Financial RSS Feeds

https://www.investing.com/rss/news.rss

https://cointelegraph.com/rss

Technical charts highlight improving fundamentals in Bitcoin and select altcoins, but bears selling the range highs and softening investor sentiment threaten to snuff out the recovery.

The US president said he supported the GENIUS Act because it was "politically popular,” but added the main reason was in response to China.

https://www.coindesk.com/arc/outboundfeeds/rss/

https://cryptobriefing.com/feed/

Iran's central bank amassed $507M in USDT to dodge sanctions, using crypto tactics to access offshore liquidity.

The post Iran’s central bank used $500M in Tether to fight FX collapse and evade sanctions appeared first on Crypto Briefing.

Ethereum and Solana are expected to solidify their positions as leading blockchain platforms by 2026. General-purpose blockchain networks will find it challenging to compete with the established network effects of Ethereum and Solana. Solana is gaining favor among developers and consumers, positi...

The post Arnav Pagidyala: Ethereum and Solana will dominate by 2026, Solana’s community culture enhances its ecosystem, and Robinhood is set to surpass Coinbase | Bankless appeared first on Crypto Briefing.

https://bitcoinist.com/feed/

Fundstrat’s head of research, Tom Lee, has told investors to prepare for a rough opening to 2026 before conditions improve later in the year. He warned that political friction and tariff talk could trigger meaningful setbacks for both stocks and Bitcoin, even as blockchain and AI remain long-term strengths.

Tom Lee’s Call And The Near-Term Picture

Lee said a more dovish stance from the US Federal Reserve and the end of quantitative tightening set the stage for gains later on.

He put a possible market correction in the mid-teens range, estimating a pullback of about 15% to 20% at one stage.

He pointed to geopolitics — including renewed tariff threats — and rising political divides as brakes on an immediate, broad rally. Reports note he still expects a late-year rebound if policy eases and liquidity returns.

Reports say the White House’s selective support for certain industries could tilt which sectors lead the recovery.

2026 is shaping up to be similar to 2025:

– good fundamentals

– tariff escalations and White House picking “winners and losers” – political divisiveness – tailwinds from AI and blockchain BUT: dovish Fed now and QT over

And so a painful decline may lie ahead but we would… https://t.co/7Mp3rcOcP1

— Thomas (Tom) Lee (not drummer) FSInsight.com (@fundstrat) January 20, 2026

Deleveraging Still Hitting Crypto Liquidity

Lee argued that recent squeezes have left crypto markets fragile. Market makers have been weakened by repeated forced exits, and that has made price moves jumpier.

He also noted that a fresh Bitcoin all-time high would be an important signal that the market has worked through those stresses, though he didn’t repeat earlier extreme price targets in his latest remarks.

Reports stress the difference between a technical bounce and a move backed by wider adoption and deeper institutional flows.

Despite warnings that a painful decline may still unfold, some investors are not backing away entirely. Reports say parts of the market continue to view sharp pullbacks as buying chances rather than exit signals.

Even with uncertainty around tariffs and global politics, Lee and his camp believes disciplined dip buying — spread out over time — offers better odds than trying to time a perfect bottom while fear dominates headlines.

“And so a painful decline may lie ahead but we would ‘buy the dip'”, Lee said in an X post.

Reports indicate that more than $1.8 billion was liquidated over a 48-hour stretch as bitcoin lost ground.

Bitcoin sank to roughly $88,500 during the slide, and Coinglass data showed the bulk of wiped positions were longs — a sign that traders had been positioned for higher prices.

The selloff erased gains made earlier in the year and pulled crypto capitalization sharply lower, in one of the biggest drops since mid-November.

Featured image from Allrecipes, chart from TradingView

A decade-old report from the World Economic Forum (WEF) is resurfacing in the crypto space, highlighting early recognition of Ripple and XRP’s potential in the banking sector. Analysts say the document illustrates how decentralized networks like Ripple may allow institutions to settle payments faster and more directly in the future.

WEF Spotlights Ripple For Settlement Case Study

A crypto market analyst identified as ‘SMQKE’ on X recently revived a 2015 WEF report, sparking fresh discussions in the crypto community. The document explores how traditional banks could interact with emerging payment technologies, and it specifically mentions the company as a system capable of transforming interbank settlement.

The WEF report revealed that, as alternative payment methods, such as decentralized networks, grow in popularity worldwide, banks have the opportunity to integrate them into their services. By adopting these technologies, institutions can make it easier for customers to move value in and out of non-traditional networks while also exploring new financial products. Ripple is cited as an example of a protocol that could serve as one of these alternative rails.

Beyond customer use, these networks can also improve how banks operate internally. By leveraging non-traditional networks, banks could streamline processes and offer smoother, faster products and services. Ripple’s protocol, for instance, enhances this process by enabling real-time settlement between banks, eliminating the need for traditional clearinghouses or correspondent banks.

A case study in the WEF report focuses on German-based Fidor Bank, an online full-service bank that implemented the payment firm for its internal settlement operations in 2014. According to the World Economic Forum, broader adoption of Ripple could enable other banks to settle payments instantly with one another. This early example demonstrates how the crypto payments company was already seen as a practical tool for improving banking efficiency.

Though the WEF report is over a decade old, its insights remain relevant as financial institutions continue exploring blockchain-based payment solutions. Notably, this is not the first time the World Economic Forum has mentioned Ripple in its reports. In its May 2025 report, the international organization highlighted Ripple and the XRP Ledger (XRPL) as key technologies in the future of asset tokenization.

How XRP Fits In The Bank Settlement Scheme

As the native token of the XRP Ledger (XRPL), XRP is designed to serve as a digital bridge for fast, low-cost cross-border payments between financial institutions. By leveraging XRPL, Ripple enables banks and payment providers to settle transactions in seconds rather than days.

Due to its high throughput and ability to handle large transaction volumes with minimal effort, the XRP Ledger appears well-suited for the demands of modern banking. Its efficiency and speed have led many to compare Ripple to SWIFT, the long-standing messaging network used by banks worldwide for international transfers.

https://cryptoslate.com/feed/

At first glance, this looks like a story that lives on the back pages of a newspaper, Japanese government bonds with maturities that run so long they sound like a joke, 20 years, 30 years, 40 years.

If you own Bitcoin, you still end up in the blast radius.

Because when Japan’s long-dated bonds start to wobble, it is rarely just about Japan. It is about the world’s last big source of cheap money slowly turning into something more expensive, and what happens to every trade that quietly depended on that cheap funding.

The moment the mood changed

Japan has spent most of the last few decades as the place where money was close to free. That shaped global markets in a thousand small ways, even if you never bought a Japanese bond in your life.

Now that era is fading.

In December, the Bank of Japan lifted its benchmark rate to 0.75%, the highest level in roughly 30 years, part of a broader shift away from ultra-low policy that defined the country’s post-1990s playbook.

That move matters because Japan is not a small player. It is a funding hub. It is a reference point. It is the place global investors could point to when they wanted to borrow cheaply, hedge later, and hunt for returns somewhere else.

When that cheap anchor starts lifting, markets adjust, sometimes gently, sometimes all at once.

The signal people can’t ignore, long bonds are screaming

The fresh red flag is coming from the far end of Japan’s yield curve, the super-long bonds.

Japan’s 40-year government bond yield pushed above 4% for the first time, hitting around 4.2% as selling pressure built, and a recent 20-year auction showed weaker demand with a bid-to-cover ratio of 3.19, below its 12-month average.

Even if you do not live in bond world, that is the kind of detail traders circle with a thick marker. Auctions are where the market reveals how much real appetite exists for the debt being issued. When demand starts slipping at the long end, investors start asking harder questions about who the marginal buyer is going forward, and how much yield Japan will have to offer to keep funding itself smoothly.

A second datapoint makes the shift feel less like a blip. Japan’s 30 year government bond yield has climbed to about 3.46%, up sharply from about 2.32% a year earlier.

This is what a regime change looks like in slow motion, one auction, one basis point, one nervous headline at a time.

Why crypto ends up involved

Crypto loves to tell stories about being outside the system. The price still lives inside the system.

When rates rise, especially long-term rates, the entire market has to rethink what tomorrow’s cash is worth today. Higher yields raise the bar for every risky bet, stocks, private credit, venture, and yes, Bitcoin.

BlackRock put it bluntly in a recent note on crypto volatility, Bitcoin has historically shown sensitivity to USD real rates, similar to gold and some emerging market currencies, even if its fundamentals do not depend on any single country’s economy.

So when Japan’s moves ripple into global yields, Bitcoin can react before anyone finishes explaining the bond math on TV.

We have already seen a version of that movie lately. Global bonds sold off after hawkish comments from BOJ Governor Kazuo Ueda, and Bitcoin fell 5.5% in the same session, extending its monthly drop to more than 20%.

That is the bridge between “Tokyo bond auction” and “why did my crypto portfolio just bleed.”

The quiet mechanism behind the drama, the yen carry trade

There is a plumbing story here, and it matters more than the headlines.

For years, one of the simplest trades in global finance was borrowing in yen at very low rates, then putting that money to work in higher-yielding assets elsewhere. It does not always show up as a single obvious position you can point at; it shows up as a backdrop, as a source of steady demand for risk and yield.

When Japan tightens, that backdrop changes.

If the yen strengthens or funding costs rise, that carry trade can unwind. Unwinds tend to be messy because they are driven by risk limits, margin calls, and crowded exits.

The Bank for International Settlements studied a volatility burst and carry trade unwind in August 2024 and described how large FX carry positions were especially sensitive to spikes in volatility and were forced to unwind quickly.

You do not need to believe crypto is “part of the carry trade” to see the connection. You just need to accept that when leverage gets pulled out of the system, the most liquid risk assets often get sold first, and Bitcoin is one of the most liquid risk assets on the planet.

Japan’s bond story is also a political story, and politics moves yields fast

The long end of Japan’s curve is reacting to policy uncertainty too. The 40-year yield jump is tied to investor anxiety over a snap election and fiscal plans, the kind of political catalyst that can turn a slow grind into a sudden lurch.

Markets can tolerate a lot, they hate guessing games about issuance, spending, and the future buyer base for government debt.

If investors begin to suspect Japan will be leaning more heavily on the bond market, and doing so while its central bank is less willing to suppress yields, they demand more compensation. That is what a rising long bond yield often represents, the market asking to be paid more for time and uncertainty.

The crypto angle that lasts longer than today’s price action

The durable question is simple, does Japan’s shift keep global financial conditions tighter than markets are expecting.

If the answer is yes, crypto’s upside gets capped, rallies become choppier, leverage becomes more fragile, and every risk flare-up feels sharper.

If the answer is no, and Japan’s transition stays orderly, then the bond market stops being the main character, and Bitcoin goes back to trading its usual mix of liquidity, positioning, and narrative.

There are a few forward paths worth mapping, and none of them require pretending anyone can predict a Bitcoin candle.

Three scenarios worth watching next

1) Orderly normalization

Japan continues raising rates gradually, the bond market absorbs it, auctions stay decent, yields stay high but stop behaving like a panic meter.

In this world, the pressure on crypto shows up as a steady headwind. Higher risk-free returns compete with speculative appetite. Bitcoin can still run, especially if other forces turn supportive, but the market keeps looking over its shoulder at real yields.

2) Auction stress turns into a global duration tantrum

More weak auctions, more headlines about demand, more volatility at the long end.

Global yields jump as relative value traders adjust and as investors worry about repatriation flows, then equities and crypto take the hit.

The recent example is already on the tape, global bonds slid on hawkish BOJ signals, and Bitcoin dropped 5.5% on the day.

This scenario tends to look like forced selling. Fundamentals become background noise.

3) Policy response calms the market

Japan’s officials push back hard against disorderly moves, issuance choices shift, bond buying operations, and guidance are used to cool volatility, and yields stop surging.

That can loosen global conditions at the margin, simply by removing a source of stress. Bitcoin responds the same way it often does when the market senses less pressure from rates and funding.

The point is not that Japan “helps crypto,” the point is that global liquidity expectations shift.

The simple dashboard, what to watch if you want the earliest tells

If you want to stay ahead of the story, you do not need twenty indicators. You need a handful.

- Japan’s long bond yields, especially the 30-year and 40-year.

- 20-year and 30-year auction strength, including bid-to-cover ratios.

- USDJPY, because carry dynamics often surface there first.

- US real yields, because Bitcoin has a history of reacting to them.

- Volatility spikes, because carry positions can unwind fast when vol rises.

Where stablecoins fit, the overlooked side channel

This part gets missed in a lot of crypto coverage.

Crypto has its own internal money system, stablecoins act like the cash register. When monetary policy shocks hit traditional markets, stablecoin liquidity can move too, which changes crypto market conditions even if on-chain narratives stay the same.

A BIS working paper on stablecoins and monetary policy found that US monetary policy shocks drive developments in both crypto and traditional markets, while traditional markets do not react much to crypto shocks in the other direction.

That supports the broader point that crypto is downstream of macro funding conditions more often than it wants to admit.

Why this “Japan story” keeps showing up in Bitcoin’s chart

Somewhere in Tokyo, there are insurers and pension managers staring at the same problem everyone is staring at, yield has returned, and it comes with volatility attached.

Somewhere else, there is a crypto trader in New York or London watching Bitcoin chop sideways, wondering why a move in Japanese bonds is pulling on their screen.

This is why.

Japan is changing the price of money after decades of holding it down. That adjustment is reaching into every corner where leverage and risk live, and crypto sits right there, liquid, global, always open, always ready to react.

If Japan’s bond market stays calm, crypto gets a cleaner runway.

If Japan’s long end keeps throwing off stress signals, the market is going to keep learning the same lesson, Bitcoin trades on the future, and the future is priced in yields.

The post Bitcoin is in the blast radius after Japan’s bond market hit a terrifying 30-year breaking point appeared first on CryptoSlate.

Canada's Prime Minister, Mark Carney, walked onto the World Economic Forum's Davos stage yesterday and said the quiet part out loud.

The rules-based order, the thing leaders love to invoke when they want the world to behave, is fading.

Carney called it a “pleasant fiction.”

He said we are living through a “rupture.”

He said great powers are using integration as a weapon, tariffs as leverage, finance as coercion, and supply chains as vulnerabilities to be exploited.

Then he reached for Václav Havel’s famous “greengrocer” from The Power of the Powerless, the shopkeeper who hangs a sign reading “Workers of the world, unite!” not because he believes it, but because he knows the ritual matters more than the words. It’s Havel’s shorthand for life under a system where everyone performs loyalty in public, even as they quietly recognize the lie.

He told the room, “It is time for companies and countries to take their signs down.”

The Davos audience cheered and clapped in response.

Perhaps, one can argue that they are trained to nod along. This week, they have extra reasons.

The talk around town has been about tariffs and coercion, and whether allies are about to be treated like revenue lines.

The mood is tied to President Trump escalating pressure around Greenland and tariff threats against European partners, a story that keeps resurfacing across conference chatter and the news cycle.

Carney’s slot was listed as a “Special Address” in the WEF run-up. His message landed in a room already primed for it.

Here is the part crypto people should not miss: when geopolitics becomes transactional in public, money stops being background infrastructure and starts feeling like a border.

That shift changes what people pay for.

It changes what investors store value in. It changes what counts as a safe option.

Bitcoin sits right in the middle of that feeling.

Not because it suddenly becomes a global settlement rail for trade invoices. It probably does not.

Not because it replaces the dollar in a clean, straight line. It almost certainly does not.

Bitcoin matters because it offers an option: a credible outside asset that is hard to block, hard to rewrite, and hard to gate behind somebody else’s permission.

In a stable world, that sounds ideological. In a rupture world, it starts to sound like risk management.

Carney even used the language of risk management. He said this room knows it. He said insurance costs money, and the cost can be shared.

Collective investments in resilience are cheaper than everyone building their own fortresses.

That is the Davos version of a truth every investor learns early: concentration risk feels fine until the day it does not.

The human part of this story, the moment you realize access can be conditional

Most people do not wake up wanting a new monetary system.

They wake up wanting their salary to clear, their bank transfer to arrive, their business to keep trading, and their savings to keep meaning something next year.

They also have a moment, sometimes it is a headline, sometimes it is a blocked payment, sometimes it is a currency shock, when they realize access can be conditional.

Carney’s speech is basically a map of how those moments multiply.

He talked about tariffs used as leverage.

He talked about financial infrastructure as coercion.

He talked about supply chains exploited as vulnerabilities.

“Over the past two decades, a series of crises in finance, health, energy and geopolitics have laid bare the risks of extreme global integration. But more recently, great powers have begun using economic integration as weapons, tariffs as leverage, financial infrastructure as coercion, supply chains as vulnerabilities to be exploited.

You cannot live within the lie of mutual benefit through integration, when integration becomes the source of your subordination.”

That is what a “rupture” feels like in everyday terms. Your costs move because of a speech in another capital. Your suppliers disappear because of a sanctions package. Your payment route gets slower because a bank somewhere decides your jurisdiction is riskier this month.

Even if you never touch crypto, that environment changes the way you value optionality.

Bitcoin is optionality with teeth.

It is not magic.

It does not make geopolitics disappear.

It does not exempt anyone from laws.

It does not stop volatility.

It does one simple thing: it exists outside most of the chokepoints that make modern finance such an effective tool of state power.

That is why this moment matters more than a single Davos speech.

Two Bitcoins show up in markets, the insurance one, and the liquidity one

If you want to talk about Bitcoin under a changing world order without slipping into slogans, you have to admit something that makes true believers uncomfortable.

Bitcoin has two personalities in markets.

- One is the insurance asset. People buy it because they worry about the rails, the long term, the shape of the world, and the rules. They want something that can move across borders as information.

- The other is the liquidity asset. In sudden shocks, Bitcoin trades like the thing that gets sold when people need dollars now.

That second personality is why “rupture” headlines can produce weird price action. The macro story gets scarier, and Bitcoin drops anyway.

The immediate response is a dollar grab: credit tightens, leverage unwinds, risk gets sold first, and questions get asked later.

There's a sequence: squeeze first, repricing later.

Tariffs as leverage, why the first wave can hurt Bitcoin, then help its story

Tariffs are more than a tax; they are a signal.

They tell markets the temperature of international relationships, they tell companies how stable their cost base will be, and they tell central banks how messy inflation might get.

This is where Carney’s argument about weaponized integration connects directly to Bitcoin’s near-term and long-term path.

If the latest tariff threats escalate into real measures, companies reprice supply chains, consumers see price pressure, and policymakers face uglier trade-offs.

The JPMorgan framing around tariffs is a reminder that they are not just politics. They are a macro variable that shows up in growth, inflation, and confidence.

In the first phase, markets often do what markets do. They go defensive, they prefer cash, they prefer the most liquid collateral, and they chase dollars.

Bitcoin can get dragged lower with everything else.

Then the second phase arrives.

Businesses and households realize this is not a one-off. They start paying for resilience. They diversify, build redundancy, and look for assets that sit outside the obvious pressure points.

That is where Bitcoin’s insurance narrative gains weight. Not everyone becomes a Bitcoin maximalist because they read the Bitcoin Whitepaper, but because a larger share of capital starts treating optionality as worth paying for.

Financial infrastructure as coercion, stablecoins live on the rails, Bitcoin sits outside them

Carney’s line about financial infrastructure matters because it points to the part of the crypto stack most people misunderstand.

Stablecoins are crypto, and stablecoins are also the dollar’s long arm.

They move fast, they settle cheaply, and they make cross-border value transfer easier. They also live inside an ecosystem of issuers, compliance, blacklists, and regulatory chokepoints.

That is beyond a moral judgment. It is the design, and it is also why stablecoins can scale.

In a world where financial infrastructure becomes more openly coercive, stablecoins can feel like a superhighway with more toll booths.

Bitcoin feels like a dirt road that still gets you out. That distinction becomes more important as countries and blocs start building their own resilience stacks.

Carney called it variable geometry: different coalitions for different issues. He talked about buyers’ clubs for critical minerals, bridging trade blocs, and AI governance among like-minded democracies.

You can see the same logic in the policy world around defense procurement, including Europe’s SAFE push.

It is about capacity, coordination, and optionality. Crypto will get pulled into that same orbit.

Some blocs will prefer regulated, surveilled rails. Some will build their own. Some will restrict foreign dependencies. Some will quietly keep a foot in every camp.

Bitcoin’s role in that environment is leveraged through existence.

If you can exit, even imperfectly, coercion becomes costlier to apply.

Middle powers, “third paths,” and why Bitcoin’s biggest impact might be psychological

Carney’s speech is a manifesto for middle powers: countries that cannot dictate terms alone, and that get squeezed when great powers turn the world into a bilateral negotiation.

He said negotiating alone with a hegemon means negotiating from weakness. He said middle powers have a choice: compete for favor, or combine to create a third path.

That is a geopolitical argument.

It also rhymes with what Bitcoin represents in finance.

Bitcoin is a third-path asset.

It is not the hegemon’s money. It is not a rival’s money. It is not a corporate ledger. It is not a treaty.

That matters most when trust is thin and alignment is messy, when alliances feel conditional, and when sovereignty sounds less like a principle and more like something you have to finance.

Carney stood with Greenland and Denmark in his remarks.

He opposed tariffs over Greenland, and called for focused talks on Arctic security and prosperity.

You do not have to take a view on Greenland to see the pattern. Trade tools are being discussed as leverage among allies in public.

When that happens, every CFO, every pension committee, every sovereign fund, and every household with savings gets a little more serious about tail risks.

That is what matters for us, the slow shift in what feels safe.

US President Donald Trump, speaking today, asserted that he “would not use force” to take Greenland but reiterated that he does still want to purchase the “big block of ice.” He reaffirmed that he expects Europe to support the purchase for world security reasons, but if it refuses, “the US will remember.”

Three forward scenarios for Bitcoin by 2030, “managed fragmentation,” “tariff spiral,” “rails fracture”

Carney called this a rupture.

He also warned against a world of fortresses and argued for shared resilience. Those are two different futures, and Bitcoin’s path looks different in each.

1) Managed fragmentation

Blocs form, standards diverge, and trade routes adjust. Coercion exists, but it stays bounded because everyone realizes escalation is expensive.

Bitcoin in this world trends upward as a portfolio's final insurance policy. Volatility remains.

Correlation to liquidity cycles remains. The structural bid grows because the world keeps paying for optionality.

2) Tariff spiral and dollar squeeze

Tariffs escalate, and retaliation follows.

Inflation uncertainty rises, central banks stay tight longer, and risk assets get hit. A dollar squeeze shows up.

Bitcoin here can look disappointing in the moment.

Price falls with leverage unwinds, narratives get mocked, then policy eventually shifts, liquidity returns, and the underlying reason people want an exit option becomes stronger.

3) Rails fracture

Financial coercion expands. Secondary sanctions and controls become more common. Cross-border payments get more politicized.

Some countries build parallel settlement stacks, some companies reroute exposure, and everyone pays more for friction.

Bitcoin’s insurance value is highest in this world because the cost of conditional access is highest.

Stablecoins still matter for commerce. Bitcoin matters for reserve optionality, for portability, and for the ability to move value when doors close.

This is also where regulation gets harsher. A fractured world tends to be a more suspicious world, and the easiest thing for states to tighten is anything that looks like capital flight.

Bitcoin’s upside here exists alongside higher enforcement pressure. That tension becomes part of the story.

The quiet tell, even Davos is arguing about resilience, not efficiency

The old globalization story was efficiency: just-in-time supply chains, single-point optimization, and frictionless capital.

Carney’s speech is about resilience, redundancy, shared standards, and variable coalitions.

And it is happening at Davos, the temple of integration. That is the tell. Even the “rules-based order” language is changing in public.

The WEF theme is still cooperation. The framing is still dialogue. And the agenda is full of resilience talk because the room knows the bargain Carney described is under strain.

Outside Davos, the news cycle reinforces the point.

The UN Security Council is still extending reporting around Red Sea attacks, reminding everyone that shipping lanes are strategic terrain. The UN record captures how persistent that risk remains.

The Venezuela tanker seizures covered by AP show hard power and economic control blending in the Western Hemisphere, too.

Le Monde’s report on a US-Taiwan deal around advanced chips and tariffs shows how industrial policy and trade are merging, even in sectors that used to be treated as pure economics.

Bitcoin does not cause any of this.

And it does not solve it.

It becomes more relevant because the world is changing around it.

What to watch next, five signals that the rupture thesis is becoming investable

A watchlist to remain alert:

- Tariff implementation dates, and whether threats turn into policy. The Greenland-linked tariff reporting is one real-time test.

- Signs of allies building redundancy stacks: defense procurement coordination, trade bridges, critical-minerals buyers’ clubs, and the policy plumbing that makes “shared resilience” real.

- Cross-border payments politics. Any move that makes access more conditional increases demand for outside options, and also increases pressure on crypto on-ramps.

- Energy and shipping risk. The Red Sea remains a live variable.

- Bitcoin’s behavior during stress. If it sells off first and rebounds when policy shifts, that fits the two-personality model. If it starts holding up during shocks, that signals the insurance bid is getting deeper.

The point Carney made, applied to Bitcoin

Carney’s speech was a warning about pretending, about “living within a lie,” about acting like the old system still works as advertised.

For Bitcoin, the parallel is simpler. People have treated money as plumbing for decades. They are starting to treat it like a geopolitical instrument again.

In that world, Bitcoin becomes easier to understand.

Not as a promise. Not as a religion. And not as a straight-line trade.

It becomes what it has always been underneath the hype: a volatile, imperfect, stubborn form of financial optionality.

A way to keep one window open when more doors start coming with terms and conditions.

The post Bitcoin is now your only lifeboat as Canada says the current world order is merely a “pleasant fiction” appeared first on CryptoSlate.

https://ambcrypto.com/feed/

Solana Mobile, Trump Media and Pump.fun have also announced new projects and milestones.

Solana Mobile, Trump Media and Pump.fun have also announced new projects and milestones. What's next for USOR after a 98% crash?

What's next for USOR after a 98% crash?https://beincrypto.com/feed/

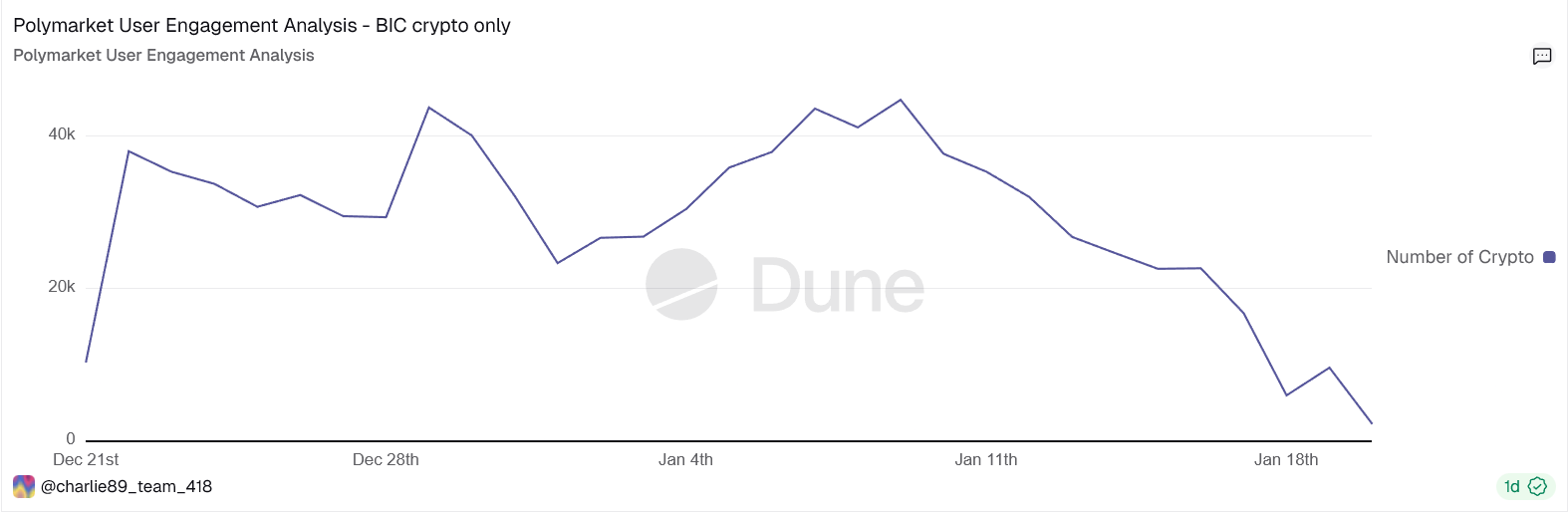

Crypto traders are still active on prediction markets, but fewer are willing to take risk. New on-chain analysis from BeInCrypto shows that high-conviction crypto trading on Polymarket has cooled steadily since early January, after peaking twice in late December and the first week of the new year.

The data does not track casual users or passive viewers. Instead, it focuses on wallets that actively placed orders and provided liquidity on crypto-related markets, offering a clearer signal of trader sentiment.

High-Conviction Crypto Activity Peaked, Then Faded

BeInCrypto analysts observed daily maker activity on Polymarket over the past 30 days, filtering only crypto-tagged markets such as Bitcoin and Ethereum price outcomes, meme coins, NFTs, and airdrops.

Because the dataset counts makers only, it captures wallets actively risking capital, not traders simply filling existing orders. The results show two clear engagement waves.

The first occurred in late December, when daily active crypto makers climbed into the high-30,000 range. The second, and stronger, wave came in early January, with activity peaking around 40,000–45,000 wallets.

However, after January 9, the trend reversed. Daily crypto maker activity declined consistently through mid-January, falling back toward the low-20,000 range before dropping sharply at the end of the window.

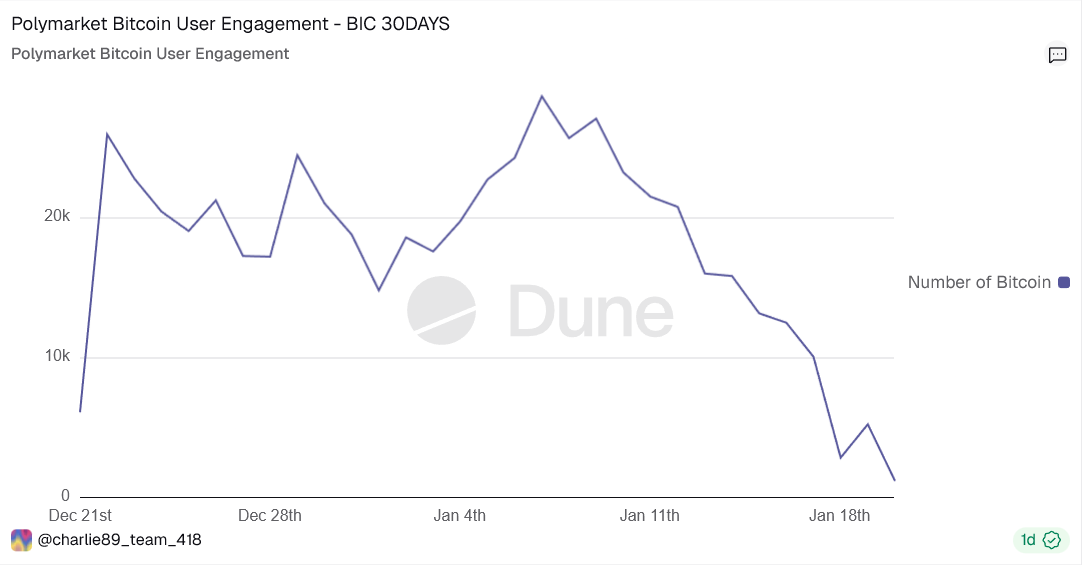

Bitcoin Engagement Confirms the Broader Cooldown

Bitcoin-focused markets followed the same pattern.

A separate Dune chart tracking Bitcoin-only maker wallets shows strong engagement in late December and early January, followed by a persistent decline.

By January 18, the number of active Bitcoin makers fell to 2,875 wallets, down sharply from the five-figure levels seen earlier in the period.

This confirms the slowdown was not limited to niche crypto bets or altcoin narratives. The pullback extended to Bitcoin, the platform’s most liquid and consistently traded crypto category.

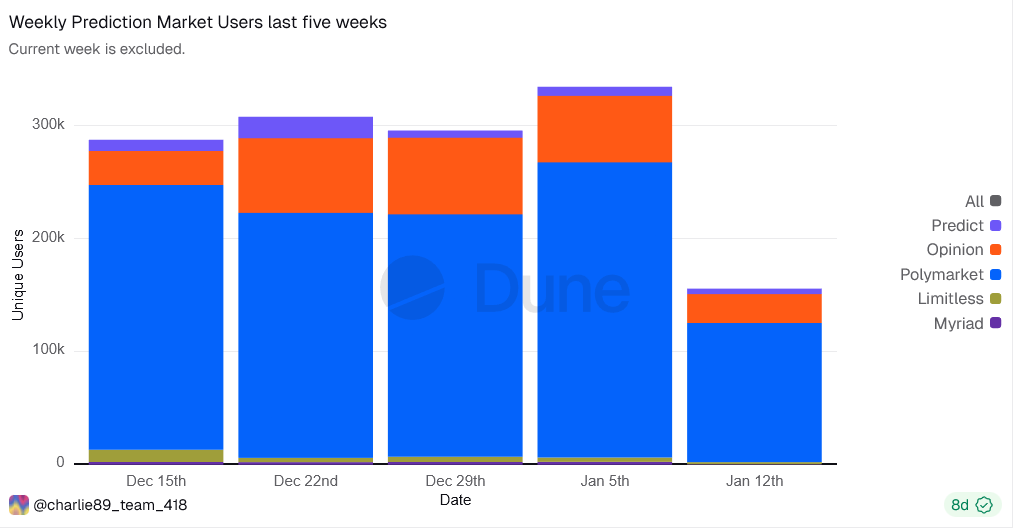

Weekly Data Shows Polymarket Dominance, but Shifting Behavior

Weekly data across prediction market platforms adds context. Polymarket continues to account for the majority of weekly prediction market users, dwarfing smaller competitors in absolute terms.

During peak weeks in late December and early January, total weekly users across platforms reached the high-200,000s to low-300,000s.

Yet while total users remained elevated, the composition of activity changed. Maker participation in crypto markets declined even as overall platform engagement stayed relatively high.

This divergence suggests traders did not leave prediction markets altogether. Instead, they became more selective about when and how much capital they were willing to commit.

Liquidity Providers Step Back Before Users Disappear

The maker-only filter is critical to understanding the signal.

Liquidity providers tend to pull back before broader user numbers fall. When volatility drops or narratives lose momentum, traders often stop posting new orders while still monitoring markets or trading opportunistically.

That pattern appears clearly in the data. Crypto maker activity declined steadily after early January, suggesting a cooling of conviction rather than a sudden collapse in interest.

This behavior mirrors dynamics seen in DeFi and derivatives markets, where funding rates, open interest, and liquidity depth often weaken before spot volumes follow.

Taken together, the data point to a clear conclusion.

Crypto traders have not abandoned prediction markets. However, fewer are willing to provide liquidity and take directional risk compared to early January.

In plain terms, prediction markets are signaling a risk-off shift in crypto sentiment, visible first among high-conviction traders.

The post Crypto Traders are Quietly Stepping Back From Prediction Markets appeared first on BeInCrypto.

Zcash has officially confirmed a bearish breakdown. The price lost a major long-term trendline and activated a technical pattern that points to a potential 34% downside move. Under normal conditions, that kind of confirmation attracts aggressive sellers. Instead, the opposite happened. Large holders stepped in, exchange balances dropped sharply, all while the leverage positioning became heavily skewed to the short side, with bears expecting more downside.

That combination rarely appears during clean breakdown moves. It usually appears when the market is setting up to punish one side of the trade.

A Confirmed Breakdown After Losing a Critical Trend Level

From a technical perspective, the breakdown is real.

Zcash is still down roughly 55% from its early November peak near $745. More importantly, the ZEC price has now lost the 100-day exponential moving average (EMA). An EMA is a trend indicator that gives more weight to recent prices, making it useful for spotting shifts in market direction.

This level mattered before. In early December, Zcash briefly dipped below the 100-day EMA, then reclaimed it the next day. That reclaim triggered a sharp 71% rally. This time, the level has not been reclaimed yet, keeping the broader trend pressure bearish.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

On the 12-hour chart, Zcash also confirmed a head-and-shoulders breakdown on January 20. This is a reversal pattern that forms after an uptrend and typically signals a deeper move lower once the neckline breaks. The measured downside from this structure points to a roughly 34% decline, which is now supposedly active.

Technically, bears have what they want. The reaction afterward is what makes this setup unusual.

Buying Appears After Weakness, Not Before It — But Why

On-chain data explains why the breakdown response matters.

Exchange balance tracks how many coins are held on trading platforms. Rising balances usually suggest selling pressure, while falling balances suggest coins are being moved into private wallets for holding.

During the breakdown itself, exchange balances rose, showing active selling. That fits the bearish narrative.

Then the behavior flipped.

Over the next 24 hours, exchange balances dropped by roughly 17%. At the same time, large holders increased exposure. Whale wallets added about 2.44% to their holdings, while the top 100 addresses (mega whales) expanded their positions by nearly 4%.

This is accumulation after confirmation, not speculative dip buying ahead of it.

When large holders buy into confirmed weakness, they are usually positioning for either a fast reclaim of key levels or a volatility event driven by forced liquidations. Derivatives data strongly supports the second scenario.

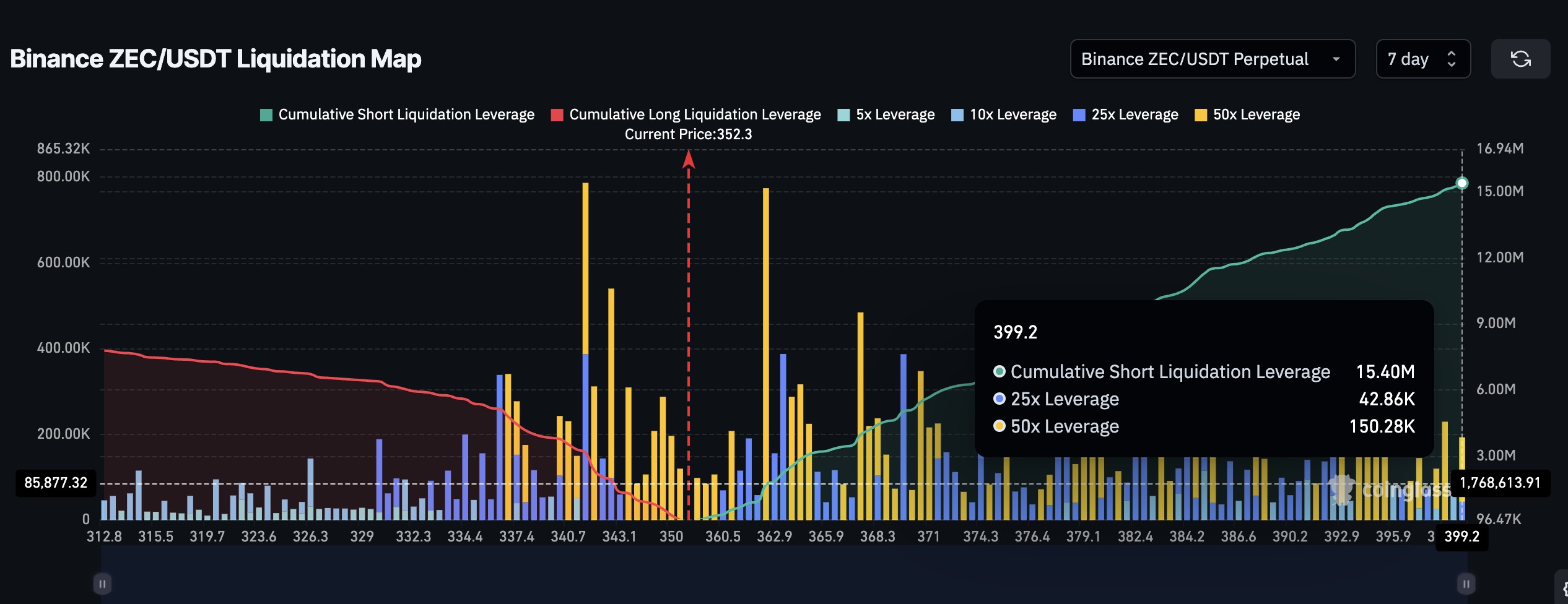

Short Positioning Creates the Conditions for a Squeeze With Key Zcash Price Levels In Focus

The liquidation map shows where leveraged traders would be lose out if the price moves against them.

Liquidation levels represent price zones where traders using leverage would be automatically closed by exchanges. When many positions cluster on one side, price moves toward those levels can accelerate quickly.

For Zcash, short liquidation exposure over the coming days sits near $15.4 million, while long liquidation exposure is closer to $7.8 million. That means the market is heavily tilted toward short bets, nearly a 2:1 short bias.

This imbalance matters. Zcash does not need a trend reversal to cause damage. Even a moderate bounce can begin liquidating short positions, forcing buy orders that push the price higher.

A move into the $375 to $400 range would trigger most short positions, trapping the bearish side of the market. A push above $450 materially weakens the bearish structure. Also, if the ZEC price manages to reclaim the 100-day EMA, history shows upside can expand rapidly rather than stabilize slowly.

The trap theory fails if the price continues lower. A sustained break below $329 on the 12-hour timeframe keeps the 34% downside path intact and opens the door toward $255 and even lower.

The post Zcash’s 34% Breakdown Triggered — Why It Could All Be A Setup To Trap The Bears appeared first on BeInCrypto.

https://cryptonewsz.com/feed/

https://www.newsbtc.com/feed/

XRP is taking a decisive step toward institutional relevance as Flare Networks unveils new infrastructure designed to support enterprise-grade financial use cases. For years, XRP has been recognized for its speed and efficiency in cross-border payments, and XRP has often been discussed as a liquidity asset, but with limited programmability and on-chain utility. Flare’s latest move changes that equation, unlocking new layers of functionality that position XRP as more than just a settlement token.

How Flare Expands XRP Smart Contract Capabilities

Flare Networks is taking concrete steps to activate XRP for institutional-grade financial infrastructure. In a recent Genfinity interview that was revealed on X, the Flare Networks team breaks down how its infrastructure is enabling traditionally idle digital assets, starting with XRP, to participate in a programmable financial system.

The conversation focuses on execution rather than theory. This includes bringing FXRP live, integrating directly with wallets, custodians, exchanges, and removing technical friction so that participation won’t require users to manage on-chain technical complexity. Flare’s strategy is not about an isolated pilot experiment, but about building durable infrastructure that can scale across different users, assets, and environments.

A core design principle is risk abstraction at the protocol level, through platforms like Firelightfi, where exposure is structured, collateralized, allowing larger participants to engage with clearer parameters, predictable outcomes, and stronger operational safeguards.

This approach shifts participation from speculative usage toward structured financial activity. The discussion makes it clear that XRP is the first implementation, not the final destination. However, the Flare broader objective is to activate multiple digital assets within a unified framework that prioritizes usability, security, and seamless integration into existing financial workflows. As highlighted in the Genfinity interview, this approach reflects the current stage of digital asset infrastructure, transitioning from experimentation toward real-world execution.

What This Means For The Future Of XRP And Tokenized Media

Crypto analyst Skipper_xrp has mentioned that SBI Group President Yoshitaka Kitao emphasized that Ripple is no longer just building products; it is creating a full-stack financial ecosystem with XRP and RLUSD integrated into every layer of its infrastructure.

The vision is already moving into execution as Ripple Labs has confirmed its collaboration with major Japanese financial institutions to launch a high-profile innovation program aimed at professionalizing the XRP Ledger ecosystem.

Meanwhile, BXE Token is preparing to debut on a US-regulated exchange with more than 12 million users and over $900 billion in annual trading volume, alongside compliance coverage across 49 countries. At the same time, decentralized media platforms are preparing for the US market.

Bitcoin tumbled sharply this week and erased the gains it had made in 2026. Reports from CoinGlass show that over the past 24 hours, 167,513 traders were forced out of their positions, with total liquidations reaching $857 million, with most of those losses coming from long bets. The price slid below the key $88,000 area on major exchanges as traders were forced out of leveraged positions.

Liquidations And Quick Drop

According to CoinGlass and market trackers, the liquidations were concentrated in long positions, which amplified the fall and made the move faster than a simple sell-off would have been. Crypto market value fell by hundreds of millions over the same short span.

Markets Turned Risk-Averse As Tariff Threats Spread

Reports note that renewed tariff threats from US President Donald Trump toward some European countries set off a fresh “Sell America” trade, which pushed investors away from US assets and toward safer bets.

Stocks fell and the dollar weakened. At the same time, traders were watching big moves in Japan’s bond market, where yields jumped sharply, increasing pressure on global liquidity. Those bond moves are important because they can force carry trades to unwind, pulling money out of risk assets — including crypto.

The sell-off did not happen for only one reason. Reports point to a mix of political shocks, bond-market stress, and a wave of forced liquidations as the main drivers. As cash flowed into safe havens, gold surged to fresh highs while crypto lost ground. Many investors treated Bitcoin like a risky asset in this episode, selling it to cover losses or margin calls elsewhere.

Different trackers gave slightly different figures on total market losses and exact liquidations over 24 and 48 hours. That is normal when markets move fast and data is pulled from different exchanges and windows. Still, the broad picture was clear: a fast, leveraged unwind sent prices lower and erased the year’s gains for Bitcoin.

Markets Will Watch Liquidity And DiplomacyLooking ahead, investors will likely watch three things closely: moves in global bond markets, any escalation or de-escalation around the tariff threats tied to Greenland, and whether forced selling slows. If liquidity conditions calm, risk assets can recover more easily. If they keep tightening, the pressure on crypto and stocks could persist.

Featured image from Pexels, chart from TradingView