Financial RSS Feeds

https://www.investing.com/rss/news.rss

https://cointelegraph.com/rss

Crypto traders often view negative funding rates as a strong buy signal, but several data points suggest ETH investors have good reasons to remain risk-averse.

Circle said digital financial infrastructure, including stablecoins, can save 20% of the cost of delivering humanitarian aid.

https://www.coindesk.com/arc/outboundfeeds/rss/

https://cryptobriefing.com/feed/

Tokenizing ETF shares could revolutionize asset management by enhancing efficiency and adaptability while ensuring regulatory compliance.

The post F/m Investments seeks SEC permission to tokenize ETF shares appeared first on Crypto Briefing.

Strive's strategic focus on Bitcoin investment and debt reduction could enhance its market position and influence in the crypto sector.

The post Vivek Ramaswamy’s Strive plans to raise $150M in preferred stock sale to buy Bitcoin and repay debt appeared first on Crypto Briefing.

https://bitcoinist.com/feed/

Bitcoin slipped below the $90,000 level as global markets reacted to rising macroeconomic tension between the United States and the European Union. Investors are closely watching the latest trade headlines, as renewed tariff threats increase uncertainty around global growth, corporate earnings, and inflation dynamics. When friction between major economies escalates, risk appetite typically fades, and crypto tends to feel the impact fast as traders reduce exposure and cut leverage.

According to an analysis by XWIN Research Japan, Bitcoin’s recent weakness fits a broader pattern that has been developing since 2025. The report argues that the Trump administration’s renewed tariff push has acted as a consistent downside pressure for BTC, mainly because tariffs influence multiple pillars of the macro environment at once. Higher tariffs can squeeze company margins, disrupt supply chains, and push inflation expectations higher, which complicates the outlook for interest rates and monetary policy.

In this environment, Bitcoin has continued to behave more like a macro-sensitive risk asset than a defensive hedge. Instead of attracting safe-haven flows, BTC has often moved in sync with equities during trade-driven risk-off waves. As a result, even brief bursts of bullish momentum have struggled to hold when economic uncertainty rises and capital rotates into safer positioning.

Tariff Risk Keeps Bitcoin Tied to Macro Conditions

The XWIN Research Japan report explains that several Bitcoin pullbacks between 2025 and 2026 aligned with periods of rising economic uncertainty driven by tariff hikes and trade frictions. During these episodes, BTC declined alongside equities, reinforcing that the market still treats Bitcoin as a macro-sensitive risk asset rather than a defensive hedge. Instead of decoupling during stress, Bitcoin often reacts like a high-beta instrument when traders rush to reduce volatility in their portfolios.

Economic risk tends to hit Bitcoin quickly because investor behavior adjusts fast. As uncertainty around growth and interest rates increases, capital typically shifts toward short-term protection. In that process, Bitcoin is frequently viewed as a liquid asset that can be sold temporarily to lower portfolio risk, rather than a long-term store of value that benefits from risk-off flows. This dynamic can amplify downside moves even when long-term fundamentals remain intact.

Exchange Netflow provides a supplementary layer of evidence. During correction phases, brief spikes in exchange inflows often appear, consistent with tactical repositioning and short-term profit protection. However, these inflows have not persisted, suggesting the absence of sustained structural selling pressure.

For now, the base scenario remains that tariff-driven economic risk is weighing on Bitcoin. If exchange inflows become sustained and supply-demand conditions weaken further, that assessment would need to be reassessed.

BTC Holds Its Ground After Breaking Below $90K

Bitcoin is trading around $88,800 on the weekly chart after a sharp selloff that briefly pushed price below the $90,000 psychological level. This drop marks a clear shift in momentum, as BTC failed to hold the mid-range structure that supported price action throughout the late-2025 consolidation phase. The weekly candle shows heavy downside pressure, with sellers rejecting attempts to stabilize above $92,000 and forcing a retest of lower demand.

Technically, Bitcoin remains trapped between key moving averages. Price is still below the blue long-term trend line, which has acted as dynamic resistance since the breakdown from the $100,000+ region. At the same time, BTC is holding above the green moving average, suggesting that while the market is weak, longer-term buyers are still defending the broader uptrend structure.

This creates a fragile equilibrium: as long as Bitcoin holds above the current support zone, bulls can attempt to rebuild a base and reclaim $90,000-$92,000. However, if volatility expands and the market loses the green trend line, it would expose BTC to a deeper correction toward the mid-$80,000s, where previous demand briefly stepped in during the prior drawdown.

Featured image from ChatGPT, chart from TradingView.com

The Bitcoin price showed a sharp pullback this week caught many traders off guard. After hovering near record highs, the world’s largest crypto slid below the $90,000 mark as a wave of leveraged positions was forced out of the market.

Related Reading: Ripple President Long Unveils Her 2026 Crypto Predictions

The drop came amid rising global uncertainty, with investors reacting to geopolitical tensions, bond market stress, and renewed risk aversion across traditional assets.

By Tuesday, the Bitcoin price had fallen to around $87,800 before staging a modest rebound to around $89,000. While the move erased recent gains, market participants say the decline reflects more than just short-term volatility. It highlights how fragile sentiment can become when macro pressures and heavy leverage collide.

Leverage Unwinds Trigger Sharp Sell-Off

Data from CoinGlass showed that roughly $1.08 billion in crypto positions were liquidated over 24 hours, affecting more than 183,000 traders. Long positions made up about 92% of those liquidations, indicating that many traders had been positioned for further upside.

The largest single forced closure was a $13.52 million BTCUSDT position on Bitget, underscoring how crowded bullish bets had become. As prices slipped, automated liquidations accelerated the decline, pushing Bitcoin through key psychological levels.

This unwinding followed weeks of relative calm in crypto markets, during which the Bitcoin price had consolidated near its highs. Once selling pressure began, it quickly exposed how dependent recent price stability had been on leveraged positioning rather than fresh spot demand.

Macro Risks Weigh on Risk Assets

The crypto sell-off unfolded alongside broader market stress. U.S. President Donald Trump’s renewed tariff threats against European nations, tied to disputes over Greenland, revived fears of a trade war. Similarly, a sell-off in Japanese government bonds pushed global yields higher, tightening financial conditions.

U.S. equities also suffered their worst session since October, with major indices dropping more than 2%. Crypto-related stocks such as Coinbase, Strategy, and Circle posted steep losses, reflecting a wider shift away from risk-sensitive assets.

While the Bitcoin price and altcoins fell, gold and silver moved in the opposite direction. Gold traded near record highs above $4,800 per ounce, and silver also reached new peaks. The contrast suggested that investors were rotating into traditional safe havens as uncertainty grew.

Key Bitcoin Price Support Levels in FocusDespite the volatility, Bitcoin has shown early signs of stabilization. Prices rebounded toward the $89,000–$90,000 area as pressure in bond markets eased and U.S. equity futures ticked higher. Still, analysts caution that the move looks more like a pause after forced selling than a clear return of risk appetite.

Technical indicators highlight the $87,000–$88,000 range as a critical support zone. A break below this level could open the door to further declines toward $85,000 or lower. On the upside, Bitcoin price faces resistance near $92,000 and $95,000.

Related Reading: XRP Holders Quietly Build Positions In A Pattern That Echoes Earlier Cycles

For now, traders are closely watching macro developments, including Trump’s speech at the World Economic Forum in Davos and ongoing signals from global bond markets. Whether dip buyers step in with conviction may determine if Bitcoin can reclaim lost ground, or if the recent slide has further to run.

Cover image from ChatGPT, BTCUSD chart on Tradingview

https://cryptoslate.com/feed/

European leaders facing a Greenland-linked dispute with Washington could treat U.S. Treasurys as a leverage point.

That would test not just the headline size of foreign holdings, but the market’s capacity to absorb speed, and how quickly higher yields would filter into the dollar, U.S. credit conditions, and crypto liquidity.

The Financial Times has framed Greenland as a plausible flashpoint for U.S.-Europe tensions and argued that Treasurys could sit on the menu of countermeasures.

That framing places the focus on execution mechanics and timing rather than a single “EU sells X” headline.

According to the U.S. Treasury’s Treasury International Capital (TIC) Table 5, foreign investors held $9.355 trillion in U.S. Treasurys at end-November 2025.

Of that total, $3.922 trillion was attributed to foreign official holders, a pool large enough that even partial portfolio shifts, especially if coordinated or fast, can register in rates.

The first constraint is measurement.

TIC country lines track securities reported by U.S.-based custodians and broker-dealers, and Treasury notes that holdings in overseas custody accounts “may not be attributed to the actual owners.”

That means the table “may not provide a precise accounting of individual country ownership,” a caveat that complicates any claim that “the EU” could dump a defined amount on command.

A portion of European beneficial ownership can appear in non-EU country lines, and European custody hubs can hold Treasurys for non-European owners. The practical implication is that “sell capacity” is not identical to “European-attributed holdings,” and policymakers have clearer influence over official portfolios than over private custody flows.

A defensible reference set exists inside the TIC data if it is described as custody attribution rather than EU ownership.

At end-November 2025, Treasurys attributed to Belgium ($481.0 billion), Luxembourg ($425.6 billion), France ($376.1 billion), Ireland ($340.3 billion), and Germany ($109.8 billion) totaled about $1.733 trillion.

Presented properly, that $1.73 trillion number is an upper-bound reference for identified major EU reporting and custody jurisdictions, not a verified EU-27 beneficial-owner total.

Custody data vs. “EU ownership” and why it matters

Official-sector positioning adds another layer because “official” can mean a classification in TIC reporting, while Fed custody data describes a location-based subset held in custody at Federal Reserve Banks.

The Federal Reserve’s international summary data show foreign official U.S. Treasury securities held in custody at Federal Reserve Banks at $2.74589 trillion in November 2025 (preliminary).

That location-based subset sits below the TIC “foreign official” total of $3.922 trillion at end-November.

How the Greenland dispute translates into selling would probably run through a sequence of policy signaling and portfolio mechanics rather than a single announcement of forced liquidation.

A preconditioning phase could unfold over weeks or months in which rhetoric hardens, and European policymakers discuss financial countermeasures in risk-management terms, consistent with the Financial Times framing that Treasurys could serve as leverage.

A second phase, spanning days to weeks, would center on a policy signal such as a coordinated call to shorten duration, reduce exposure, or adjust reserve-management guidelines.

Those steps can be executed without formally labeling the move as weaponization, and without requiring a centralized “EU” sale order.

The execution phase would then determine market impact, with two channels that can overlap.

One is official runoff through non-reinvestment at maturity, which can play out over quarters or years.

The other is active secondary-market sales by public and private holders, which can compress into weeks if hedging constraints, risk limits, or volatility targeting bind.

Even if the political intent is gradual diversification, volatility can turn it into a de facto flow shock if private hedgers and leveraged Treasury holders de-risk at the same time.

The liquidation timeline matters because research has linked month-scale changes in foreign official flows to rate moves.

A 2012 Federal Reserve International Finance Discussion Papers study estimated that if foreign official inflows into Treasurys drop by $100 billion in a month, 5-year Treasury rates rise about 40–60 basis points in the short run.

It also estimated long-run effects near 20 basis points after private investors respond.

The paper is dated, so the figures function as order-of-magnitude bounds for speed risk rather than a point estimate for today’s market structure.

Even so, the core implication remains: a faster “dump” (or a faster stop in marginal buying) has a different rate profile than a maturity runoff.

Important: The table below lays out editorial scenario constructs using an execution-speed lens. Sale sizes are illustrative except the $1.73 trillion line, which is a TIC custody-attribution reference for major EU reporting and custody jurisdictions and explicitly not a verified EU beneficial-owner amount. The rate language is framed as regime risk (orderly vs disorderly) rather than a linear “bps per $X” extrapolation.

| Scenario (sale amount) | One-month execution (flow shock framing) | One-quarter execution (absorption window) | 1–3 years (runoff framing) |

|---|---|---|---|

| $250B | Heuristic short-run +100–150 bps on 5-year rates if concentrated in a month; long-run effects nearer +50 bps after private response (2012 elasticity) | Lower peak move if distributed, with repricing tied to hedging and risk appetite | Often resembles reduced reinvestment, with term-premium drift more than a single shock |

| $500B | Heuristic short-run +200–300 bps; long-run effects nearer +100 bps (2012 elasticity) | Greater chance of persistent term-premium repricing if sustained alongside wider “sell America” flows | Functions as diversification, with market impact spread across cycles |

| $1.0T | Tail-risk short-run +400–600 bps; long-run effects nearer +200 bps (2012 elasticity) | Would test dealer balance sheets and risk-bearing capacity even with time to adjust | Hard to distinguish from structural reallocation without clearer attribution data |

| $1.73T (TIC custody-attribution reference) | Tail-risk framing if treated as a one-shot sale, while noting the $1.73T is not EU beneficial ownership | Could transmit as a multi-quarter tightening impulse if sales coincide with heavier hedging demand | Resembles a multi-year reserve and portfolio shift if done mainly through runoff |

Execution speed, yield shock risk, and broader market spillovers

Any sustained yield backup would land on a U.S. economy carrying a large debt stock.

U.S. gross national debt stands at $38.6 trillion as of press time.

That scale increases sensitivity to marginal funding-cost shifts even when refinancing occurs over time.

Higher Treasury yields typically tighten financial conditions through benchmark effects on mortgages, investment-grade issuance, and leveraged credit.

Equity valuations can also re-rate as the risk-free discount rate changes, channels that become more acute if the term premium reprices rather than only the policy path.

The spillover is broader than Treasurys because foreign investors hold a large footprint across U.S. markets.

The Treasury’s annual survey reported $31.288 trillion in foreign holdings of U.S. securities, including $12.982 trillion in long-term debt and $16.988 trillion in equities.

In crypto-adjacent markets, stablecoin issuers are also material Treasury buyers; see CryptoSlate’s breakdown of stablecoin issuers’ Treasury demand.

Dollar outcomes split into two regimes that can coexist across horizons.

In acute stress, a geopolitical shock can push investors toward dollar liquidity and U.S. collateral even as one bloc sells, a setup where yields move higher while the dollar holds up, or even strengthens.

Over longer horizons, sustained politicization can pull the other direction if allies treat U.S. government paper as a policy variable, nudging incremental diversification in official portfolios and gradually weakening structural dollar demand.

The International Monetary Fund’s COFER data show the dollar at 56.92% of disclosed global reserves in Q3 2025, with the euro at 20.33%.

That structure tends to change in steps rather than a single break.

The IMF has also described prior quarterly moves as sometimes valuation-driven, noting that the Q2 2025 decline in the dollar share was “largely valuation-driven” through exchange-rate effects.

That dynamic can blur interpretation of quarter-to-quarter shifts during volatility.

Crypto transmission: liquidity, discount rates, and narrative reflexivity

For crypto markets, the near-term linkage would run through rates and dollar liquidity rather than reserve shares alone.

A fast Treasury liquidation that lifts intermediate yields would raise the global discount rate and can tighten leverage conditions that feed into BTC and ETH positioning.

A slower runoff would transmit more through term-premium drift and portfolio rebalancing across equities and credit.

The narrative channel can cut the other way.

A high-profile episode where allied blocs discuss Treasurys as a policy tool can reinforce the “neutral settlement” framing that parts of the market apply to crypto, even if the first-order move is risk reduction under higher yields.

Tokenized Treasury products sit at the intersection of TradFi collateral and crypto rails; see CryptoSlate’s coverage as tokenized U.S. Treasurys reached a $7.45 billion all-time high.

What traders and policymakers would watch for is not a single “EU sells X” headline, because custody-based data can misstate beneficial ownership.

Instead, they would likely track a sequence of observable proxies, including shifts in foreign official custody holdings at the Fed and changes in TIC-reported totals over subsequent months.

If Greenland becomes the trigger for sustained U.S.-EU financial brinkmanship, the market variable that matters first is whether any Treasury reduction is executed as a one-month flow shock or a multi-year runoff.

The post US Treasurys face a $1.7 trillion EU “dump” over Greenland, forcing shift to Bitcoin if dollar safety vanishes appeared first on CryptoSlate.

Binance, the largest crypto exchange by trading volume, has listed Ripple's RLUSD stablecoin on its platform.

On Jan. 21, the exchange announced that it would open spot trading pairs, including RLUSD/USDT, RLUSD/U, and XRP/RLUSD, on Jan. 22 by 8 AM UTC.

Critically, Binance will initiate trading on the RLUSD/USDT and RLUSD/U pairs with zero fees until further notice.

To a casual trader, this reads like a straightforward listing announcement. However, industry experts noted that the move could fundamentally alter the market hierarchy and cement RLUSD's rapid growth over the past year.

The logic here is not that Binance magically creates value, but that the exchange can change how the market routes value. If that routing translates into sustained net issuance, RLUSD could plausibly jump into the top three stablecoins in a rapidly expanding market.

Engineering a liquidity event

The specific mechanics of the Binance listing suggest a push for dominance rather than mere participation.

By waiving fees, Binance is not merely adding trading pairs; it is subsidizing adoption. Zero-fee stablecoin pairs have a history of changing market share on centralized exchanges by redirecting where trades clear.

Kaiko’s analysis of stablecoin dynamics on Binance offers a precedent for disrupting these numbers. After the exchange re-listed USDC in March 2023, the token’s market share on centralized exchanges reportedly surged from roughly 60% to above 90%.

This shift did not necessarily mean USDC instantly became the superior asset. It meant Binance made it the cheapest and most convenient rail, and the market followed the incentives.

Kaiko has also documented how zero-fee regimes can dominate exchange volume and reshape market structure.

This presents both a promise and a warning for Ripple’s stablecoin. Incentives can create deep liquidity quickly, but they can also inflate activity that evaporates when the subsidy ends.

For RLUSD to move toward the top three, two distinct “flywheels” must spin in sequence.

The first is routing adoption. Zero fees encourage market makers and high-frequency desks to quote tighter spreads and push more flows through RLUSD pairs.

This improves the experience for all participants by deepening the order book, reducing slippage, and ensuring more reliable execution. In stablecoin markets, where product differentiation is often thin, the preferred asset is frequently the one that trades most efficiently.

The second flywheel is balance-sheet adoption. Market cap grows only when RLUSD is actually held, whether as exchange collateral, in DeFi lending markets, or in treasury allocations.

Binance creates the environment for this by expanding RLUSD utility. The listing announcement confirmed that portfolio margin eligibility will be added, increasing the token’s utility in leveraged trading strategies.

Furthermore, inclusion in Binance Earn is planned. This would give users yield-bearing incentives to hold the asset rather than simply trade it.

The math behind the climb

Despite this strategic setup, the numerical gap RLUSD must close to reach the top three is substantial.

Data from CryptoSlate shows that RLUSD has a circulating supply of around $1.4 billion. This places it among the top 10-largest stablecoins by market cap but significantly behind market leaders Tether's USDT and Circle's USDC.

To breach the “top 3 stablecoin,” RLUSD would need roughly $5.1 billion in new circulation to displace Ethena’s USDe, whose supply sits around $6.47 billion.

Over a 12-month period, reaching that benchmark would require approximately $424 million in net new RLUSD issuance per month

These are large numbers that would require RLUSD to grow four to seven times from its current base within a relatively tight window.

However, macro tailwinds may assist this ascent.

The US Treasury has publicly argued that the stablecoin market, currently valued at around $300 billion, could grow tenfold by the end of the decade. That would imply that the market could reach $3 trillion by 2030.

Meanwhile, US banking giant JPMorgan is more optimistic, projecting that stablecoins could reach $2 trillion within two years under a bullish adoption scenario.

If those trajectories materialize, RLUSD reaching the top three will not only be about stealing market share from incumbents but also about riding a rising tide.

Institutional plumbing over retail hype

While the Binance listing provides the liquidity spark, Ripple’s best case for the top three relies on institutional plumbing.

Over the past two years, Ripple has assembled a stack that resembles that of a payments and capital markets infrastructure provider more than that of a typical crypto issuer.

The foundation of any potential growth is a regulatory posture that has resulted in RLUSD being issued under a New York DFS Limited Purpose Trust Company Charter. At the same time, Ripple has received conditional approval for an OCC charter.

This dual layer of state and federal oversight sets a bar for transparency and compliance that few other issuers can claim.

For corporate treasurers and bank compliance officers, this regulatory perimeter often matters more than brand recognition.

Perhaps the most direct catalyst for sticky institutional adoption is that Ripple has quietly positioned itself at the center of the global payment network as a platform that settles, secures, and moves digital money.

Last year, Ripple had a $4 billion acquisition spree that included the purchase of prime broker Hidden Road, custody firm Palisade, treasury-management platform GTreasury, and stablecoin payments provider Rail.

These firms form the foundation of a vertically integrated enterprise spanning trading, custody, payments, and liquidity management.

This move essentially expands RLUSD’s growth runway beyond crypto exchange wallets. It moves the asset into multi-asset margin and financing workflows where stablecoin balances can scale rapidly.

A stress test

The risk remains that while trading volume can be manufactured, adoption cannot.

Binance’s own spot market has cooled recently, with CoinDesk Data reporting spot volume fell to $367 billion in December 2025, the lowest since September 2024.

Yet even at these reduced levels, Binance remains large enough that a fee subsidy can reshape liquidity routing.

So, the ultimate danger in this move is that RLUSD could become a “cheap rail” but not a “held asset.”

If trading volume explodes but circulating supply barely grows, the market will have its answer: Binance can create liquidity, but not necessarily durable adoption.

For RLUSD to credibly challenge for the top three, the story must evolve from “listed and traded” to “used and held.”

The post Ripple’s RLUSD just got Binance’s strongest growth lever, can that catapult it into a top 3 asset? appeared first on CryptoSlate.

https://ambcrypto.com/feed/

Funding is negative, and long-term holders are moving their supply.

Funding is negative, and long-term holders are moving their supply. Behind Ethereum’s red candles lies a tug-of-war few charts can fully explain.

Behind Ethereum’s red candles lies a tug-of-war few charts can fully explain.https://beincrypto.com/feed/

Markets rallied after US President Donald Trump called off tariffs on European allies on Wednesday following his speech at the World Economic Forum in Davos.

However, the relief proved short-lived, suggesting that while levies and military action were ruled out, lingering concerns over a potential Greenland takeover and Fed intervention at home continued to weigh on investor sentiment.

Global Markets Experience Short-Lived Relief

Shortly after Trump walked back earlier promises to impose tariffs on eight European countries, Bitcoin reclaimed the $90,000 level. The move reflected investor relief amid signs of de-escalation following a volatile week.

US equities also stabilized. The S&P 500 rose 1%, recovering part of the 2.1% decline recorded a day earlier after Trump’s original tariff announcement. The Nasdaq posted similar gains. Meanwhile, the Dow Jones Industrial Average jumped 550 points.

The relief, however, appeared short-lived. The dollar remained under pressure, edging lower against both the euro and the yen.

Demand for gold also remained firm, with prices hovering near $4,839, up around 1% from the previous day.

Despite Trump’s tariff reversal and his assurance that the United States would not use force to acquire Greenland, investor confidence remains fragile. The remarks did little to ease broader concerns about geopolitical risks and policy uncertainty, which continue to shape market sentiment.

Greenland Push Meets Fed Independence Fears

Trump’s firm push for the United States to acquire Greenland did little to fully eliminate uncertainty. Though the president disclosed on social media that the United States and Europe had “formed the framework of a future deal,” the deal has not yet been closed, and its details remain unknown.

If it falls through, Trump already anticipated that consequences would follow if the European Union failed to meet US demands.

“We want a piece of ice for world protection. You can say yes, we will be very appreciative. You can say no, and we will remember,” the US President said.

At the same time, Trump renewed calls for looser monetary policy, sharply criticizing the Federal Reserve. He targeted Chair Jerome Powell, calling him “stupid” and accusing him of maintaining overly restrictive interest rates that he said were weighing on economic growth.

Concerns about potential political interference in the US central bank have rippled through financial markets in recent weeks amid heightened investor unease.

Several prominent business leaders have publicly defended the principle of central bank independence. Last week, JPMorgan Chase CEO Jamie Dimon criticized the Department of Justice’s decision to pursue a criminal investigation into Powell.

“This is probably not a great idea and in my view, it will have the reverse consequences of raising inflation expectations and probably increase rates over time,” he told reporters during a conference call.

Despite the criticism, Trump did not soften his stance. He concluded his remarks by expressing confidence that the next individual selected to replace Powell as chair would “do the right job.”

Overall, investors remain cautious about what may come next.

The post Markets Rally After Trump Scraps Tariffs, but Greenland and Fed Risks Linger appeared first on BeInCrypto.

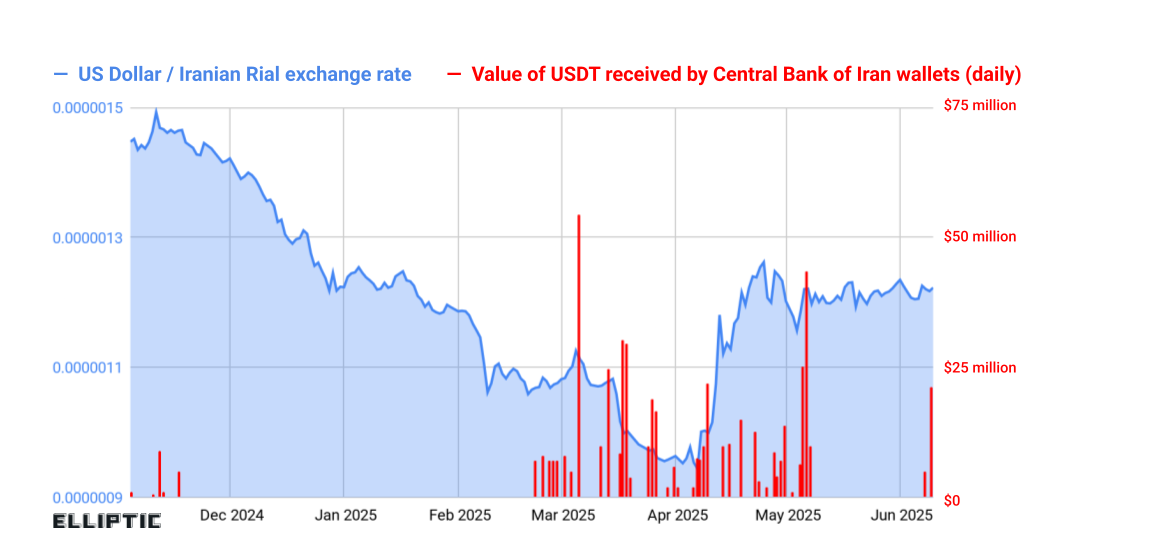

Iran’s Central Bank secretly purchased more than $500 million worth of Tether’s USDT stablecoin as the country’s currency crisis deepened, according to new findings from crypto security firm Elliptic.

The transactions point to a state-level effort to stabilize the collapsing rial and maintain trade flows while bypassing the global banking system.

Iran’s Rial Crisis Explained

Elliptic said it identified a network of crypto wallets controlled by the Central Bank of Iran (CBI) that accumulated at least $507 million in USDT during 2025.

The figure represents a lower bound, as the analysis only includes wallets attributed with high confidence.

Iran’s currency crisis has intensified over the past year, with the rial plunging to historic lows on the open market.

By early 2026, the exchange rate had deteriorated to levels where the rial’s purchasing power was effectively wiped out, fueling public anger and market panic.

Although the rial did not technically fall to “zero,” its rapid depreciation rendered it nearly unusable for international trade and savings.

Multiple exchange rates, high inflation, and a loss of confidence pushed businesses and households toward dollars, gold, and crypto-linked alternatives.

Sanctions pressure compounded the crisis. Restricted access to dollar clearing and correspondent banking sharply limited Iran’s ability to deploy foreign currency reserves, even when oil revenues were available.

Elliptic Traces USDT Purchases to 2025

Against this backdrop, Elliptic uncovered leaked documents showing two USDT purchases by the Central Bank in April and May 2025, paid for in UAE dirhams (AED). The timing coincided with rising pressure on the rial and renewed volatility in currency markets.

Using these documents as a starting point, Elliptic mapped the Central Bank’s broader wallet infrastructure. Its analysis revealed a systematic accumulation of stablecoins, rather than ad hoc crypto use.

Initial Reliance on Domestic Exchanges

Until mid-2025, most of the Central Bank’s USDT flowed into Nobitex, Iran’s largest cryptocurrency exchange. Nobitex allows users to hold USDT, exchange it for other cryptoassets, or sell it for rials.

This pattern suggests the Central Bank initially used the exchange as a domestic liquidity channel. USDT functioned as a parallel dollar reserve that could be converted into local currency when needed.

However, that approach carried significant exposure.

Strategy Shifts After Major Hack

In June 2025, the flow of funds changed abruptly. Elliptic found that USDT was no longer routed primarily through Nobitex but instead sent through cross-chain bridges, moving assets from TRON to Ethereum.

From there, the funds were swapped on decentralized exchanges, moved across blockchains, and routed through some centralized platforms. This process continued through the end of 2025.

The shift followed a $90 million hack of Nobitex on June 18, 2025, carried out by the pro-Israel group Gonjeshke Darande.

The group accused Nobitex of facilitating sanctions evasion and claimed to have destroyed the stolen assets.

Local Claims Raise Data Security Concerns

Iranian media reporting has since amplified scrutiny of the Central Bank’s crypto operations.

Businessman Babak Zanjani recently claimed the Central Bank purchased USDT to manage the foreign exchange market and transferred the funds to wallets linked to a national banking technology subsidiary.

“The concerning point is that for every wallet to which we transferred Tether, our wallet address was, within a short period, either disclosed to hostile networks or placed on Israel’s sanctions and seizure lists. This raises a serious and fundamental question: Is there an information breach within the Central Bank, or does Israel secretly monitor the Central Bank’s structure and processes?” wrote Babak Zanjani.

Zanjani alleged that wallet addresses were quickly exposed and later flagged by hostile actors, raising concerns about information leakage inside sensitive financial institutions.

While unproven, the claims intensified calls for transparency from the Central Bank and its technology partners.

The post Iran’s Central Bank Bought $500 Million in USDT Stablecoin to Prop Up Rial appeared first on BeInCrypto.

https://cryptonewsz.com/feed/

https://www.newsbtc.com/feed/

Solana Mobile has rolled out its long-awaited SKR token airdrop for Seeker smartphone users and select developers, adding a fresh ecosystem catalyst as SOL trades near a critical technical support zone.

Related Reading: What the Triple-Tap At $1.80 Means For The XRP Price

The launch comes at a time when Solana’s price is hovering around $120–$130, an area analysts see as decisive for the token’s medium-term direction. SKR debuted at around $0.006 and climbed above $0.01 within hours of launch, pushing its market capitalization past $70 million.

More than 100,000 users are eligible to claim the airdrop through the Seeker phone’s built-in wallet over a 90-day window. Any unclaimed tokens will be returned to the general distribution pool.

Solana SKR Airdrop Targets Users and Developers

Solana Mobile allocated 30% of SKR’s fixed 10 billion token supply to airdrops and early unlocks. Nearly 2 billion SKR are being distributed to Seeker phone owners and developers who deployed “quality apps” in the Solana dApp Store during Season 1.

The company said the token underpins governance, incentives, and economic activity within the Solana Mobile ecosystem. SKR can be staked directly from the Seed Vault wallet, with inflation events occurring every 48 hours. The annual inflation rate starts at 10% and declines by 25% each year until it stabilizes at 2%.

The airdrop coincides with the start of Seeker’s Season 2 campaign, which introduces a refreshed app catalog, rewards programs, and a focus on sectors such as DeFi, gaming, payments, trading, and decentralized physical infrastructure (DePIN).

Community reaction has been mixed. Some users reported receiving several thousand dollars’ worth of SKR, while others reported allocations closer to $50–$100. Some users expressed disappointment, citing delays in phone delivery and additional shipping costs.

SOL Price Near Key SupportWhile SKR draws attention to Solana’s mobile strategy, the SOL token itself is facing a technical test. After breaking below $136, SOL has slipped into the $120–$127 zone, where an ascending trendline from the 2023 lows meets historical horizontal support.

This area has previously acted as both resistance and support, making it a closely watched “flip zone” for traders. A sustained hold above $120 could open the door to a recovery toward the $135–$150 range. A breakdown, however, may expose downside targets near $110 or even $100.

Related Reading: Trove’s New Token Craters 95%, Sparking Investor Revolt

Short-term indicators show some stabilization. SOL recently bounced from around $124 to near $128, supported by renewed ETF inflows of roughly $3.08 million and spot market accumulation of about $9.31 million. These flows suggest buyers are stepping in at current levels.

Cover image from ChatGPT, SOLUSD chart on Tradingview

Ethereum has taken a sharp turn after facing a firm rejection at the $3,220 level, with price breaking structure and slipping into a weaker posture. The speed of the drop and lack of strong buying interest raise an important question for traders: Is this merely an early warning sign within a broader uptrend, or the start of a deeper distribution phase that could pressure ETH further in the near term?

Rejection At $3,220 Signals Distribution, Not A Shakeout

Crypto analyst PEPE is Friend highlighted that Ethereum’s sharp rejection at the $3,220 level was deliberate rather than random. The drop was clean, with key structure breaking down, selling pressure accelerating, and price quickly flushing toward the $3,106 area, aligning with a classic distribution behavior rather than a simple shakeout.

Assessing the current price reaction, there are still no signs of a true reversal. The bounce has been notably weak, trading volume remains thin, and buyers have yet to show a strong commitment. Instead of signaling renewed bullish momentum, the move higher appears to be a technical pullback within a broader weakening structure.

The key technical zone remains well-defined. ETH is trading below the former support band between $3,170 and $3,200. As long as the price stays below this range, any upside move is likely to be viewed as a selling opportunity rather than the start of a sustained recovery.

When this price action is viewed alongside Ethereum spot ETF data, the picture becomes clearer. While ETF flows remain positive daily, they lack strong momentum or a standout confirmation day. Capital appears to be absorbed rather than aggressively deployed, suggesting institutional demand is not yet strong enough to drive a decisive breakout. Until that changes, sellers are expected to remain in control below the $3,170–$3,200 resistance zone.

Ethereum Slips Below $3,062 As Bears Regain Short-Term Control

In an X post, Kamile Uray noted that Ethereum has closed below the $3,062 level, shifting attention toward the next major downside zone at $2,623. This level is now critical, as holding above it could allow ETH to stabilize and attempt another recovery move.

On the upside, a clean break above the pink-box resistance near $3,445 would activate bullish formations such as a cup-and-handle or an ascending triangle, opening the door for a move toward the $3,894 area.

Further strength would be confirmed if ETH manages to close above the $3,661 high, which would mark the first higher high on the daily chart relative to the previous downtrend, improving the bullish outlook. Still, $3,894 remains a key level, as it aligns with the 0.618 Fibonacci retracement of the last decline.

On the downside, a clear break below the $2,623 low would expose ETH to deeper losses, with the $2,274–$2,104 zone emerging as the next major support area. This region hosts a potential bullish “Libra” reversal setup, and Ethereum could once again attempt a bounce toward its previous all-time high if reversal confirmation appears there.