Financial RSS Feeds

https://www.investing.com/rss/news.rss

https://cointelegraph.com/rss

In an interview from the WEF in Davos, David Sacks addressed disputes over stablecoin yield and the crypto market structure legislation that's stalled in the US Senate.

The Central Bank of Iran reportedly stockpiled more than half a billion dollars worth of USDt amid escalating protests and crypto usage in the country.

https://www.coindesk.com/arc/outboundfeeds/rss/

https://cryptobriefing.com/feed/

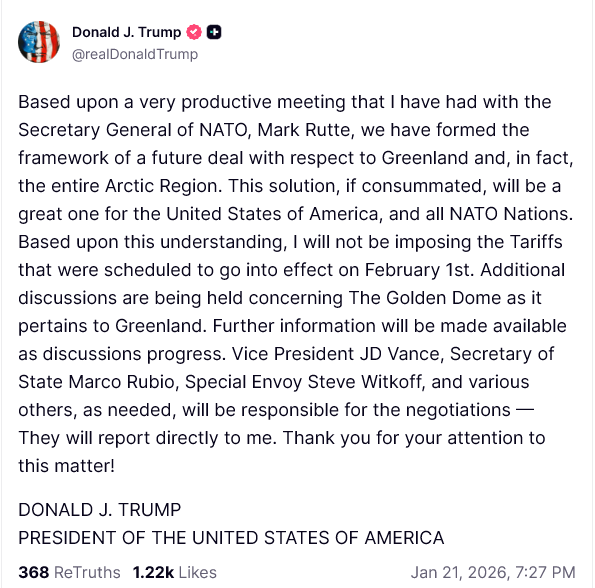

Donald Trump says he will not impose 10% tariffs on NATO nations on Feb 1 after reaching a framework deal over Greenland and Arctic talks.

The post Trump reverses planned Feb 1 tariffs on NATO nations after Greenland talks appeared first on Crypto Briefing.

Intel stock hits four-year high with 35% YTD gain on $8.9B government investment and 18A chip launch ahead of Q4 earnings.

The post Intel shares surge 11% to four-year high ahead of Q4 earnings call appeared first on Crypto Briefing.

https://bitcoinist.com/feed/

A disagreement over US crypto regulation has spilled into public view, drawing the Cardano and XRP communities into an unexpected clash. The reason is the Digital Asset Market Clarity Act, a proposed bill intended to define how digital assets are regulated in the United States.

The disagreement started after Charles Hoskinson openly criticized Brad Garlinghouse over his stance on the legislation, which led to pushback from prominent XRP community members. This comes just after reports have suggested growing frustration among lawmakers toward Coinbase over disagreements tied to the Clarity Act.

Hoskinson’s Criticism And Garlinghouse’s Position In Full Context

The tension came to the surface during a livestream in January 2026, where Hoskinson criticized Garlinghouse’s apparent support for advancing the Clarity Act despite its shortcomings. In the video, Hoskinson expressed skepticism about the bill’s direction and origins, remarking sarcastically, “And what we got is Elizabeth Warren wrote the bill, that’s leadership we can believe in.”

He went on to challenge the idea that passing an imperfect bill is preferable to continued uncertainty, pointing directly to the position of Ripple CEO Brad Garlinghouse. Hoskinson questioned whether handing regulatory power to the same institutions that previously sued, subpoenaed, or shut down crypto businesses could truly be considered progress.

Hoskinson’s remarks did not go unanswered. Vet, a notable XRP community member and XRP Ledger dUNL validator, reposted the video on X and criticized Hoskinson’s approach. Vet questioned why Hoskinson chose to publicly attack Garlinghouse instead of contributing constructively to the legislative process, writing, “How about focusing on helping shape the Clarity Bill instead of crashing out on Brad for no reason, Charles?”

Why The Clarity Act Matters To Both Communities

The Clarity Act is one of a few bills introduced during the current crypto-positive Trump administration that aims to bring structure to a regulatory environment that has been uncertain for years. The Clarity Act, in particular, was introduced to bring clarity around whether digital assets should be treated as securities or commodities and which agencies should oversee them.

The bill represents a necessary step toward legal certainty and institutional participation. Supporters of XRP tend to see engagement with lawmakers as a practical route forward after years of legal battles. However, others like Charles Hoskinson are of a different notion.

The Clarity Act is not without its issues. Sources close to the White House say the administration is considering pulling its support for the Clarity Act if Coinbase does not return to negotiations over stablecoin yield provisions. However, Coinbase CEO Brian Armstrong noted that Coinbase is actively working to find common ground with banks on yield-related issues.

A similar Act, called the Guiding and Establishing National Innovation for US Stablecoins Act, or the “GENIUS Act,” was signed into law in 2025 by President Donald Trump as part of efforts to create better regulatory clarity towards stablecoins in the United States.

Interestingly, Ripple CEO Brad Garlinghouse was part of the crypto industry leaders that expressed support for the Genius Act after it was signed into law.

In a sudden move, the cryptocurrency market flipped extremely bearish, causing major digital assets such as XRP to drop sharply. After days of trading above the $2 price mark, the altcoin has fallen below this level, bringing it to the key $1.80 support. While the leading altcoin continues to face heightened volatility, its derivatives market is telling a different story.

Traders Crowd Back Into The XRP Market

XRP’s price action and its derivatives market are moving in different directions as traders continue move back into the altcoin. On-chain data shows that derivatives activity is heating up, with Open Interest (OI) undergoing a sharp rise after weeks of downward performance or sluggish growth.

A crypto pundit and investor, Xaif Crypto, reported that XRP open interest has moved above its 30-day average as volatility reaches its highest level since November 2025. This rise in open interest is centered on Binance, the largest cryptocurrency exchange in the world.

As both speculative positioning and hedging activity pick up pace in reaction to broader price swings, the rise suggests a resurgence of trader activity. Furthermore, heightened volatility and rising open interest frequently indicate a turning point, when leverage is increasing, and the market is preparing for a big move.

The chart indicates that the total open interest is around $566 million against a 30-day average near $529 million. These figures suggest that new positions are steadily entering the market, not aggressively. However, this is not the major signal of the trend.

Currently, rising open interest volatility, with the standard deviation at its highest level in months, is the primary indicator. Meanwhile, the Z score is still moderate, sitting around the 0.57 level. Xaif Crypto stated that this development suggests cautious accumulation and growing risk without extreme leverage in the market.

It is worth noting that these conditions typically unfold prior to a strong directional move. With the current setup, XRP has entered a more dynamic and reactive trading environment than it has seen in months, regardless of whether this surge of activity resolves into continuation or reversal.

A Steady Wave Of Capital Inflows

A recent CoinShares report from Xaif Crypto shows that XRP is still attracting fresh capital at a significant rate. Despite a volatile market condition, weekly inflows have extended, pointing to a growing confidence among investors in the leading altcoin.

In the past week, the token pulled in over $69.5 million in inflows. This figure shows that demand is persistently building beneath the surface, indicating rising accumulation rather than speculative interest. While markets have shifted toward a volatile state, fresh capital is still being rotated into XRP.

The capacity of XRP to attract investment even in slower times is becoming a more significant indicator for its medium-term prospects. As both institutional and large-scale participants flock in, this raises the discussion that a bigger move might be imminent, and these investors are positioning themselves ahead of it.

https://cryptoslate.com/feed/

At first glance, this looks like a story that lives on the back pages of a newspaper, Japanese government bonds with maturities that run so long they sound like a joke, 20 years, 30 years, 40 years.

If you own Bitcoin, you still end up in the blast radius.

Because when Japan’s long-dated bonds start to wobble, it is rarely just about Japan. It is about the world’s last big source of cheap money slowly turning into something more expensive, and what happens to every trade that quietly depended on that cheap funding.

The moment the mood changed

Japan has spent most of the last few decades as the place where money was close to free. That shaped global markets in a thousand small ways, even if you never bought a Japanese bond in your life.

Now that era is fading.

In December, the Bank of Japan lifted its benchmark rate to 0.75%, the highest level in roughly 30 years, part of a broader shift away from ultra-low policy that defined the country’s post-1990s playbook.

That move matters because Japan is not a small player. It is a funding hub. It is a reference point. It is the place global investors could point to when they wanted to borrow cheaply, hedge later, and hunt for returns somewhere else.

When that cheap anchor starts lifting, markets adjust, sometimes gently, sometimes all at once.

The signal people can’t ignore, long bonds are screaming

The fresh red flag is coming from the far end of Japan’s yield curve, the super-long bonds.

Japan’s 40-year government bond yield pushed above 4% for the first time, hitting around 4.2% as selling pressure built, and a recent 20-year auction showed weaker demand with a bid-to-cover ratio of 3.19, below its 12-month average.

Even if you do not live in bond world, that is the kind of detail traders circle with a thick marker. Auctions are where the market reveals how much real appetite exists for the debt being issued. When demand starts slipping at the long end, investors start asking harder questions about who the marginal buyer is going forward, and how much yield Japan will have to offer to keep funding itself smoothly.

A second datapoint makes the shift feel less like a blip. Japan’s 30 year government bond yield has climbed to about 3.46%, up sharply from about 2.32% a year earlier.

This is what a regime change looks like in slow motion, one auction, one basis point, one nervous headline at a time.

Why crypto ends up involved

Crypto loves to tell stories about being outside the system. The price still lives inside the system.

When rates rise, especially long-term rates, the entire market has to rethink what tomorrow’s cash is worth today. Higher yields raise the bar for every risky bet, stocks, private credit, venture, and yes, Bitcoin.

BlackRock put it bluntly in a recent note on crypto volatility, Bitcoin has historically shown sensitivity to USD real rates, similar to gold and some emerging market currencies, even if its fundamentals do not depend on any single country’s economy.

So when Japan’s moves ripple into global yields, Bitcoin can react before anyone finishes explaining the bond math on TV.

We have already seen a version of that movie lately. Global bonds sold off after hawkish comments from BOJ Governor Kazuo Ueda, and Bitcoin fell 5.5% in the same session, extending its monthly drop to more than 20%.

That is the bridge between “Tokyo bond auction” and “why did my crypto portfolio just bleed.”

The quiet mechanism behind the drama, the yen carry trade

There is a plumbing story here, and it matters more than the headlines.

For years, one of the simplest trades in global finance was borrowing in yen at very low rates, then putting that money to work in higher-yielding assets elsewhere. It does not always show up as a single obvious position you can point at; it shows up as a backdrop, as a source of steady demand for risk and yield.

When Japan tightens, that backdrop changes.

If the yen strengthens or funding costs rise, that carry trade can unwind. Unwinds tend to be messy because they are driven by risk limits, margin calls, and crowded exits.

The Bank for International Settlements studied a volatility burst and carry trade unwind in August 2024 and described how large FX carry positions were especially sensitive to spikes in volatility and were forced to unwind quickly.

You do not need to believe crypto is “part of the carry trade” to see the connection. You just need to accept that when leverage gets pulled out of the system, the most liquid risk assets often get sold first, and Bitcoin is one of the most liquid risk assets on the planet.

Japan’s bond story is also a political story, and politics moves yields fast

The long end of Japan’s curve is reacting to policy uncertainty too. The 40-year yield jump is tied to investor anxiety over a snap election and fiscal plans, the kind of political catalyst that can turn a slow grind into a sudden lurch.

Markets can tolerate a lot, they hate guessing games about issuance, spending, and the future buyer base for government debt.

If investors begin to suspect Japan will be leaning more heavily on the bond market, and doing so while its central bank is less willing to suppress yields, they demand more compensation. That is what a rising long bond yield often represents, the market asking to be paid more for time and uncertainty.

The crypto angle that lasts longer than today’s price action

The durable question is simple, does Japan’s shift keep global financial conditions tighter than markets are expecting.

If the answer is yes, crypto’s upside gets capped, rallies become choppier, leverage becomes more fragile, and every risk flare-up feels sharper.

If the answer is no, and Japan’s transition stays orderly, then the bond market stops being the main character, and Bitcoin goes back to trading its usual mix of liquidity, positioning, and narrative.

There are a few forward paths worth mapping, and none of them require pretending anyone can predict a Bitcoin candle.

Three scenarios worth watching next

1) Orderly normalization

Japan continues raising rates gradually, the bond market absorbs it, auctions stay decent, yields stay high but stop behaving like a panic meter.

In this world, the pressure on crypto shows up as a steady headwind. Higher risk-free returns compete with speculative appetite. Bitcoin can still run, especially if other forces turn supportive, but the market keeps looking over its shoulder at real yields.

2) Auction stress turns into a global duration tantrum

More weak auctions, more headlines about demand, more volatility at the long end.

Global yields jump as relative value traders adjust and as investors worry about repatriation flows, then equities and crypto take the hit.

The recent example is already on the tape, global bonds slid on hawkish BOJ signals, and Bitcoin dropped 5.5% on the day.

This scenario tends to look like forced selling. Fundamentals become background noise.

3) Policy response calms the market

Japan’s officials push back hard against disorderly moves, issuance choices shift, bond buying operations, and guidance are used to cool volatility, and yields stop surging.

That can loosen global conditions at the margin, simply by removing a source of stress. Bitcoin responds the same way it often does when the market senses less pressure from rates and funding.

The point is not that Japan “helps crypto,” the point is that global liquidity expectations shift.

The simple dashboard, what to watch if you want the earliest tells

If you want to stay ahead of the story, you do not need twenty indicators. You need a handful.

- Japan’s long bond yields, especially the 30-year and 40-year.

- 20-year and 30-year auction strength, including bid-to-cover ratios.

- USDJPY, because carry dynamics often surface there first.

- US real yields, because Bitcoin has a history of reacting to them.

- Volatility spikes, because carry positions can unwind fast when vol rises.

Where stablecoins fit, the overlooked side channel

This part gets missed in a lot of crypto coverage.

Crypto has its own internal money system, stablecoins act like the cash register. When monetary policy shocks hit traditional markets, stablecoin liquidity can move too, which changes crypto market conditions even if on-chain narratives stay the same.

A BIS working paper on stablecoins and monetary policy found that US monetary policy shocks drive developments in both crypto and traditional markets, while traditional markets do not react much to crypto shocks in the other direction.

That supports the broader point that crypto is downstream of macro funding conditions more often than it wants to admit.

Why this “Japan story” keeps showing up in Bitcoin’s chart

Somewhere in Tokyo, there are insurers and pension managers staring at the same problem everyone is staring at, yield has returned, and it comes with volatility attached.

Somewhere else, there is a crypto trader in New York or London watching Bitcoin chop sideways, wondering why a move in Japanese bonds is pulling on their screen.

This is why.

Japan is changing the price of money after decades of holding it down. That adjustment is reaching into every corner where leverage and risk live, and crypto sits right there, liquid, global, always open, always ready to react.

If Japan’s bond market stays calm, crypto gets a cleaner runway.

If Japan’s long end keeps throwing off stress signals, the market is going to keep learning the same lesson, Bitcoin trades on the future, and the future is priced in yields.

The post Bitcoin is in the blast radius after Japan’s bond market hit a terrifying 30-year breaking point appeared first on CryptoSlate.

Canada's Prime Minister, Mark Carney, walked onto the World Economic Forum's Davos stage yesterday and said the quiet part out loud.

The rules-based order, the thing leaders love to invoke when they want the world to behave, is fading.

Carney called it a “pleasant fiction.”

He said we are living through a “rupture.”

He said great powers are using integration as a weapon, tariffs as leverage, finance as coercion, and supply chains as vulnerabilities to be exploited.

Then he reached for Václav Havel’s famous “greengrocer” from The Power of the Powerless, the shopkeeper who hangs a sign reading “Workers of the world, unite!” not because he believes it, but because he knows the ritual matters more than the words. It’s Havel’s shorthand for life under a system where everyone performs loyalty in public, even as they quietly recognize the lie.

He told the room, “It is time for companies and countries to take their signs down.”

The Davos audience cheered and clapped in response.

Perhaps, one can argue that they are trained to nod along. This week, they have extra reasons.

The talk around town has been about tariffs and coercion, and whether allies are about to be treated like revenue lines.

The mood is tied to President Trump escalating pressure around Greenland and tariff threats against European partners, a story that keeps resurfacing across conference chatter and the news cycle.

Carney’s slot was listed as a “Special Address” in the WEF run-up. His message landed in a room already primed for it.

Here is the part crypto people should not miss: when geopolitics becomes transactional in public, money stops being background infrastructure and starts feeling like a border.

That shift changes what people pay for.

It changes what investors store value in. It changes what counts as a safe option.

Bitcoin sits right in the middle of that feeling.

Not because it suddenly becomes a global settlement rail for trade invoices. It probably does not.

Not because it replaces the dollar in a clean, straight line. It almost certainly does not.

Bitcoin matters because it offers an option: a credible outside asset that is hard to block, hard to rewrite, and hard to gate behind somebody else’s permission.

In a stable world, that sounds ideological. In a rupture world, it starts to sound like risk management.

Carney even used the language of risk management. He said this room knows it. He said insurance costs money, and the cost can be shared.

Collective investments in resilience are cheaper than everyone building their own fortresses.

That is the Davos version of a truth every investor learns early: concentration risk feels fine until the day it does not.

The human part of this story, the moment you realize access can be conditional

Most people do not wake up wanting a new monetary system.

They wake up wanting their salary to clear, their bank transfer to arrive, their business to keep trading, and their savings to keep meaning something next year.

They also have a moment, sometimes it is a headline, sometimes it is a blocked payment, sometimes it is a currency shock, when they realize access can be conditional.

Carney’s speech is basically a map of how those moments multiply.

He talked about tariffs used as leverage.

He talked about financial infrastructure as coercion.

He talked about supply chains exploited as vulnerabilities.

“Over the past two decades, a series of crises in finance, health, energy and geopolitics have laid bare the risks of extreme global integration. But more recently, great powers have begun using economic integration as weapons, tariffs as leverage, financial infrastructure as coercion, supply chains as vulnerabilities to be exploited.

You cannot live within the lie of mutual benefit through integration, when integration becomes the source of your subordination.”

That is what a “rupture” feels like in everyday terms. Your costs move because of a speech in another capital. Your suppliers disappear because of a sanctions package. Your payment route gets slower because a bank somewhere decides your jurisdiction is riskier this month.

Even if you never touch crypto, that environment changes the way you value optionality.

Bitcoin is optionality with teeth.

It is not magic.

It does not make geopolitics disappear.

It does not exempt anyone from laws.

It does not stop volatility.

It does one simple thing: it exists outside most of the chokepoints that make modern finance such an effective tool of state power.

That is why this moment matters more than a single Davos speech.

Two Bitcoins show up in markets, the insurance one, and the liquidity one

If you want to talk about Bitcoin under a changing world order without slipping into slogans, you have to admit something that makes true believers uncomfortable.

Bitcoin has two personalities in markets.

- One is the insurance asset. People buy it because they worry about the rails, the long term, the shape of the world, and the rules. They want something that can move across borders as information.

- The other is the liquidity asset. In sudden shocks, Bitcoin trades like the thing that gets sold when people need dollars now.

That second personality is why “rupture” headlines can produce weird price action. The macro story gets scarier, and Bitcoin drops anyway.

The immediate response is a dollar grab: credit tightens, leverage unwinds, risk gets sold first, and questions get asked later.

There's a sequence: squeeze first, repricing later.

Tariffs as leverage, why the first wave can hurt Bitcoin, then help its story

Tariffs are more than a tax; they are a signal.

They tell markets the temperature of international relationships, they tell companies how stable their cost base will be, and they tell central banks how messy inflation might get.

This is where Carney’s argument about weaponized integration connects directly to Bitcoin’s near-term and long-term path.

If the latest tariff threats escalate into real measures, companies reprice supply chains, consumers see price pressure, and policymakers face uglier trade-offs.

The JPMorgan framing around tariffs is a reminder that they are not just politics. They are a macro variable that shows up in growth, inflation, and confidence.

In the first phase, markets often do what markets do. They go defensive, they prefer cash, they prefer the most liquid collateral, and they chase dollars.

Bitcoin can get dragged lower with everything else.

Then the second phase arrives.

Businesses and households realize this is not a one-off. They start paying for resilience. They diversify, build redundancy, and look for assets that sit outside the obvious pressure points.

That is where Bitcoin’s insurance narrative gains weight. Not everyone becomes a Bitcoin maximalist because they read the Bitcoin Whitepaper, but because a larger share of capital starts treating optionality as worth paying for.

Financial infrastructure as coercion, stablecoins live on the rails, Bitcoin sits outside them

Carney’s line about financial infrastructure matters because it points to the part of the crypto stack most people misunderstand.

Stablecoins are crypto, and stablecoins are also the dollar’s long arm.

They move fast, they settle cheaply, and they make cross-border value transfer easier. They also live inside an ecosystem of issuers, compliance, blacklists, and regulatory chokepoints.

That is beyond a moral judgment. It is the design, and it is also why stablecoins can scale.

In a world where financial infrastructure becomes more openly coercive, stablecoins can feel like a superhighway with more toll booths.

Bitcoin feels like a dirt road that still gets you out. That distinction becomes more important as countries and blocs start building their own resilience stacks.

Carney called it variable geometry: different coalitions for different issues. He talked about buyers’ clubs for critical minerals, bridging trade blocs, and AI governance among like-minded democracies.

You can see the same logic in the policy world around defense procurement, including Europe’s SAFE push.

It is about capacity, coordination, and optionality. Crypto will get pulled into that same orbit.

Some blocs will prefer regulated, surveilled rails. Some will build their own. Some will restrict foreign dependencies. Some will quietly keep a foot in every camp.

Bitcoin’s role in that environment is leveraged through existence.

If you can exit, even imperfectly, coercion becomes costlier to apply.

Middle powers, “third paths,” and why Bitcoin’s biggest impact might be psychological

Carney’s speech is a manifesto for middle powers: countries that cannot dictate terms alone, and that get squeezed when great powers turn the world into a bilateral negotiation.

He said negotiating alone with a hegemon means negotiating from weakness. He said middle powers have a choice: compete for favor, or combine to create a third path.

That is a geopolitical argument.

It also rhymes with what Bitcoin represents in finance.

Bitcoin is a third-path asset.

It is not the hegemon’s money. It is not a rival’s money. It is not a corporate ledger. It is not a treaty.

That matters most when trust is thin and alignment is messy, when alliances feel conditional, and when sovereignty sounds less like a principle and more like something you have to finance.

Carney stood with Greenland and Denmark in his remarks.

He opposed tariffs over Greenland, and called for focused talks on Arctic security and prosperity.

You do not have to take a view on Greenland to see the pattern. Trade tools are being discussed as leverage among allies in public.

When that happens, every CFO, every pension committee, every sovereign fund, and every household with savings gets a little more serious about tail risks.

That is what matters for us, the slow shift in what feels safe.

US President Donald Trump, speaking today, asserted that he “would not use force” to take Greenland but reiterated that he does still want to purchase the “big block of ice.” He reaffirmed that he expects Europe to support the purchase for world security reasons, but if it refuses, “the US will remember.”

Three forward scenarios for Bitcoin by 2030, “managed fragmentation,” “tariff spiral,” “rails fracture”

Carney called this a rupture.

He also warned against a world of fortresses and argued for shared resilience. Those are two different futures, and Bitcoin’s path looks different in each.

1) Managed fragmentation

Blocs form, standards diverge, and trade routes adjust. Coercion exists, but it stays bounded because everyone realizes escalation is expensive.

Bitcoin in this world trends upward as a portfolio's final insurance policy. Volatility remains.

Correlation to liquidity cycles remains. The structural bid grows because the world keeps paying for optionality.

2) Tariff spiral and dollar squeeze

Tariffs escalate, and retaliation follows.

Inflation uncertainty rises, central banks stay tight longer, and risk assets get hit. A dollar squeeze shows up.

Bitcoin here can look disappointing in the moment.

Price falls with leverage unwinds, narratives get mocked, then policy eventually shifts, liquidity returns, and the underlying reason people want an exit option becomes stronger.

3) Rails fracture

Financial coercion expands. Secondary sanctions and controls become more common. Cross-border payments get more politicized.

Some countries build parallel settlement stacks, some companies reroute exposure, and everyone pays more for friction.

Bitcoin’s insurance value is highest in this world because the cost of conditional access is highest.

Stablecoins still matter for commerce. Bitcoin matters for reserve optionality, for portability, and for the ability to move value when doors close.

This is also where regulation gets harsher. A fractured world tends to be a more suspicious world, and the easiest thing for states to tighten is anything that looks like capital flight.

Bitcoin’s upside here exists alongside higher enforcement pressure. That tension becomes part of the story.

The quiet tell, even Davos is arguing about resilience, not efficiency

The old globalization story was efficiency: just-in-time supply chains, single-point optimization, and frictionless capital.

Carney’s speech is about resilience, redundancy, shared standards, and variable coalitions.

And it is happening at Davos, the temple of integration. That is the tell. Even the “rules-based order” language is changing in public.

The WEF theme is still cooperation. The framing is still dialogue. And the agenda is full of resilience talk because the room knows the bargain Carney described is under strain.

Outside Davos, the news cycle reinforces the point.

The UN Security Council is still extending reporting around Red Sea attacks, reminding everyone that shipping lanes are strategic terrain. The UN record captures how persistent that risk remains.

The Venezuela tanker seizures covered by AP show hard power and economic control blending in the Western Hemisphere, too.

Le Monde’s report on a US-Taiwan deal around advanced chips and tariffs shows how industrial policy and trade are merging, even in sectors that used to be treated as pure economics.

Bitcoin does not cause any of this.

And it does not solve it.

It becomes more relevant because the world is changing around it.

What to watch next, five signals that the rupture thesis is becoming investable

A watchlist to remain alert:

- Tariff implementation dates, and whether threats turn into policy. The Greenland-linked tariff reporting is one real-time test.

- Signs of allies building redundancy stacks: defense procurement coordination, trade bridges, critical-minerals buyers’ clubs, and the policy plumbing that makes “shared resilience” real.

- Cross-border payments politics. Any move that makes access more conditional increases demand for outside options, and also increases pressure on crypto on-ramps.

- Energy and shipping risk. The Red Sea remains a live variable.

- Bitcoin’s behavior during stress. If it sells off first and rebounds when policy shifts, that fits the two-personality model. If it starts holding up during shocks, that signals the insurance bid is getting deeper.

The point Carney made, applied to Bitcoin

Carney’s speech was a warning about pretending, about “living within a lie,” about acting like the old system still works as advertised.

For Bitcoin, the parallel is simpler. People have treated money as plumbing for decades. They are starting to treat it like a geopolitical instrument again.

In that world, Bitcoin becomes easier to understand.

Not as a promise. Not as a religion. And not as a straight-line trade.

It becomes what it has always been underneath the hype: a volatile, imperfect, stubborn form of financial optionality.

A way to keep one window open when more doors start coming with terms and conditions.

The post Bitcoin is now your only lifeboat as Canada says the current world order is merely a “pleasant fiction” appeared first on CryptoSlate.

https://ambcrypto.com/feed/

SOL vs ETH: What staking ratios reveal about economic strength.

SOL vs ETH: What staking ratios reveal about economic strength. Bitcoin and altcoins rallied after Donald Trump said the US would delay planned tariffs following talks with NATO, easing geopolitical pressure on risk assets.

Bitcoin and altcoins rallied after Donald Trump said the US would delay planned tariffs following talks with NATO, easing geopolitical pressure on risk assets.https://beincrypto.com/feed/

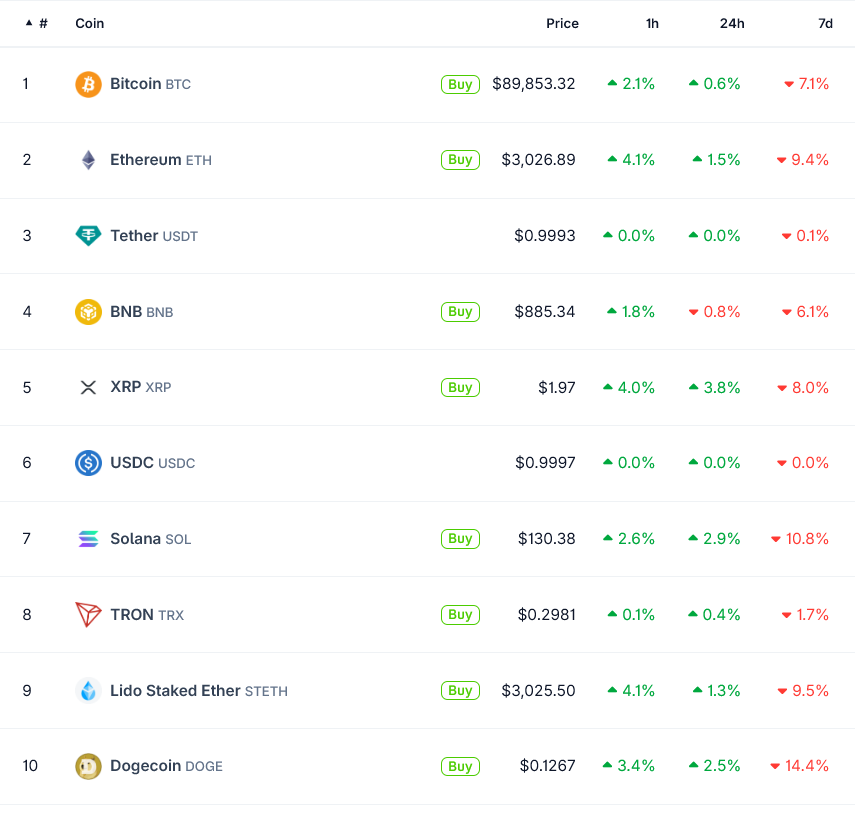

Bitcoin and global markets rebounded sharply after US President Donald Trump said he would not proceed with tariffs linked to Greenland. The announcement erased trade war fears that had rattled investors earlier in the day.

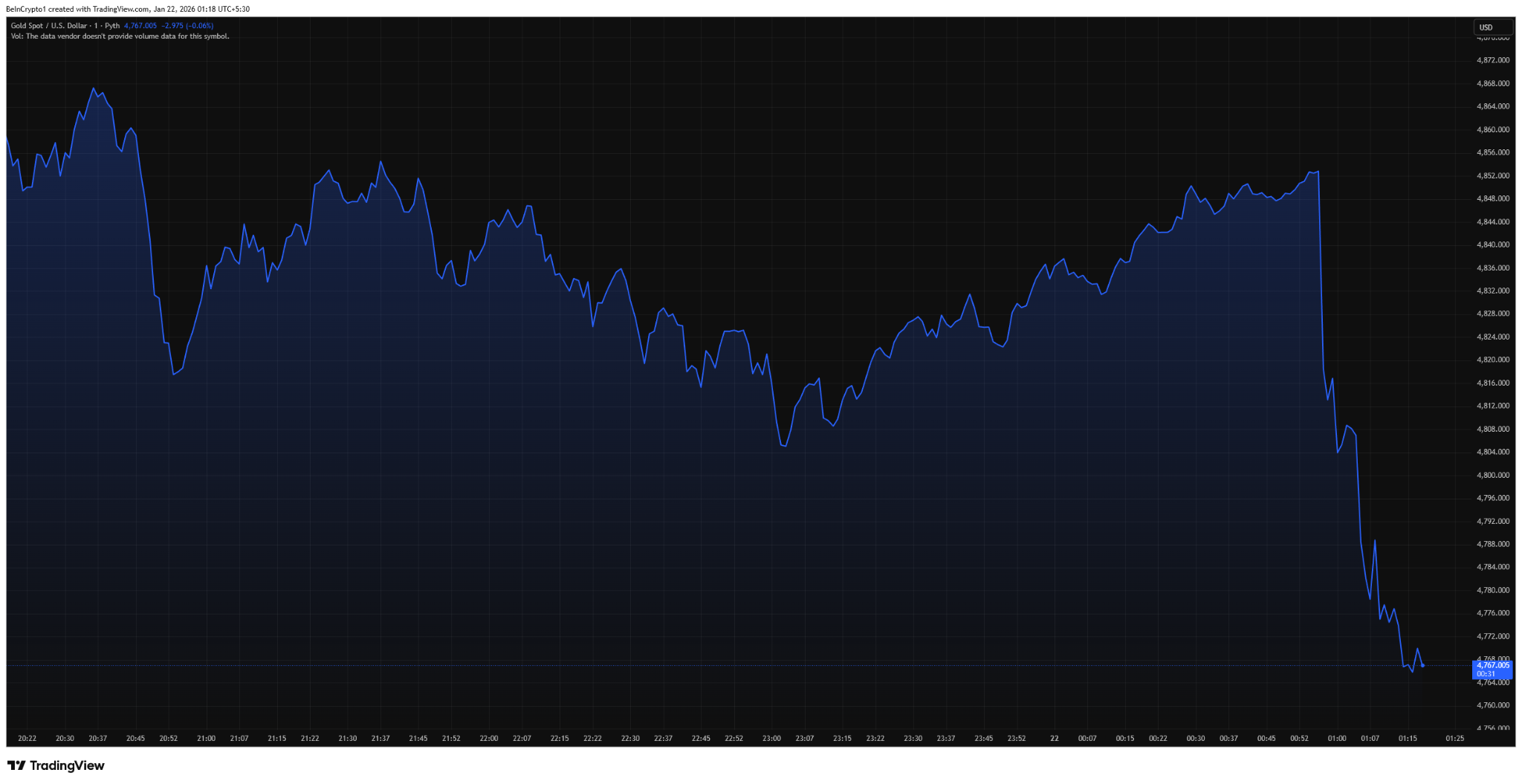

Bitcoin climbed back toward $90,000, recovering from intraday lows below $89,000, while Ethereum rebounded toward $3,000 after briefly slipping under that level. US equities also stabilized, with the S&P 500 turning higher following earlier losses. Gold, which had risen on geopolitical risk, pared gains.

Greenland Tariff Fears Had Driven Risk-off Moves

The market reaction followed Trump’s statement that a framework agreement had been reached with NATO Secretary General Mark Rutte, reducing the likelihood of imminent trade action against European allies.

Earlier in the session, markets sold off after Trump and senior US officials revived aggressive tariff rhetoric at the World Economic Forum in Davos.

Investors reacted to the renewed use of tariffs as a geopolitical lever, particularly after Treasury Secretary Scott Bessent defended tariffs as an effective negotiating tool.

Bessent warned foreign governments not to retaliate, saying, “Sit back, take a deep breath. Do not retaliate,” while reiterating that tariffs remain central to US economic and security strategy.

Crypto markets fell alongside equities as investors priced in higher inflation risks, tighter liquidity conditions, and renewed global trade uncertainty.

Bitcoin dropped below $90,000, while Ethereum slid under $3,000, reflecting crypto’s sensitivity to macro risk shocks.

As that risk fades with the latest update from the US president, markets have shifted. Risk assets show early signs of recovery. Meanwhile, Gold prices immediately dropped following the announcement.

Reversal Validates Macro-Driven Crypto Flows

The rapid recovery highlights how closely crypto markets are now tied to macro and policy signals, particularly around inflation and trade.

Earlier analysis showed that tariffs imposed over the past year have largely been absorbed by US consumers. The data reinforced concerns that renewed trade escalation could delay rate cuts and tighten financial conditions.

That backdrop had already weighed on digital assets since October, contributing to range-bound price action and repeated failed rallies above key resistance levels.

Once the immediate tariff threat was removed, risk appetite returned, triggering short-covering and spot buying across crypto and equities. The S&P 500 erased losses, while Bitcoin stabilized after a volatile session.

While markets welcomed the de-escalation, uncertainty remains. Trump said further discussions are ongoing regarding Greenland’s strategic role in missile defense and Arctic security, suggesting the issue is not fully resolved.

The post Trump Calls Off Greenland Tariffs, Markets Rebound as Risk Fades appeared first on BeInCrypto.

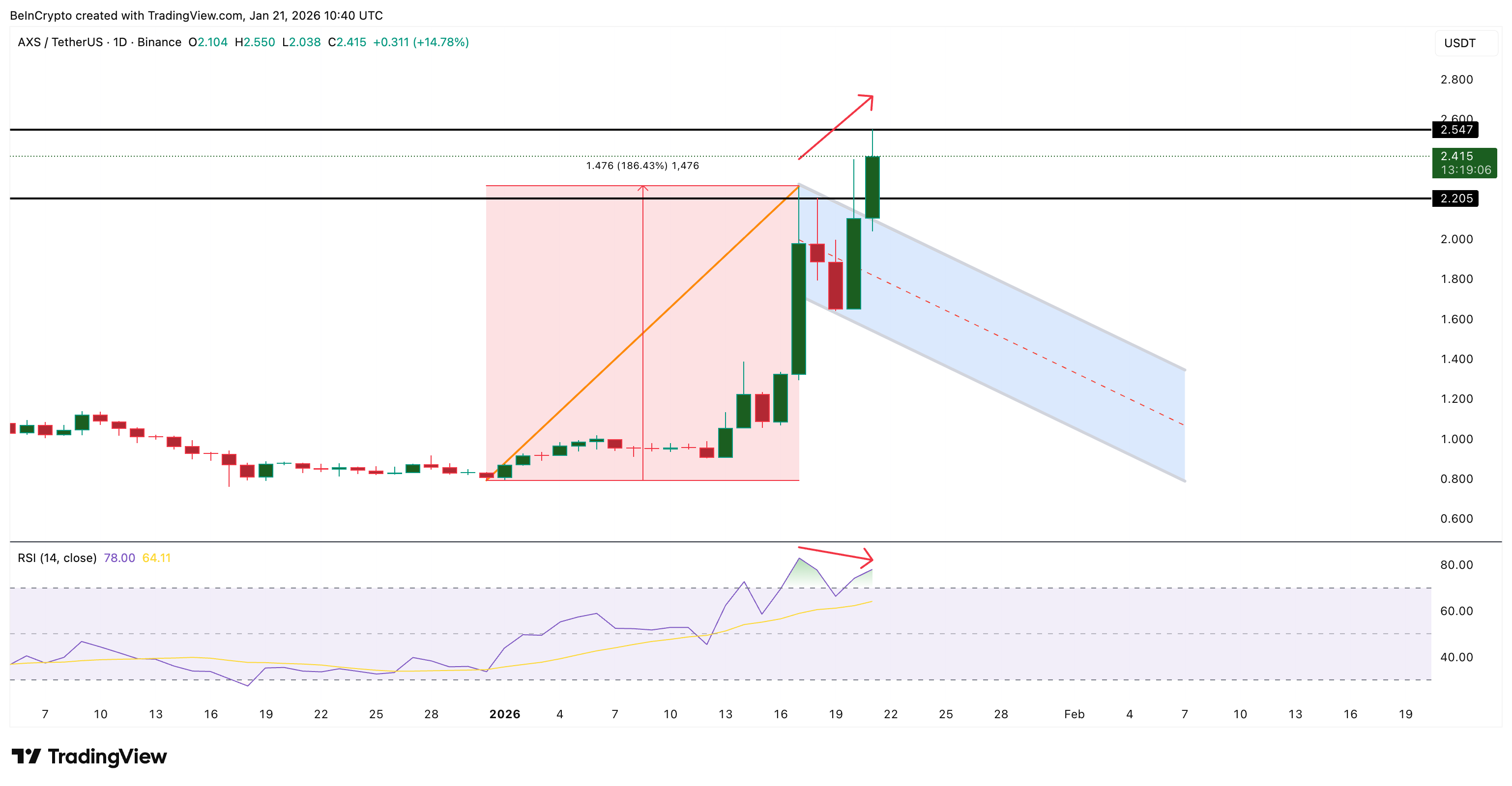

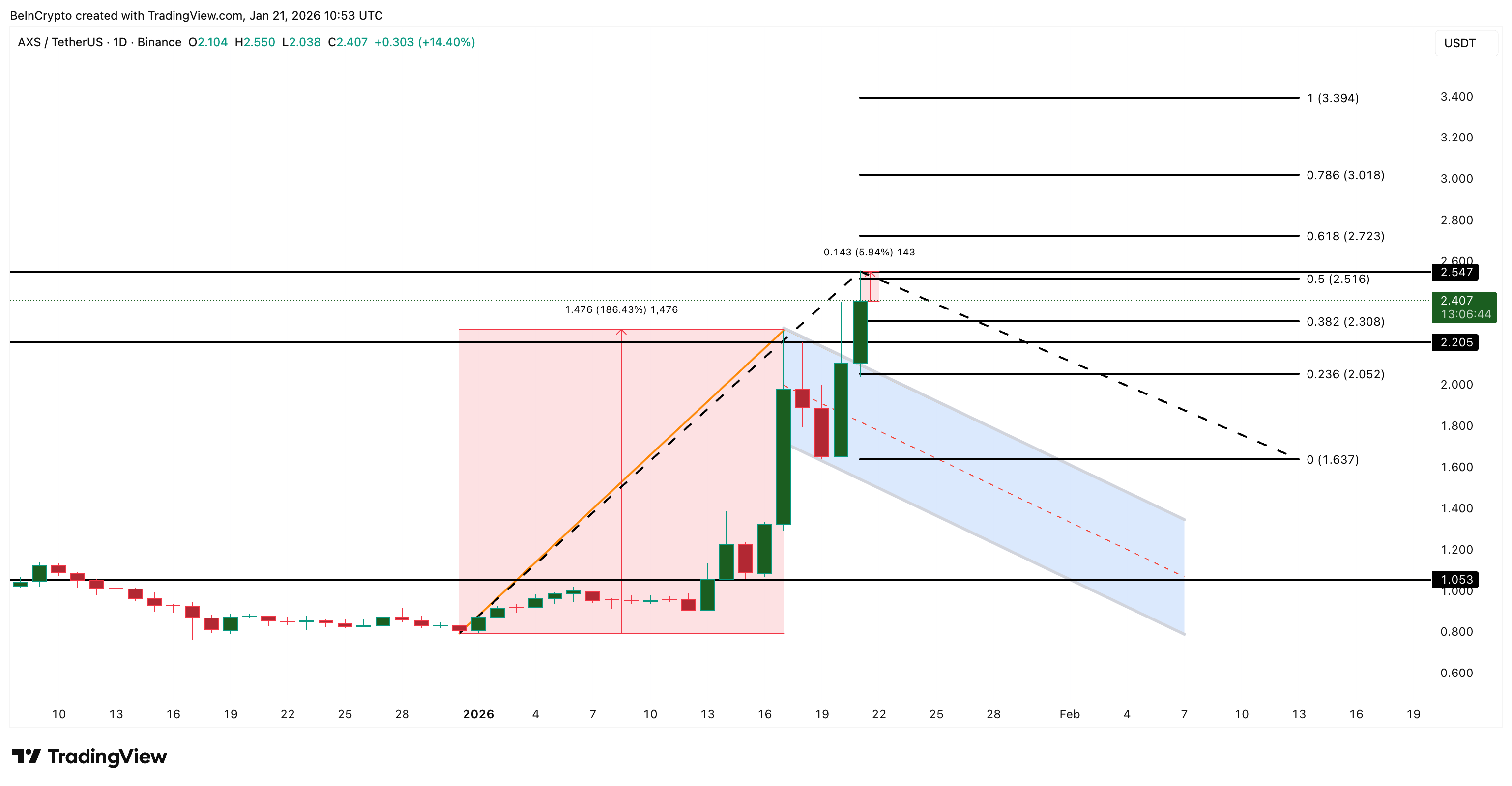

Axie Infinity is having a strong day. AXS is up about 17% today, confirming the breakout that was flagged earlier. With this move, the token is now up roughly 180% month-on-month, putting it among the top performers in the GameFi space.

But big rallies often raise one uncomfortable question. Is this strength real demand, or is it providing exit liquidity for larger holders? The charts and on-chain data point to a more complex answer.

Breakout Confirms, but Momentum Starts to Cool

The AXS price breakout itself was clean.

AXS broke out of a bullish flag after a few sessions of consolidation. Price rallied to a high near $2.54, a move of roughly 168% from the base. But the reaction at $2.54 matters.

Price was sharply rejected, leaving a long upper wick. That wick signals active selling, not passive profit-taking. It establishes $2.54 as a real supply level.

Momentum now adds a warning.

Between January 17 and January 21, the AXS price seems to be printing higher price highs while RSI is forming a lower high. RSI measures momentum by comparing recent gains and losses. When the price rises, but the RSI weakens, upside strength is fading, a pattern known as bearish divergence. For divergence confirmation, the next candle needs to form below $2.54, while the RSI stays lower than the last peak.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

This developing bearish divergence does not invalidate the breakout.

It suggests that continuation now requires new demand, not just the momentum of earlier buyers. Without it, the rally is vulnerable to a pullback, pause, or even reversal.

Big Holders Sell Into Strength While Short-Term Buyers Chase

On-chain data explains why the rally looks unstable.

Since January 13, AXS price climbed from about $0.95 to $2.39, a gain of roughly 151%. Over the same period, whale supply fell from 255.16 million AXS to about 244 million AXS. That means whales sold roughly 11.2 million AXS, or about 4.4% of their holdings, directly into rising prices.

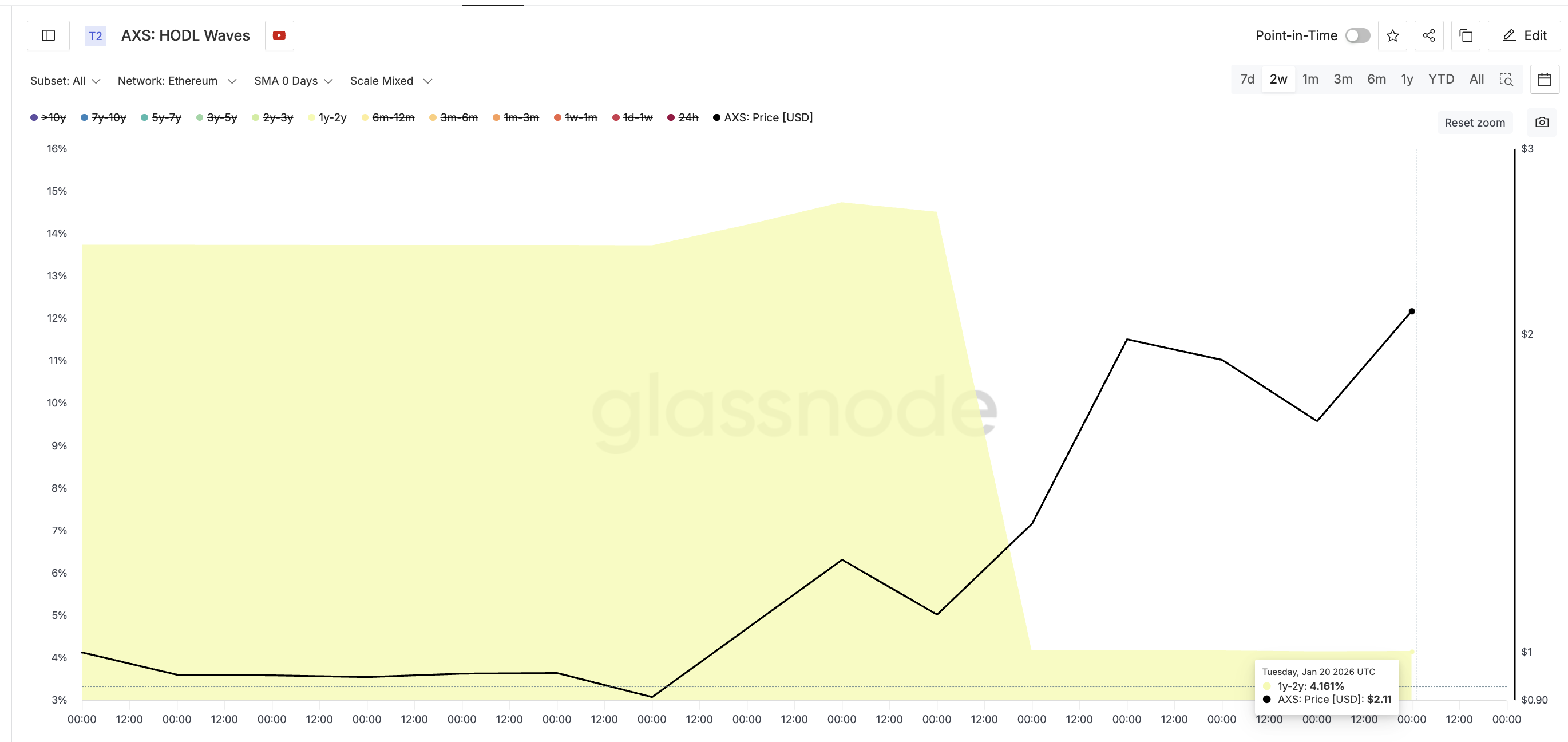

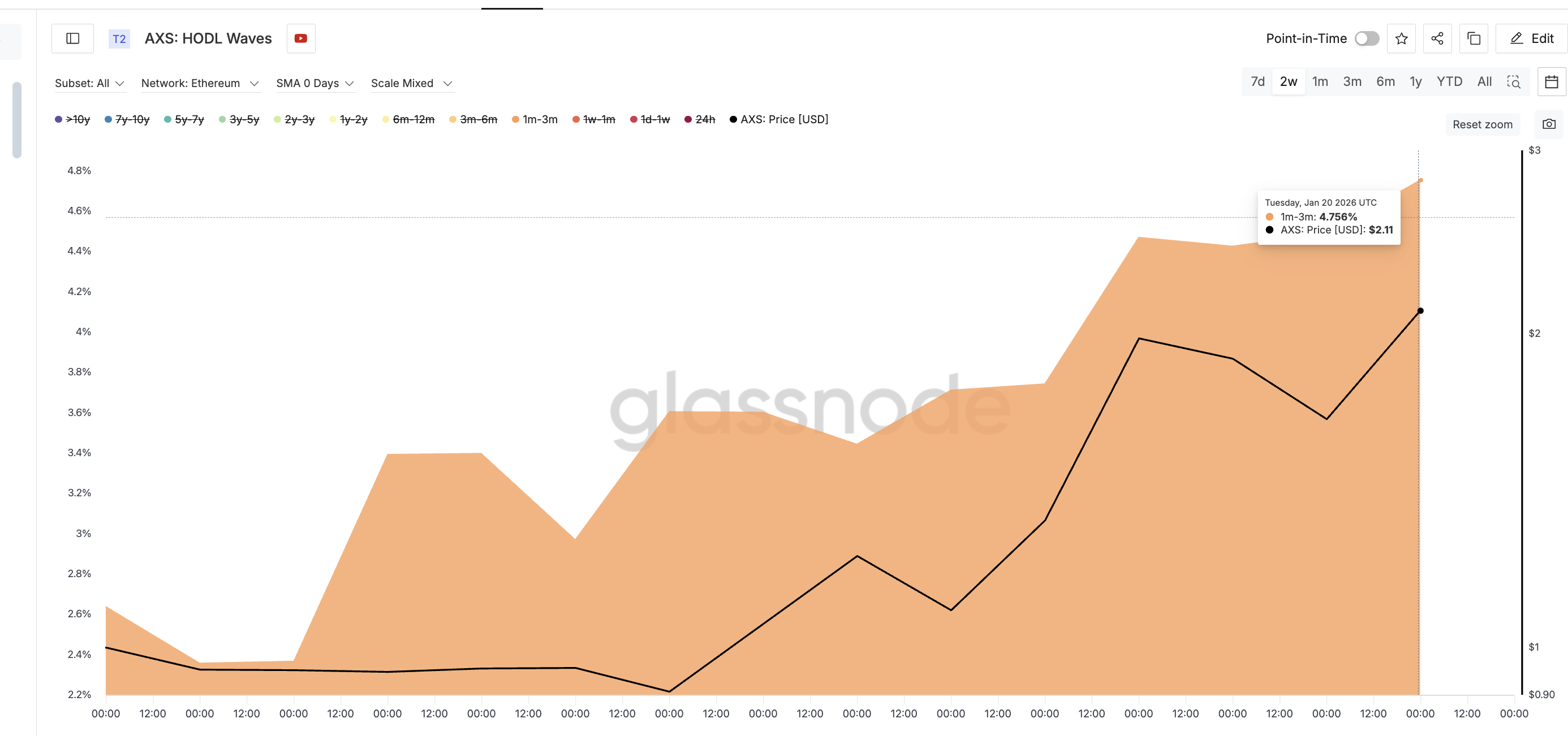

HODL waves confirm this behavior.

HODL waves track how long coins have been held and show which holder groups are increasing or decreasing supply. The 1-year to 2-year cohort dropped sharply, falling from 13.73% of the total supply to about 4.16%. Long-term holders are using this rally to reduce exposure, not build it.

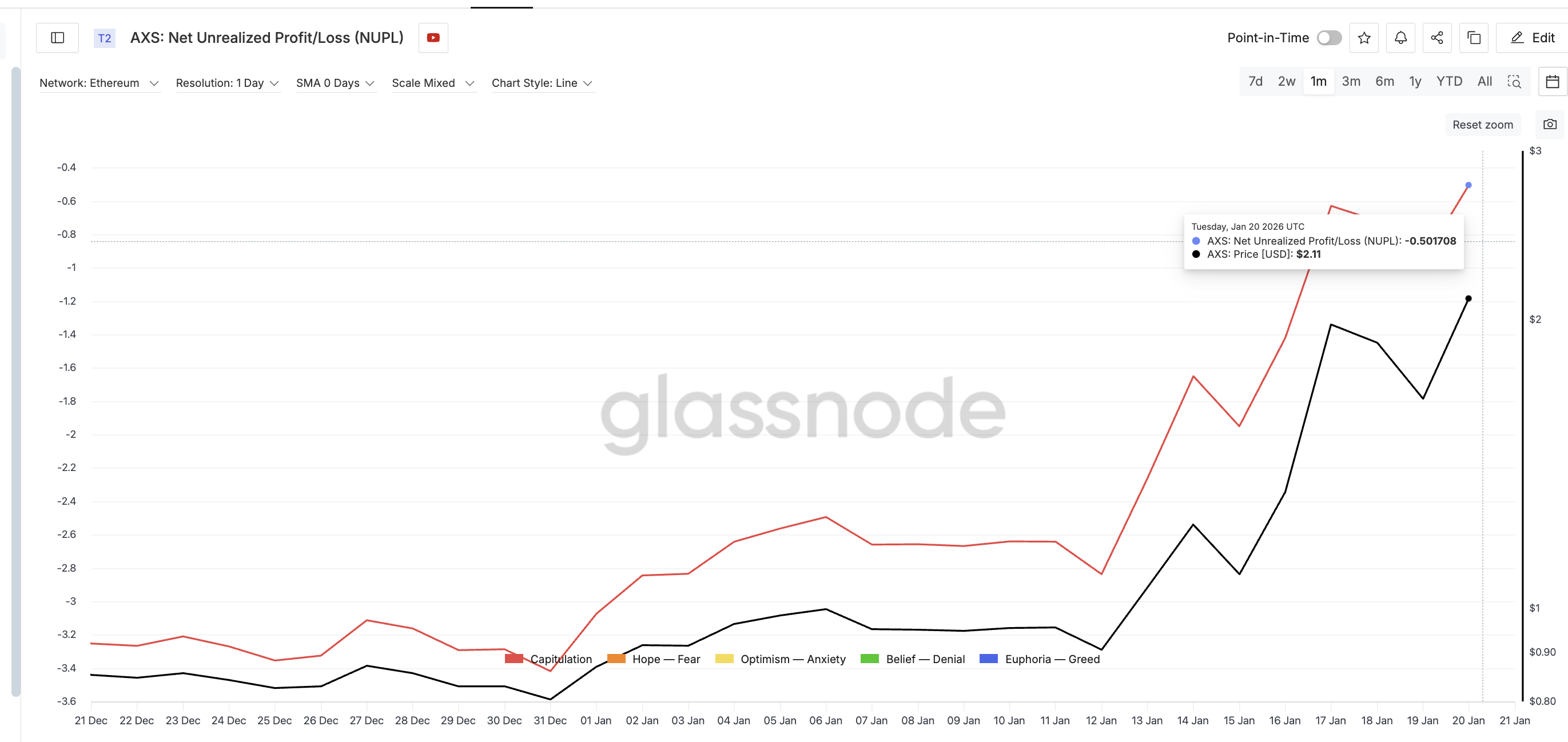

NUPL explains why this is happening now. Net Unrealized Profit/Loss (NUPL) measures whether holders are sitting in profit or loss. A negative value means holders are still underwater. For AXS, NUPL remains deep in the capitulation zone, but the intensity of losses is easing.

Since late December, NUPL has improved from roughly −3.4 to around −0.5. In simple terms, holders are still selling at a loss, but each price rally reduces that loss. That creates strong incentives to sell into strength to recover capital.

Short-term holders are doing the opposite. The 1-month to 3-month cohort increased its share from 2.64% to 4.76%, an increase of over 80%. These buyers are chasing momentum, not recovering losses.

This is the classic exit-liquidity structure. Long-term holders and whales sell as losses shrink, while short-term traders buy, expecting a fast continuation.

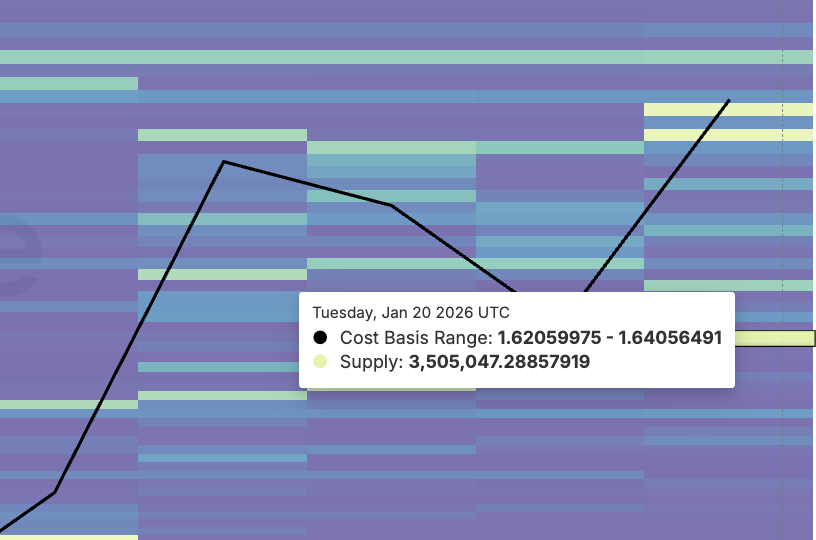

Cost Basis And AXS Price Levels Show Where Exit Liquidity Turns Risky

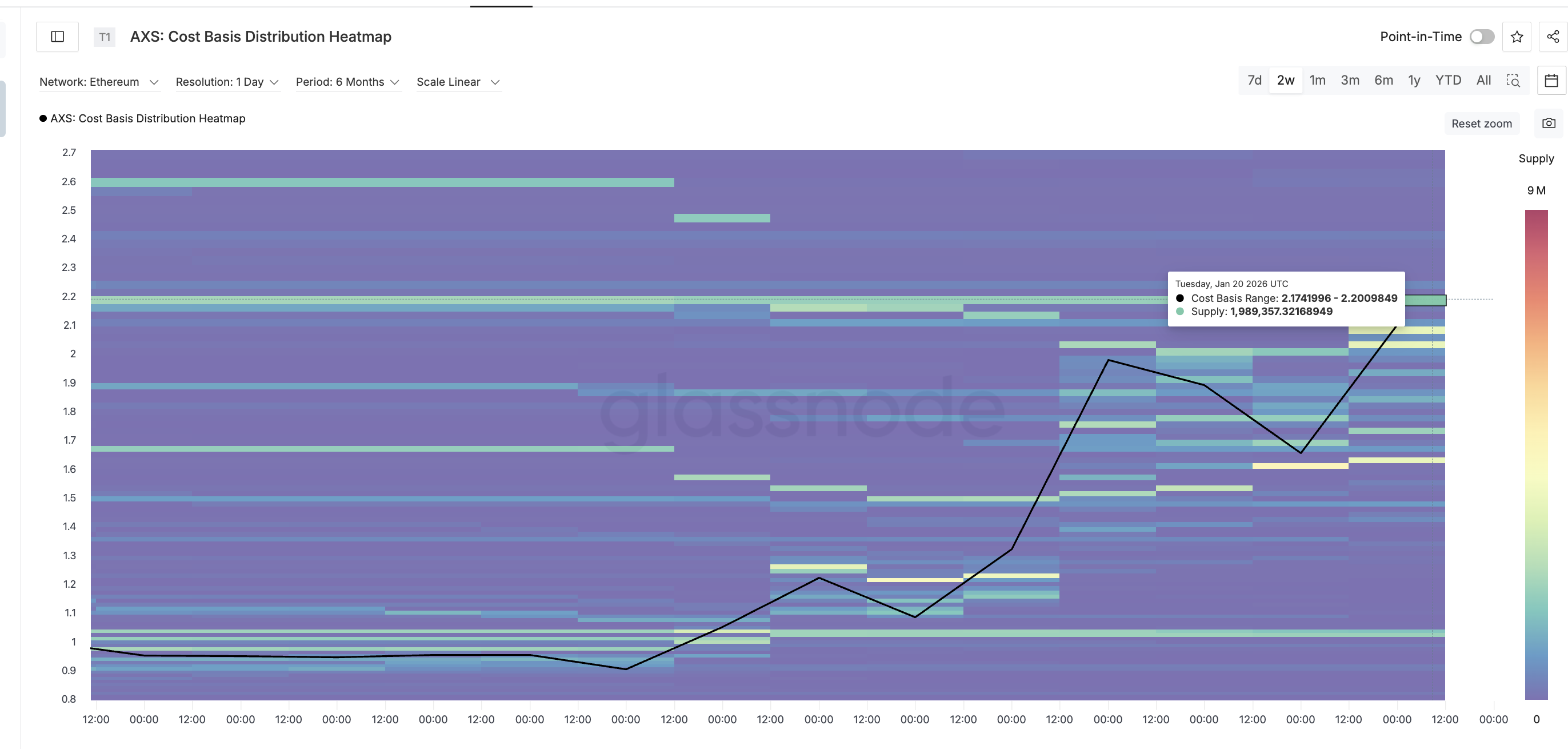

Cost basis data shows where this GameFi setup holds or breaks.

The most important near-term support sits at $2.17–$2.20, a level also on the price chart. Roughly 1.99 million AXS were accumulated in this range. As long as price holds above it, pullbacks remain corrective.

Below that, the strongest structural support lies at $1.62–$1.64, where about 3.50 million AXS were accumulated. A break below $1.63, a level on the price chart, would signal that short-term buyers are trapped and the breakout structure is failing.

On the upside, bulls need a clean daily close above $2.54, roughly 6% above current levels, to reopen the path toward $2.72 and potentially $3.01.

Until that happens, upside moves are likely to meet selling pressure rather than acceleration.

The post Is The 180% Axie Infinity (AXS) Rally Just Exit Liquidity For Holders? Charts Have The Answer appeared first on BeInCrypto.

https://cryptonewsz.com/feed/

https://www.newsbtc.com/feed/

PEPE is finally entering a critical phase as recent price action suggests the market is actively pushing out bears ahead of a potential structural shift. Pseudonymous crypto analyst ‘The Composite Trader’ argues that the move is less about immediate upside and more about completing a controlled reversal process and preventing any further downside.

In an X post this Tuesday, The Composite Trader updated a setup he first outlined on January 5, explaining that PEPE’s sharp bullish expansion at the start of the year was never meant to be sustained. He labeled the move as manipulative and stated that a price reversal toward a yearly open was the intended outcome.

PEPE Stages Reversal Move To Force Out Bears

His accompanying chart supports this narrative by illustrating a brutal downtrend that began in late 2025, with PEPE plummeting nearly 50% before following a descending curved channel. The analyst highlighted a Break of Structure (BOS) at a lower level in the pattern, followed by a short-lived rally into the $0.0065-$0.0075 region. This upward move was explicitly labeled “manipulation” on the chart, pushed higher to hunt for buy-side liquidity, with no real demand to sustain higher prices.

Related Reading: Why Meme Coins Like PEPE And FARTCOIN Are Ready To Explode

According to the analyst, PEPE’s ongoing reversal process is designed to force out current bearish positions before any confirmed trend change. The chart shows that the meme coin has already corrected by roughly 33.21%, wiping out some of the gains it achieved earlier this year. This move aligns closely with The Composite Trader’s earlier expectation that the yearly open would be challenged, confirming the market’s downward momentum.

The analyst also noted that similar price patterns are emerging across other altcoin pairs, reflecting the broader impact of whale-driven movements. He has emphasized the importance of understanding the timing behind these reversals, suggesting that not every price shift signals a sustainable uptrend.

Furthermore, the Composite Trader has said that accumulation schematics and bullish reversals for PEPE will be confirmed when the time is right. Until then, the market remains bearish with strategic price corrections, requiring patience from investors and traders.

Analyst Predicts More Decline For PEPE Price

Crypto analyst Davie Satoshi has also shared insights on PEPE’s price behavior and its potential next moves. He predicts that PEPE could decline even further if Bitcoin crashes to $85,000 and $75,000. Based on his analysis, PEPE’s price movement is now closely tied to BTC, and the lower Bitcoin goes, the more likely PEPE will follow.

Excluding PEPE, Satoshi forecasts that all meme coins could enter a downtrend if Bitcoin declines. Despite this bearish outlook, he believes PEPE will likely rebound and move back up. The analyst expects the meme coin to reverse sharply and find new support levels. He advises non-PEPE holders to take advantage of the current downtrend by buying the dip.

XRP is taking a decisive step toward institutional relevance as Flare Networks unveils new infrastructure designed to support enterprise-grade financial use cases. For years, XRP has been recognized for its speed and efficiency in cross-border payments, and XRP has often been discussed as a liquidity asset, but with limited programmability and on-chain utility. Flare’s latest move changes that equation, unlocking new layers of functionality that position XRP as more than just a settlement token.

How Flare Expands XRP Smart Contract Capabilities

Flare Networks is taking concrete steps to activate XRP for institutional-grade financial infrastructure. In a recent Genfinity interview that was revealed on X, the Flare Networks team breaks down how its infrastructure is enabling traditionally idle digital assets, starting with XRP, to participate in a programmable financial system.

The conversation focuses on execution rather than theory. This includes bringing FXRP live, integrating directly with wallets, custodians, exchanges, and removing technical friction so that participation won’t require users to manage on-chain technical complexity. Flare’s strategy is not about an isolated pilot experiment, but about building durable infrastructure that can scale across different users, assets, and environments.

A core design principle is risk abstraction at the protocol level, through platforms like Firelightfi, where exposure is structured, collateralized, allowing larger participants to engage with clearer parameters, predictable outcomes, and stronger operational safeguards.

This approach shifts participation from speculative usage toward structured financial activity. The discussion makes it clear that XRP is the first implementation, not the final destination. However, the Flare broader objective is to activate multiple digital assets within a unified framework that prioritizes usability, security, and seamless integration into existing financial workflows. As highlighted in the Genfinity interview, this approach reflects the current stage of digital asset infrastructure, transitioning from experimentation toward real-world execution.

What This Means For The Future Of XRP And Tokenized Media

Crypto analyst Skipper_xrp has mentioned that SBI Group President Yoshitaka Kitao emphasized that Ripple is no longer just building products; it is creating a full-stack financial ecosystem with XRP and RLUSD integrated into every layer of its infrastructure.

The vision is already moving into execution as Ripple Labs has confirmed its collaboration with major Japanese financial institutions to launch a high-profile innovation program aimed at professionalizing the XRP Ledger ecosystem.

Meanwhile, BXE Token is preparing to debut on a US-regulated exchange with more than 12 million users and over $900 billion in annual trading volume, alongside compliance coverage across 49 countries. At the same time, decentralized media platforms are preparing for the US market.