batches and orders transactions, periodically anchoring state back to Bitcoin. The result is extremely low-latency processing for swaps, payments, and dApp calls, while $BTC itself remains the ultimate source of truth.

For users, that architecture shows up as practical advantages: high-speed payments in wrapped $BTC with low fees, DeFi primitives like swaps, lending, and staking, plus NFT and gaming dApps built in Rust using familiar SVM tooling.

SPL-compatible tokens are adapted for the Layer 2, giving Solana-native builders a clear porting path into the Bitcoin universe without rewriting everything from scratch.

On the market side, the presale has already raised over $28.8M, with tokens currently offered at $0.013365, signaling strong demand for a BTC-centric scalability play.

Whales are also betting big on the project, with one recently snapping up over $500K worth of $HYPER tokens.

If you want to grab your share of tokens, you can check out our Bitcoin Hyper buying guide for more information.

If you want to grab your share of tokens, you can check out our Bitcoin Hyper buying guide for more information.

Meanwhile, if you’re more of a long-term investor, you’ll be pleased to know that $HYPER has a huge potential upside given its premise. By the end of 2026, $HYPER could go a high of $0.20, or a 1396% increase from its current price.

But with yet another price increase coming up in a few hours, now’s your chance to buy tokens at a currently discounted price.

Join the $HYPER presale today.

This article is for informational purposes only and does not constitute financial, investment, or trading advice; always do your own research.

Authored by Bogdan Patru, Bitcoinist — https://bitcoinist.com/kevin-oleary-says-fed-cuts-wont-impact-bitcoin-as-bitcoin-hyper-pumps

https://cryptoslate.com/feed/

Bitcoin was launched fifteen years ago. The industry has ballooned into a nearly $4 trillion ecosystem, yet Satoshi’s vision of everyday payments remains largely unfulfilled. The hope for peer-to-peer payments has shifted to stablecoins. But rather than replacing banks, stablecoins risk becoming bank-like infrastructure. Stronger regulation in the U.S. and Europe may push them toward centralized rails rather than open money.

Regulation turning stablecoins into regulated payment networks

In America, the GENIUS Act established a federal framework for payments with stablecoins—who can issue them, how to back them up, and how they’re regulated. In Europe, MiCA regulation (Markets in Crypto-Assets) became applicable in 2024 and set strict requirements for stablecoins under categories like “e-money tokens” and “asset-referenced tokens.”

These regulations foster legitimacy and safety, but at the same time push stablecoin issuers into the world of banks. When issuers need to comply with reserve, audit, KYC, and redemption requirements, the structure and essence of stablecoins shift. They become centralized gateways rather than peer-to-peer money. Over 60% of corporate stablecoin usage is cross-border settlement, not consumer payments. Stablecoins are becoming more institutional tools and fewer tokens for individuals.

The danger: becoming the next SWIFT

What does it mean to “become the next SWIFT”? It means evolving into the go-to rail for institutions; efficient yet opaque, centralized yet indispensable. SWIFT transformed global banking by enabling messaging between banks; it did not democratize banking access. If stablecoins mirror that evolution, they’ll deliver faster rails for existing players rather than empowering the unbanked.

Crypto’s promise was programmable money—cash that moves with logic, autonomy, and user control. But when transactions require issuer permission, compliance tagging, and monitored addresses, the architecture changes. The network becomes compliant infrastructure, not money. That subtle but profound shift may make stablecoins less radical and more reactionary.

A better path to open rails with compliance baked in

The challenge is not regulation; it’s design. To uphold the promise of stablecoins while adhering to regulatory demands, developers and policymakers should embed compliance in the protocol layer, maintain composability across jurisdictions, and preserve non-custodial access. Back in the real world, initiatives like the Blockchain Payments Consortium provide a glimpse of hope that standardizing cross-chain payments is possible without sacrificing openness.

Stablecoins must work for individuals, not just institutions. If they serve only large players and regulated flows, they won’t disrupt—they’ll conform. The design must allow true peer-to-peer movement, selective privacy, and interoperability. Otherwise, the rails will lock us into old hierarchies, just faster.

Stablecoins still hold the potential to rewrite money. But if we allow them to become institutionalized rails built for banks rather than people, we will have replaced one central system with another. The question isn’t whether we regulate—stablecoins will be regulated. It’s whether we design for inclusion and autonomy, or lock in yesterday’s system behind digital wrappers. The future of money depends on which path we choose.

The following is a guest post and opinion from Joël Valenzuela, Director of Marketing and Business Development at Dash.

The post Stablecoins were built to replace banks but on course to becoming one appeared first on CryptoSlate.

XRP spot ETFs have posted one of the most consistent inflow streaks of this quarter, attracting roughly $756 million across eleven consecutive trading sessions since their Nov. 13 launch.

Yet the strength in the ETF demand contrasts with XRP’s price performance.

According to CryptoSlate’s data, the token has fallen about 20% over the same period and currently trades near $2.03.

This divergence has prompted CryptoSlate to examine how XRP’s ownership structure is shifting beneath the surface.

The strong ETF inflows alongside falling prices point to a market absorbing two opposing forces of steady institutional allocation on one side and a broader risk reduction on the other.

Essentially, this pattern reflects a more complex process in which new, regulated demand is entering the ecosystem as existing holders adjust their exposure.

XRP dominates crypto ETFs flow

The inflow profile of XRP products is statistically remarkable, particularly against a backdrop of net redemptions elsewhere.

During the reporting period, Bitcoin ETFs saw over $2 billion in outflows, and Ethereum products recorded nearly $1 billion in withdrawals.

Even high-flying competitors like Solana have managed only about $200 million in cumulative inflows. At the same time, other altcoin ETFs have drawn smaller totals, with Dogecoin, Litecoin, and Hedera products each holding between $2 million and $10 million.

In this context, XRP stands alone for its consistent accumulation, with the four products now holding about 0.6% of the token’s total market capitalization.

Considering this, market participants attribute the demand to the ETF’s operational efficiency. The four XRP funds offer institutional allocators a compliant, low-friction path into the asset, bypassing the custody headaches and exchange risks associated with direct token handling.

However, the fact that these inflows have not translated into upward price pressure suggests that other market segments may be reducing exposure or managing risk amid elevated macro and crypto-specific uncertainty.

This phenomenon is not unprecedented in crypto, but the scale here is distinct.

The selling pressure is likely originating from a combination of early adopters cashing out after years of volatility and potential treasury movements. The ETF boom has essentially created a liquidity bridge, allowing large-scale entities to offload positions without crashing the order book instantly.

Consolidation or centralization risk?

Meanwhile, the ownership data below the surface reinforces the view that the asset is undergoing a radical centralization.

Data from blockchain analysis firm Santiment indicates that the number of “whale” and “shark” wallets holding at least 100 million XRP has plummeted by 20.6% over the past eight weeks.

This pattern of fewer large wallets with more combined assets can be interpreted in different ways.

Some market observers have framed this as “consolidation,” arguing that supply is moving into “stronger hands.”

However, a risk-adjusted view suggests rising centralization risk.

With nearly half of the available supply concentrated in a shrinking cohort of entities, the market’s liquidity profile is becoming increasingly fragile.

This centralization of supply means that future price action is heavily dependent on the decisions of fewer than a few dozen entities. If this group decides to distribute, the resulting liquidity shock could be severe.

Simultaneously, spot exchange balances are thinning as tokens move into the regulated custody solutions required by ETF issuers.

While this theoretically reduces the “float” available for retail trading, it hasn’t triggered a supply shock. Instead, the transfer from exchange to custodian appears to be a one-way street for now, soaking up circulating supply sold by the shrinking whale cohort.

The benchmark race

The inflow streak has renewed discussion about which asset could emerge as the benchmark altcoin for institutional portfolios.

Historically, regulated crypto exposure has centered almost exclusively on Bitcoin and Ethereum, with other assets attracting minimal attention. XRP’s recent flow profile, which has significantly exceeded the cumulative inflows of other altcoin ETFs, has temporarily shifted that dynamic.

Part of the interest stems from developments around Ripple. The firm’s licensing expansion in Singapore and the significant adoption of RLUSD, its dollar-backed stablecoin, give institutions a broader ecosystem to evaluate.

At the same time, Ripple’s acquisitions across custody, brokerage, and treasury management have created a vertically integrated framework that resembles components of traditional financial infrastructure, offering a foundation for regulated participation.

Still, analysts caution that a short inflow streak does not establish a new long-term benchmark.

XRP will need to sustain demand across multiple market phases to maintain its position relative to peers such as Solana, which has gained attention for its growing tokenization activity, and to assets that may attract larger flows once new ETFs launch.

For now, XRP’s performance within the ETF complex reflects early momentum rather than structural dominance.

The flows highlight genuine institutional interest, but the asset’s price behavior reflects the broader challenges large-cap cryptocurrencies face amid macroeconomic uncertainty.

The post How XRP became the top crypto ETF trade despite price slides toward $2 appeared first on CryptoSlate.

https://ambcrypto.com/feed/

Is Bitcoin's 'Santa rally' back, or will Japan spoil the party?

Is Bitcoin's 'Santa rally' back, or will Japan spoil the party?  Post-upgrade demand will determine if an ETH rally will follow.

Post-upgrade demand will determine if an ETH rally will follow.https://beincrypto.com/feed/

This article is authored by Arthur Firstov, the Chief Business Officer at Mercuryo, a global leader in crypto payments infrastructure. Arthur is a recognized voice on stablecoins, digital banking, and the convergence of web3 and traditional finance – and this article is based on his insights from partnerships with more than 300 companies, including Circle, Coinbase, Mastercard, Revolut, and Polymarket.

As the digital assets market matures beyond speculation, a new phase of global finance is emerging, one defined by interoperability, compliance, and inclusion. Speaking at Token2049 Singapore 2025, Arthur Firstov outlined how the next evolution of financial systems is closing the gap between decentralized finance (DeFi) and traditional financial institutions.

The conversation focused on a simple idea with big implications: the worlds of crypto and mainstream finance are no longer parallel universes. They are converging to build accessible, efficient, and transparent global markets for both institutional and retail participants.

A Payment Layer for the Digital-Asset Era

“Stablecoins are becoming the new fintech,” says Firstov, who believes that in the next few years, every fintech company will, in effect, be a stablecoin company.

The data supports this trajectory. Recent research shows that stablecoin transfers for payments have already reached roughly $19.4 billion year-to-date in 2025 and are on pace to surpass $1 trillion annually by 2030, just for the emerging payments use cases, not speculative trading. At the same time, McKinsey now estimates that total stablecoin transaction volume across all use cases has already topped $27 trillion a year, putting it on a potential path to overtake legacy networks before the decade is out.

That growth highlights how quickly the narrative has shifted from “crypto trading” to “digital settlement rails.”

“In practice, the experience is seamless. Users can buy digital assets with a debit card or Apple Pay, convert them into stablecoins, send value globally in seconds, and cash out to a bank account,” Firstov explains.

Behind that simplicity is an expanding network of wallets, fintechs, and global payment rails working together to power instant, borderless transfers, the foundation of a new digital-asset settlement layer for the modern economy.

From Skepticism to Scale: Klarna, Tempo and the New Rails

One of the clearest signals that this shift is real comes from names that, until recently, had nothing to do with crypto.

In late 2025, Swedish digital bank Klarna, best known for its “buy now, pay later” services, announced KlarnaUSD, its first U.S.-dollar stablecoin, built on Tempo, a new payments-focused blockchain developed by Stripe and Paradigm.

KlarnaUSD is issued via Bridge’s Open Issuance platform (a Stripe company) and is currently live in test mode, with a full launch on Tempo’s mainnet planned for 2026. Klarna explicitly frames the move as a way to:

– Bypass expensive, slow cross-border payment routes

– Tap into a $120 billion annual cross-border fee pool

– Serve over 100 million existing customers on cheaper, programmable rails

For Firstov, this kind of partnership is exactly what “closing the gap” looks like in practice:

“When a digital bank like Klarna launches a stablecoin on a dedicated payments blockchain, the story is no longer ‘crypto people sending tokens to each other.’ It is mainstream payment companies quietly rewriting their settlement stack on top of stablecoin rails.”

Moves like KlarnaUSD on Tempo sit in the same category as PayPal’s PYUSD and other institution-led experiments: they are early, controlled, and compliance-heavy, but they reveal where the industry expects the real growth to come from.

Who Is Using It and Why

“The digital-assets audience usually consists of blockchain enthusiasts and developers driving innovation in the space,” Firstov says.

But he adds that the user base now extends far beyond tech insiders:

– Digital nomads managing income across borders

– People with families abroad sending remittances

– Aspiring founders and freelancers getting paid globally

– More sophisticated users exploring new digital-asset products and yield opportunities

This variety of users reflects the growing diversity in access. In Latin America and Southeast Asia, where local currencies often face severe volatility, stablecoins are increasingly used as everyday banking alternatives rather than speculative assets.

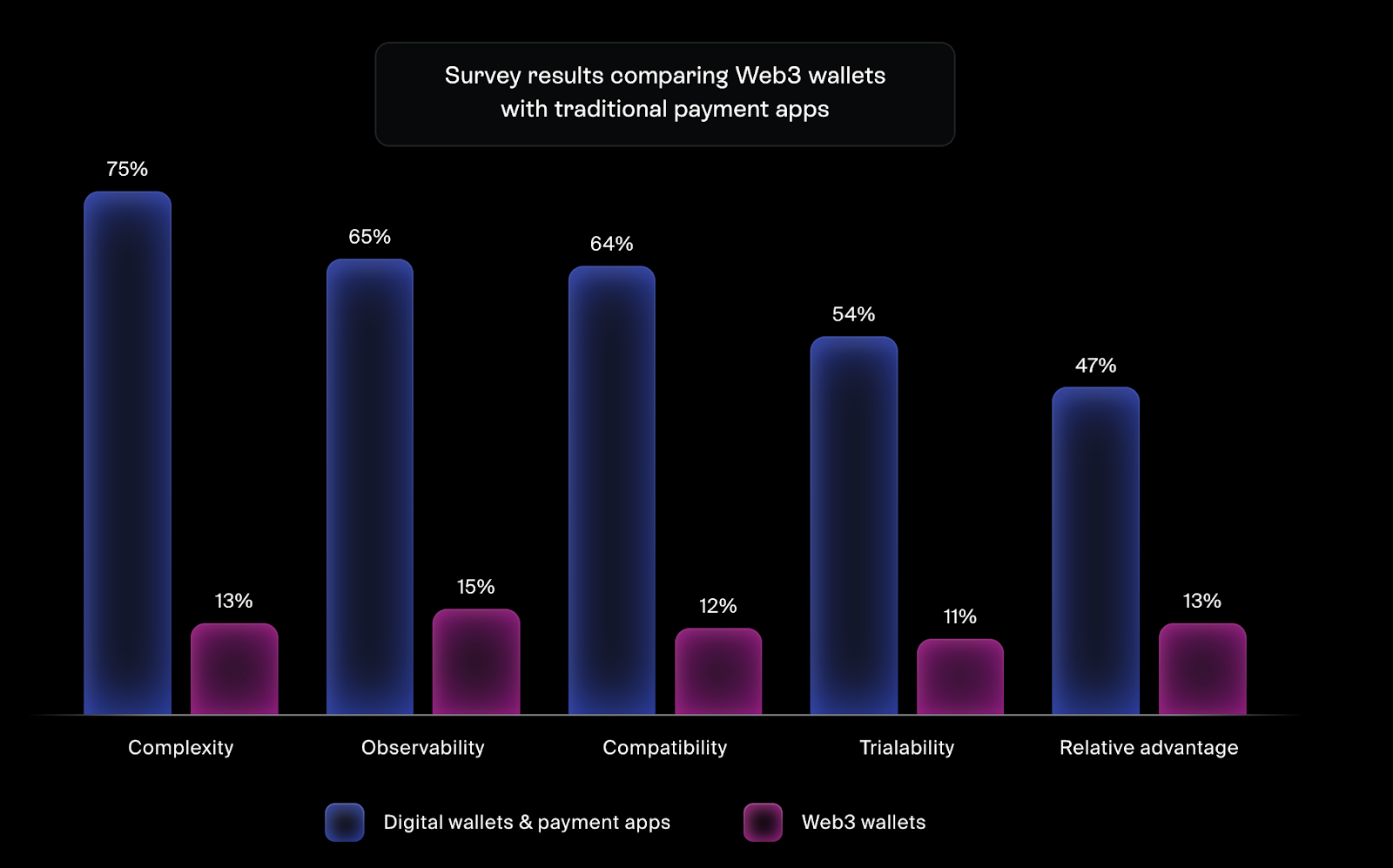

The macro numbers underline the shift. The global stablecoin supply has pushed past $300 billion, signaling that this is no longer a niche segment. Meanwhile, new research from Protocol Theory (in partnership with Mercuryo) shows that in the U.S. only 12 percent of adults feel web3 wallets fit their lives, compared with 64 percent for traditional digital wallets. That gap highlights both the remaining friction and the size of the opportunity to make self-custodial experiences as intuitive as the apps people already use every day.

Liquidity, Infrastructure and Market Movement

“The real battlefield today is infrastructure,” Firstov insists. “It does not matter which chain you use; what matters is that the rails work around the clock, globally.”

Recent reports back this up: payment volumes in B2B stablecoin settlements jumped from under $100 million per month in early 2023 to more than $3 billion monthly in early 2025. That kind of growth demands serious plumbing:

– Multi-chain settlement

– Real-time routing

– Robust global compliance and sanctions screening

– Institutional-grade custody and auditability

This is where examples like KlarnaUSD on Tempo are instructive. Tempo is purpose-built for payments, and Klarna is using it not as a marketing gimmick, but as a way to lower settlement costs for merchants and users at scale.

Meanwhile, institutions are waking up more broadly. Tokenized real-world assets (RWAs) could reach $2 trillion by 2028, with stablecoins acting as the underlying “plumbing” that moves value between markets and instruments. Firstov points to ETF-style flows, digital asset token (DAT) liquidity channels, and regulated rails as early previews of what is coming next.

The “Golden Era” for Users

“We are stepping into the golden era for users,” Firstov says. “The biggest financial institutions and blockchain platforms are now competing for distribution. As a result, users can access new financial products and markets, from stablecoins to tokenized assets, with fees near zero and almost no premium.”

That is a bold claim, but the numbers give it weight. Cost reductions of up to 99 percent have been reported in cross-border transfers using stablecoin rails compared to legacy correspondent banking. And as Klarna, PayPal, Stripe, Revolut and others deploy stablecoin-based rails, the playing field is shifting from early adopters to global scale.

In effect, users are getting the upside of institutional competition: cheaper transfers, faster settlement, and access to new products, while the heavy lifting happens behind the scenes in infrastructure.

Final Take

Arthur Firstov and his peers are operating at a rare inflection point. The merging of DeFi, stablecoins, and institutional finance signals a future where money moves anytime, anywhere, instantly, and cheaply.

What once looked like two separate universes, crypto on one side and banks and fintechs on the other, is rapidly becoming a single, programmable financial fabric. KlarnaUSD on Tempo is one concrete example; the next wave will bring more banks, more stablecoins, and more tokenized assets onto similar rails.

As the underlying infrastructure matures, liquidity deepens, and regulatory clarity expands, the promise of programmable money is no longer theoretical. The mission now is not just innovation but inclusion, ensuring that from retail users in Argentina to hedge funds in New York, everyone can plug into the same digital-asset economy.

The post Stablecoins in the Wild: When Fintech Discovers Programmable Money appeared first on BeInCrypto.

Binance has promoted co-founder Yi He to Co-CEO, joining Richard Teng in shared leadership as the company faces a $1 billion terrorism financing lawsuit and the aftermath of founder Changpeng Zhao’s criminal conviction.

This leadership change is a crucial moment for the world’s largest cryptocurrency exchange as it works to repair its reputation following years of regulatory scrutiny.

Dual Leadership Structure and Focus

Binance announced Yi He’s appointment as Co-CEO. She joins Richard Teng, and together they are tasked with strengthening the company’s regulatory standards and building trust in the digital asset sector.

Binance is stressing global regulatory compliance and a commitment to transparency.

Teng will focus on legal, regulatory, and administrative responsibilities, using his experience with regulated markets.

Yi He will concentrate on product development, retail operations, and user-oriented initiatives, ensuring smooth operations and customer satisfaction. She previously served as chief customer service officer at Binance.

While customer experience remains a strong focus, her influence has expanded its interactionfrom operational oversight to strategic leadership. She now helps shape Binance’s overall direction, not just how it interacts with users.

Yi He has publicly addressed her connection with CZ, stating her independence despite having children together.

Legal and Regulatory Hurdles After Trump Pardon

Binance’s executive changes come with ongoing legal challenges. The exchange faces a $1 billion federal lawsuit from victims and families of the October 7, 2023 Hamas attack. The suit, filed in North Dakota, lists Binance, CZ, and Gunagying “Heina” Chen as defendants.

Plaintiffs accuse Binance of facilitating funding to terrorist groups including Hamas and Hezbollah. The lawsuit alleges weak compliance, off-chain transactions, and operation of questionable accounts in Venezuela and Brazil.

The suit followed President Trump’s pardon of CZ in early 2025. Trump’s move overturned a four-month prison sentence CZ received after pleading guilty to inadequate anti-money laundering controls. The US Senate condemned the pardon in an October 2025 resolution.

According to CZ’s lawyer Teresa Goody Guillén, the pardon resulted from a formal review by the Justice Department and the White House. She called CZ’s case a compliance matter, not criminal fraud or money laundering.

In a November 2023 settlement, Binance agreed to pay $4.3 billion, and CZ paid a $50 million fine. He resigned as CEO and accepted restrictions on his industry involvement. Goody rejected claims of improper Binance-Trump connections, citing transparent blockchain records.

Amid questions about whether CZ could still influence Binance’s operations, Yi He stressed her professional independence, saying her “achievements and capabilities as co-founder are often overlooked” due to personal associations.

With dual leadership now in place, Binance faces the challenge of stabilizing its reputation while navigating one of the most consequential legal threats in its history.

Yi He’s Rise: From OKX to Binance’s Helm

Yi He entered the cryptocurrency arena in 2013 at OKX, where she worked in marketing and branding. While at OKX, she recruited CZ in 2014. Later, in 2017, CZ brought her into Binance as Chief Marketing Officer, a key moment for the new exchange.

As co-founder, Yi He has been crucial in establishing Binance’s culture and improving user experience. Her strategies fueled the expansion into spot trading, futures, and DeFi products. Binance now claims over 300 million users worldwide.

Yi He has strongly denied the terrorism financing accusations, highlighting that much criticism comes from traditional financial sectors. She maintains the company’s compliance and pointed to US Treasury statements showing crypto is rarely used by Hamas.

Nonetheless, the lawsuit provides examples allegedly linking Binance customers to illicit transactions. Plaintiffs say internal Binance messaging shows knowledge of suspicious funds. The pending civil trial in North Dakota could set important precedents for crypto exchange liability.

The post Yi He Appointed Binance Co-CEO Amidst Legal and Regulatory Challenges appeared first on BeInCrypto.

https://cryptonewsz.com/feed/

https://www.newsbtc.com/feed/

Ethereum fell more than 2% within 24 hours, sliding below $3,000 after losing its $2,900 support level. The drop triggered widespread liquidations, with around $500 million in long positions wiped out. Data shows that $79 million of the $106 million in ETH-focused contracts liquidated were long bets.

Trading activity spiked sharply during the decline, with daily volume rising 200% to $33.2 billion. The broader crypto market also contracted, falling nearly 1.2% and erasing an estimated $1100 billion in value within hours. Bitcoin, SOL, XRP, and DOGE followed similar downward moves.

Despite the volatility, some firms accumulated ETH during the downturn. BitMine Immersion Technologies increased its holdings by 96,798 ETH, diverging from the trend of companies reducing risk exposure.

Fusaka Upgrade Goes Live, Aiming to Boost Scalability

On December 3, Ethereum is set to activate its Fusaka upgrade, the network’s second major 2025 update. The upgrade aligns execution- and consensus-layer changes, introducing features that aim to improve Layer 2 and reduce costs.

A key component is PeerDAS, a data-sampling mechanism designed to reduce the bandwidth validators need to verify Layer 2 data. This system aims to cut validator bandwidth requirements by up to 85% and expand blob data capacity, potentially lowering Layer 2 transaction fees by 40–60%.

Fusaka also raises Ethereum’s block gas limit to 60 million, enabling more transactions per block, and introduces updates to the Ethereum Virtual Machine that streamline smart contract execution. These combined changes are expected to enhance the network’s transaction capacity.

Industry interest had been rising ahead of the upgrade. Major financial players, including Amundi and Fidelity, recently announced moves into tokenized products built on Ethereum, reflecting broader institutional activity across the network.

Can Ethereum (ETH) Recover From Oversold Levels?Ethereum (ETH) last traded at around $2,807, with technical indicators indicating continued bearish momentum. The MACD remains in negative territory, while the Relative Strength Index sits at 32, signaling oversold conditions.

Key support levels are at $2,700 and $2,500. A failure to hold these zones may deepen the downtrend, while a rebound could push ETH back toward $2,900–$3,000. Open Interest rose 4.3% after the decline, suggesting traders are reopening positions and preparing for higher volatility.

Whether the Fusaka upgrade can shift market sentiment remains uncertain, but its long-term scaling impact may play a role in Ethereum’s broader recovery.

Cover image from ChatGPT, ETHUSD chart from Tradingview

Bitcoin has turned itself around with a sharp surge to $92,000, unleashing a fresh wave of short liquidations on the derivatives exchanges.

Bitcoin Has Seen A Flash Recovery Back To $92,000

Bitcoin suffered a blow on Monday as its price slipped under $84,000, but just as quickly as it had crashed, the cryptocurrency has made a swift recovery on Tuesday.

With the asset’s price now floating above $92,000, its price has surged by more than 8% over the last 24 hours.

Like is usually the case, Bitcoin hasn’t been alone in this rally; the rest of the cryptocurrency market has also shot up alongside the number one digital asset. Some of the top altcoins have even managed to outperform BTC, with Ethereum (ETH) sitting in a profit of nearly 10% for the past day.

The fresh wave of volatility in the sector has triggered a liquidation squeeze in the derivatives market.

Crypto Liquidations Have Crossed $400 Million In Last 24 Hours

According to data from CoinGlass, the cryptocurrency market as a whole has suffered over $410 million in liquidations during the past day. “Liquidation” here naturally refers to the forceful closure that any contract undergoes after it has amassed a certain percentage of loss (as defined by the platform).

Considering that the price action in this window was majorly to the upside, it’s not surprising to see that short contracts made up for most of the derivatives flush.

As is visible in the above table, $348 million in short positions found liquidation in the last 24 hours, equivalent to about 85% of the total flush.

In terms of the individual symbols, Bitcoin, Ethereum, and Solana were the top three contributors to the liquidation event with $196 million, $95 million, and $18 million in positions, respectively.

Just $13 million of the Bitcoin liquidations involved long investors; the rest $182 million in liquidations struck the traders betting on a bearish outcome for the cryptocurrency.

A mass liquidation event like this latest one is popularly known as a squeeze. Today’s squeeze involved shorts in an extreme majority, so the event will be termed a short squeeze.

During a squeeze, a sharp swing in the price triggers a large derivatives flush, which only ends up feeding back into the price move. The amplified price swing then unleashes a further cascade of liquidations.

Such events aren’t a particularly rare sight in the cryptocurrency market, as assets tend to be volatile and many traders opt for significant amounts of leverage.