Financial RSS Feeds

https://www.investing.com/rss/news.rss

https://cointelegraph.com/rss

The Bitcoin price rally to $90,000 failed to hold after 17,000 BTC were sent to exchanges, but an improving spot market suggests that traders view BTC’s current pricing as discounted.

Natix and Valeo are building a decentralized, self-driving camera model to offer a transparent foundation for the safe mainstream deployment of physical AIs.

https://www.coindesk.com/arc/outboundfeeds/rss/

https://cryptobriefing.com/feed/

Chainlink acquires Atlas to enhance SVR protocol, scaling on multiple blockchains and boosting MEV recapture for DeFi protocols.

The post Chainlink acquires Atlas to power DeFi liquidation auctions across more blockchains appeared first on Crypto Briefing.

The launch of this ETF highlights growing investor demand for assets that hedge against inflation and currency devaluation, impacting global markets.

The post Bitwise launches new ETF targeting Bitcoin, gold, and mining equities appeared first on Crypto Briefing.

https://bitcoinist.com/feed/

The idea of a cryptocurrency like XRP competing directly with global banks once sounded unrealistic, but that line is starting to blur. Ripple, the payments technology company behind XRP, has spent recent months pushing deeper into payments, liquidity, custody, and treasury infrastructure with acquisitions.

This has seen the role of XRP changing from a settlement token into something that increasingly mirrors core banking functions. The question is no longer whether Ripple can coexist with global banks, but what changes if it begins competing head-on with them.

A Strategic Challenge For Banks

Recent acquisitions and commentary across the global financial landscape have seen conversations about XRP’s role as a cross-border settlement token change into what might happen if Ripple starts competing with banks. Ripple has completed several high-profile acquisitions in recent months that extend its reach into treasury services, trading infrastructure, stablecoin rails, and custody, and each of these deals speaks to a broader strategy.

One of the most consequential moves was Ripple’s purchase of Hidden Road in April 2025. Hidden Road is a global prime broker that clears trillions annually and serves more than 300 institutional clients. With Hidden Road, which now operates as Ripple Prime, Ripple is now in charge of a multi-asset clearing, prime brokerage, and financing business.

Another significant acquisition was that of GTreasury, a treasury management platform bought for about $1 billion in October 2025. Ripple also agreed to acquire Rail, a stablecoin payments platform, for around $200 million in August 2025. Integrating Rail’s stablecoin-focused technology strengthens Ripple’s broader payments ecosystem and helps better position its stablecoin, Ripple USD (RLUSD).

That acquisition sits alongside other strategic deals completed in recent months, such as the purchases of Palisade and, most recently, Sydney-based fintech firm Solvexia on January 6, 2026 by GTreasury.

Can Ripple Start Competing With Major Banks?

Ripple has always been clear about its stance of competing with SWIFT as the leading global messaging network for financial institutions across the globe. Ripple’s CEO, Brad Garlinghouse, noted that the company plans to capture up to 14% of SWIFT’s current cross-border volume within the next five years.

Ripple’s partnerships with over 300 banks and financial institutions around the world already show how its blockchain rails are being used to speed cross-border settlement and manage liquidity efficiently. Many partners use RippleNet’s messaging for faster transfers, and those that use XRP often do so to tap into liquidity corridors that eliminate the need for massive prefunded accounts on both ends of a transaction.

Vincent Van Code, a popular crypto commentator on X, noted that Ripple is now encroaching on banks’ multi-trillion-dollar treasury, remittance, and custody revenue streams, areas that have historically been protected by legacy infrastructure. Ripple was held back for years by external constraints, but those barriers are now giving way and all the strategic pieces are beginning to fall into place.

Most banks are working on outdated systems and will soon be forced to rebuild their infrastructure from the ground up, a process that could cost between $3 billion and $4 billion per institution just to remain competitive.

Ethereum (ETH) has stabilized above the $3,000 mark after a sharp sell-off earlier this week, as large holders increased their exposure during the dip. The recovery follows a volatile period in which ETH briefly fell below key technical levels, triggering liquidations and renewed caution across the broader crypto market.

On January 22, Ethereum was trading around $3,003, up roughly 1.3% over 24 hours. The rebound came after ETH dropped nearly 13% between January 19 and 21, touching the $2,900 area for the first time in four weeks.

That decline coincided with heightened macro uncertainty, ETF outflows, and the liquidation of over $480 million in bullish leveraged positions.

Ethereum Accumulation Contrasts With Cautious Positioning

On-chain data shows that large Ethereum holders accumulated aggressively during the recent downturn. Whale balances increased by roughly 290,000 ETH over a two-day period, representing purchases worth close to $360 million at current prices.

This behavior suggests that some long-term investors view the recent pullback as a buying opportunity. However, other indicators point to a more cautious stance among experienced traders.

The smart money index remains below its signal line, a level that has historically been crossed ahead of stronger upside moves. In previous instances, such confirmations preceded double-digit gains, but no such signal has emerged so far.

Derivatives data support this wait-and-see approach. ETH perpetual futures funding rates briefly turned negative, indicating reduced confidence among leveraged traders. Options markets have also shown increased demand for downside protection after repeated rejections near the $3,400 level over the past two months.

Technical Structure Highlights Tight Trading RangeFrom a technical perspective, Ethereum is trading within a symmetrical triangle on the daily chart.

Momentum indicators show a bullish divergence, the relative strength index has formed higher lows while the price made lower lows between November and mid-January. This pattern suggests that selling pressure may be weakening, though confirmation is still lacking.

The immediate level to watch on the upside is $3,050, a former support zone that ETH lost during the recent sell-off. A sustained daily close above this level would indicate short-term stabilization.

Above that, the $3,146–$3,164 range represents a dense supply zone, where approximately 3.4 million ETH have been accumulated. This area is expected to act as a strong resistance.

Related Reading: Bitcoin Took Top Spot In 2025 Crypto Payments, Litecoin Third-Most Used: CoinGate

On the downside, failure to hold the triangle’s lower boundary near $2,910 could open the door to a deeper move toward the $2,610 support area.

Cover image from ChatGPT, ETHUSD chart on Tradingview

https://cryptoslate.com/feed/

Pierre Rochard's call for the Federal Reserve to integrate Bitcoin into its stress tests came at an unusual moment: the Fed is soliciting public comment on its 2026 scenarios while simultaneously proposing new transparency requirements for how it builds and updates those models.

The timing creates a natural question that has nothing to do with whether Rochard's specific claims hold up: can the Fed ever treat Bitcoin as a stress-test variable without “adopting” it as policy?

The answer isn't about ideology. It's about plumbing.

The Fed won't mainstream Bitcoin because a former strategy chief asks nicely. But if bank exposures to Bitcoin through custody, derivatives, ETF intermediation, or prime-brokerage-style services become large enough to move capital or liquidity metrics in a repeatable way, the Fed may eventually be forced to model BTC price shocks the same way it models equity drawdowns or credit spreads.

That shift wouldn't signal endorsement. It would signal that Bitcoin had become too embedded in regulated balance sheets to ignore.

What stress tests actually test

The Fed's supervisory stress tests feed directly into the Stress Capital Buffer, the amount of capital large banks must hold above regulatory minimums.

The tests project losses and revenues under adverse scenarios, then translate those projections into required capital. Scenario design matters because it determines comparability across firms: banks that face the same hypothetical shock are evaluated on the same terms.

For 2026, the Fed proposed scenarios that run from the first quarter of 2026 through the first quarter of 2029 and use 28 variables.

The set includes 16 US metrics: six activity indicators, four asset prices, and six interest rates.

Internationally, the Fed models 12 variables across four blocs: the euro area, the UK, developing Asia, and Japan. The models track real GDP, inflation, and exchange rates in each.

| Subhead | Variables | Count |

|---|---|---|

| Economic activity & prices | Real GDP growth; Nominal GDP growth; Real disposable personal income growth; Nominal disposable personal income growth; CPI inflation (CPI-U); Unemployment rate | 6 |

| Asset prices / financial conditions | House price index; Commercial real estate (CRE) price index; Equity prices (U.S. Dow Jones Total Stock Market Index); Stock market volatility (VIX) | 4 |

| Interest rates | 3-month Treasury rate; 5-year Treasury yield; 10-year Treasury yield; 10-year BBB-rated corporate yield; 30-year fixed mortgage rate; Prime rate | 6 |

The Fed explicitly noted that the 2026 set is identical to the 2025 set. Bitcoin isn't in it.

Banks with large trading operations face an additional global market shock component that stresses a broader set of risk factors, such as equity indices, credit spreads, commodity prices, foreign exchange, and volatility surfaces.

Banks with substantial trading or custody operations are also tested under a counterparty default scenario.

These components offer a natural entry point for Bitcoin: the Fed could fold a BTC shock into the global market shock framework without treating it as a core macroeconomic variable.

| Country / bloc | Real GDP (growth) | Inflation (CPI or local equivalent) | USD exchange rate (level) |

|---|---|---|---|

| Euro area | Euro area real GDP growth | Euro area inflation | USD/euro |

| United Kingdom | U.K. real GDP growth | U.K. inflation | USD/pound |

| Developing Asia | Developing Asia real GDP growth | Developing Asia inflation | F/USD (index) |

| Japan | Japan real GDP growth | Japan inflation | yen/USD |

What would make Bitcoin eligible

Four criteria would need to align before the Fed treats Bitcoin as a scenario input, and none of them requires the Fed to take a position on Bitcoin's long-term viability.

The first is materiality. Exposures must be large enough to move post-stress capital ratios meaningfully. The Fed's own transparency proposal discusses “material model changes” in terms of their impacts on projected Common Equity Tier 1 ratios, with thresholds ranging from 10 to 20 basis points.

That's not a Bitcoin-specific benchmark, but it's a realistic yardstick for “big enough to matter.” If a 50% Bitcoin drawdown paired with a volatility spike could push a bank's projected CET1 ratio down by 20 basis points, the Fed has a supervisory reason to model it.

The next criterion is repeatability. The shock must show up as a recurring driver of losses or liquidity stress, not a one-off headline.

Bitcoin's history of sharp drawdowns, often coinciding with equity selloffs and tighter funding conditions, provides the Fed with a benchmark to calibrate against. If Bitcoin behaves like a levered risk-on asset during stress episodes, it starts to look like other factors the Fed already models.

Then comes mapping into bank balance sheets. The Fed needs a clean transmission channel from a Bitcoin move to profit-and-loss or liquidity for regulated firms.

Plausible channels now include broker-dealer intermediation for ETFs, custody, riskless principal execution, and derivatives margining.

The last is data auditability. The Fed needs a defensible, monitorable series.

Bitcoin increasingly has institutional-grade reference points, such as BlackRock's IBIT, which references the CME CF Bitcoin Reference Rate. That makes Bitcoin easier to define in a stress scenario than many niche credit markets.

Why now feels different

Three developments in 2025 lowered the barriers to bank-adjacent Bitcoin activity and made future stress-test inclusion more plausible.

The Fed withdrew prior guidance on crypto-asset activities and shifted to “normal supervisory process” monitoring. The OCC issued guidance on crypto-asset safekeeping and, in Interpretive Letter 1188, confirmed that national banks may conduct riskless principal crypto-asset transactions.

The SEC rescinded Staff Accounting Bulletin 121 via SAB 122, removing an accounting treatment widely viewed as a custody roadblock for banks.

ETFs are now a bank-adjacent market structure. BlackRock's IBIT alone reported $70.24 billion in net assets as of Jan. 20.

The Banque de France noted that ETF authorized participants are often broker-dealer subsidiaries of US global systemically important banks, and that some US G-SIBs reported more than $2.7 billion in crypto-ETF investments by end-2024.

Authorized participants create and redeem ETF shares, hedge flows, and provide liquidity, which are activities that sit on regulated balance sheets and can transmit Bitcoin volatility into funding and margin pressures.

The Fed is also in an unusual transparency and comment cycle heading into 2026. It published proposed scenarios and explicitly asked for public comment. It issued a separate proposal on stress-test transparency and public accountability, outlining new documentation requirements and a cadence for reviewing material model changes.

This posture makes exploratory scenario components, such as testing emerging risks without embedding them in binding capital requirements, more institutionally plausible than they were before.

What changes if Bitcoin gets included

Including Bitcoin in stress tests wouldn't constitute endorsement. It would standardize how banks model crypto-related risks and eliminate the current patchwork of ad hoc proxies, such as equity volatility plus tech drawdowns.

Additionally, banks would get a common path to compare against, improving comparability across firms.

It would also implicitly mainstream Bitcoin as a modeled risk factor. Once the Fed treats Bitcoin like interest rates or equity indices, something that can transmit stress and must be projected under adverse conditions, it becomes harder to dismiss crypto exposures as fringe activities.

That shift could tighten controls and compliance around crypto-facing business lines.

Banks would treat those activities more like other capital-sensitive businesses: tighter limits, governance, model validation, documented hedging assumptions, and more granular data collection.

The Fed already has the latitude to add scenario components based on a bank's activities and risk profile. Bitcoin could arrive first as a targeted component for banks with meaningful crypto intermediation rather than as a universal macro variable.

That tier structure offers a natural path forward.

How Bitcoin could enter the stress-test framework

Three implementation tiers seem plausible over time, each triggered by growing bank exposure.

Tier 1 is a trading-book Bitcoin shock inside the global market shock, and is the most likely first step.

Crypto-linked trading, hedging, and ETF facilitation at G-SIB broker-dealers would trigger a Bitcoin spot shock, a volatility shock, and a basis/liquidity shock that feed margin and counterparty exposures. This is exactly the kind of component stress test that stress tests already use for other asset classes.

Historically consistent ranges might include a 50% to 80% Bitcoin drawdown over a short horizon, implied volatility doubling or tripling, and liquidity demand spikes tied to price gaps and margin calls.

Tier 2 is treating Bitcoin as a supervisory variable. This is harder and requires broad bank mapping.

Multiple banks would need to show material, measurable Bitcoin-linked profit-and-loss sensitivity across quarters, like custody, lending to ecosystem participants, derivatives, and prime-like financing.

The Fed would need to build and validate supervisory models that, in a repeatable way, translate Bitcoin paths into losses, fee income, and liquidity stress.

Tier 3 is an exploratory Bitcoin scenario. This becomes possible during a transparency era like the current one. The Fed could publish an exploratory sensitivity analysis alongside the main test, exploring crypto-TradFi spillovers without embedding Bitcoin in binding capital requirements.

The current 2026 transparency posture makes this more institutionally feasible than it used to be.

The governance counterweight

Bank trade groups generally argue the Fed should preserve discretion in scenario design and ensure transparency requirements don't create distortions or mechanical capital impacts divorced from real risk.

The Fed itself has noted that adding “salient risks” via scenarios can reduce the ability to test other emerging risks and increase the burden.

That's the sober institutional reason Bitcoin won't appear in stress tests until exposures justify it: not because the Fed opposes Bitcoin, but because scenario design is a capital-allocation tool with real consequences for bank behavior.

The question isn't whether the Fed will “adopt Bitcoin.” The question is whether Bitcoin exposures at regulated banks will grow large enough and become embedded enough in trading, custody, and intermediation activities that the Fed can no longer model bank resilience without modeling Bitcoin shocks.

If that happens, Bitcoin won't enter stress tests as a policy statement. It will enter because the Fed ran out of ways to ignore it.

The post Bitcoin is about to hit the Federal Reserve’s 2026 stress tests, creating a massive capital risk for regulated banks appeared first on CryptoSlate.

A single wallet on Hyperliquid holds a long position worth roughly $649.6 million in Ethereum (ETH), with 223,340 ETH entered at around $3,161.85, with a liquidation estimate near $2,268.37.

As of press time, ETH traded around $2,908.30, and the liquidation threshold sits about 22% below that. This is far enough to avoid imminent danger but close enough to matter if volatility accelerates.

The position has already bled roughly $56.6 million in unrealized losses and another $6.79 million in funding costs, leaving a cushion of about $129.9 million before forced closure.

The same wallet made over $100 million during October's crypto selloff, riding two Bitcoin (BTC) shorts and an ETH long opened in early October to combined profits of $101.6 million across positions that lasted between 12 and 190 hours.

That track record makes the current drawdown notable: not because the trader lacks skill, but because the size of the position and the mechanics of cross-margin liquidation on Hyperliquid create pressure that could ripple beyond a single account.

How cross margin changes the calculation

Hyperliquid's cross-margin system means the liquidation price displayed on the position isn't fixed. It shifts as collateral changes, funding payments accumulate, and unrealized profit or loss accrues across other positions in the account.

The platform's documentation states that, for cross-margin, the liquidation price is independent of the leverage setting. As a result, changing leverage reallocates the amount of collateral backing each position without altering the maintenance margin threshold.

This matters because “liq price” on cross margin is a moving target, not a countdown timer.

The wallet's $129.9 million margin provides breathing room. Still, funding rates on ETH perpetuals can swing quickly during volatility, and any correlated losses in other positions would reduce account-level equity, pulling the liquidation price closer to spot.

What happens when liquidations hit

Hyperliquid sends most liquidations directly to the order book, meaning the forced position closure happens within the perpetual market first rather than dumping spot ETH.

The platform's liquidator vault and HLP backstop absorb trades that fall below maintenance margin thresholds.

If conditions deteriorate to the point that even the backstop can't cover losses, Hyperliquid's auto-deleveraging mechanism kicks in, closing out opposing positions to prevent bad debt.

The spillover to the spot usually arrives indirectly. Arbitrageurs and market makers respond to dislocations between perpetual and spot prices, hedging flows accelerate, and basis spreads widen as leverage unwinds.

That chain of reactions can amplify downward pressure, especially if multiple large positions cluster near similar liquidation levels and trigger cascade effects.

Hyperliquid adjusted margin requirements after a March 2025 episode in which a roughly $200 million ETH long liquidation led to a $4 million loss for the HLP backstop.

The platform responded by introducing a 20% minimum collateral requirement in certain scenarios. That precedent shows Hyperliquid will intervene when large liquidations threaten system stability, but it also demonstrates that backstop losses are possible.

Where leverage clusters

CoinGlass liquidation heatmaps offer a second view of where cascade risk concentrates.

The heatmaps are derived from trading volume, leverage usage, and related data, showing relative-intensity zones where liquidations could cluster if price moves through certain thresholds.

CoinGlass explicitly notes that the maps are relative indicators rather than deterministic forecasts, and that actual liquidation amounts may differ from the displayed levels.

For ETH, recent heatmap data suggests notable leverage clusters between $2,800 and $2,600, with another concentration near $2,400. The $2,268 liquidation threshold for the $650 million long sits below those clusters, meaning it wouldn't necessarily trigger in isolation.

However, if a broader deleveraging wave pushes ETH through the $2,400 zone, that wallet's position would be swept into the cascade.

The 22% downside to liquidation doesn't imply imminent failure, but it does place the position within range of historical ETH volatility. ETH has printed 20%-plus drawdowns multiple times over the past two years, often during correlated risk-off moves across equities and crypto.

The wallet's October success came from timing macro reversals and exiting before momentum flipped.

The current ETH long, by contrast, has been open long enough to accumulate significant negative carry-through funding and mark-to-market losses. The position now depends on ETH reversing course before funding drains more equity or volatility forces a margin call.

The post The “insider wallet” that made over $100M on October tariff trade in threat of liquidation if one asset continues to dip appeared first on CryptoSlate.

https://ambcrypto.com/feed/

Crypto custody firm BitGo has raised $212.8 million in its U.S. IPO, signalling continued investor demand for regulated digital asset infrastructure.

Crypto custody firm BitGo has raised $212.8 million in its U.S. IPO, signalling continued investor demand for regulated digital asset infrastructure. Payments and security on the network are expanding.

Payments and security on the network are expanding.https://beincrypto.com/feed/

Flipper has released an upgraded version of its AI-driven DEX aggregator, designed to simplify token swaps and order management on Solana. The protocol aggregates liquidity from Raydium, Whirlpool (Orca), and Meteora, with plans to expand to additional exchanges.

Smart swaps are now live: the system analyzes pools and selects the most efficient route, including multi-hop paths through intermediate tokens, to ensure the best rates. All this happens within a single transaction, with built-in slippage protection and WSOL support.

Limit orders include take profit (to lock in gains up to 1000%) and stop loss (to minimize losses during price drops). Orders can be combined with swaps, canceled, or set to expire, with support for Token 2022 and xstocks for confidential transactions.

The AI assistant provides market forecasts — analyzing trends, liquidity, volatility, and risk — and suggests optimal entry and exit points. Funds are stored in automated vaults, never held by the platform itself. Security is reinforced through route validation, audits, and event monitoring.

The protocol is deployed on mainnet at: fLpRcgQSJxKeeUOgbb6M7bWe1iyYQbahjoGXGWwr4HgHit

Testing has covered swaps, orders, and routing performance.

What’s Next for Flipper?

Future updates will connect additional liquidity sources, including Saber, Orca TokenSwap, OpenBook, Phoenix, and Raydium CLMM. Planned improvements include automatic order execution via oracles, enhanced AI sentiment analysis, gas optimization, and API integrations for developers.

The protocol is designed for:

• Users seeking the best exchange rates without manual searching

• Traders who rely on automated orders and AI analytics

• Developers integrating flexible adapters into DeFi systems

About the Project

Flipper is an AI-powered DEX aggregator built on the Solana blockchain to simplify DeFi trading. The platform unites liquidity from multiple exchanges, offering smart routing, limit orders (take profit & stop loss), an AI assistant for market analysis and forecasts, and support for xstocks confidential tokens via Token 2022.

All operations are non-custodial — funds remain in the user’s wallet. The system focuses on security, slippage protection, and MEV-attack mitigation.

The project is evolving iteratively, guided by community feedback, with plans for expanded integrations and new features.

Join the community on Telegram: @flipper_dex_chat

Start trading: https://app.flpp.io/

The post Flipper Launches Updated Trading Protocol on Solana appeared first on BeInCrypto.

Ethereum’s price recently suffered a sharp decline, briefly dropping below the $3,000 level during heightened market volatility. ETH fell to an intraday low near $2,870 before stabilizing.

While the move unsettled short-term traders, BlackRock argues Ethereum’s long-term value lies beyond price action, rooted in its central role in tokenization.

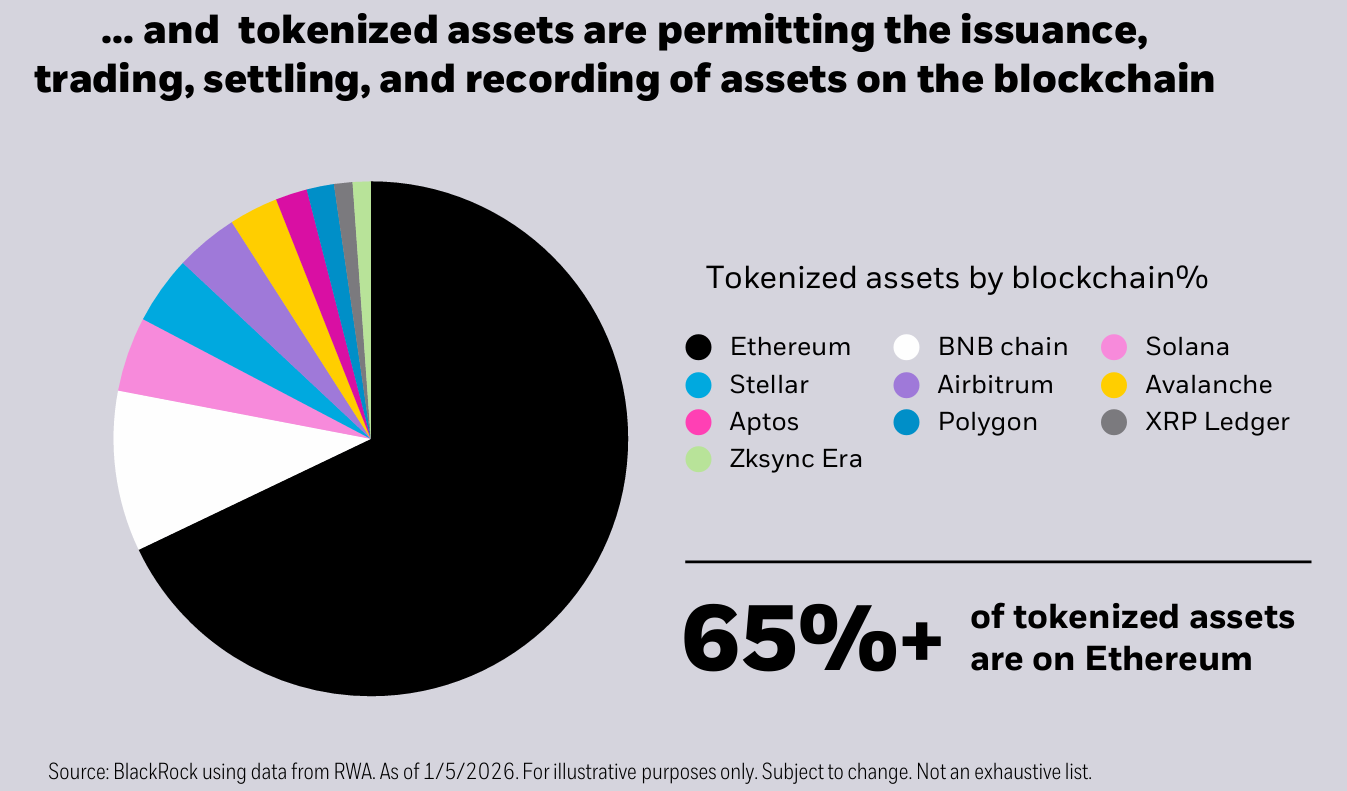

Ethereum’s Tokenized Future Looks Bright

BlackRock’s Thematic Outlook 2026 describes Ethereum as the “toll road” for tokenization. The comparison highlights Ethereum’s role as essential infrastructure rather than a speculative asset. As more financial instruments migrate on-chain, networks facilitating issuance, settlement, and compliance stand to benefit structurally.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

The report notes that about 65% of all tokenized assets currently reside on Ethereum. This dominance gives the network a near-monopolistic position in tokenization markets. Growth in stablecoin usage already reflects tokenization in practice. As adoption expands, Ethereum is positioned to capture consistent network demand.

Ethereum Is Already Dominating The RWA Market

The real-world asset market reinforces this narrative. Tokenized RWAs recently reached a new all-time high of roughly $21 billion in total value locked. Ethereum alone accounts for approximately $11.6 billion of that figure, representing about 55% of the entire RWA market.

Such concentration suggests Ethereum’s advantage is compounding rather than eroding. Issuers and institutions tend to build where liquidity, tooling, and security already exist. This dynamic strengthens network effects. Investors appear to be recognizing that Ethereum’s leadership in RWAs could deepen as tokenization scales globally.

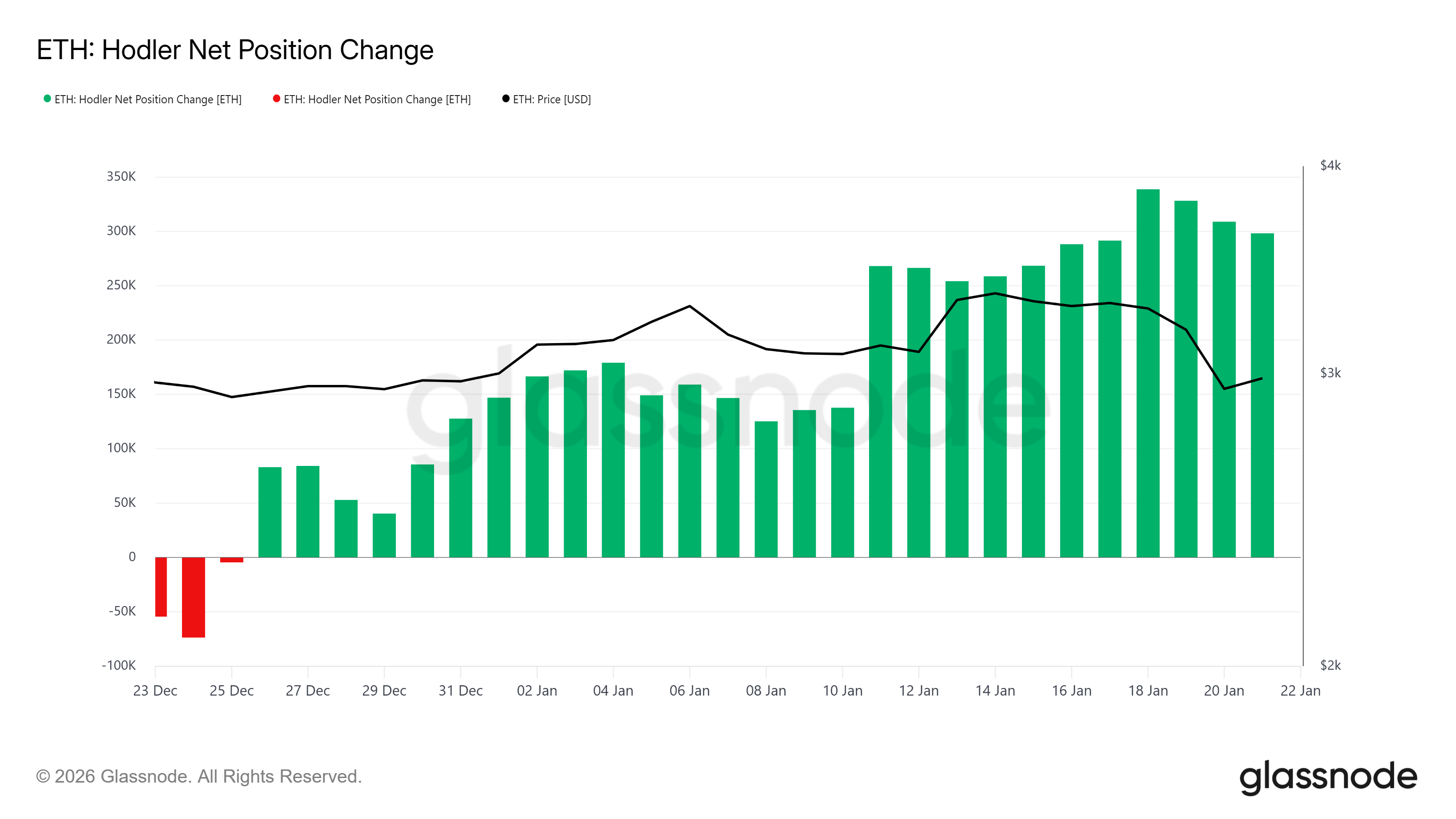

Long-term holder behavior aligns with this structural outlook. On-chain data shows Ethereum’s net position change turning positive among long-term holders. Selling pressure from this group has faded after weeks of distribution. Accumulation has replaced selling, signaling renewed conviction.

Long-term holders often respond to fundamental developments rather than short-term price swings. Their shift toward buying suggests confidence in Ethereum’s role within financial infrastructure. Reduced sell-side pressure from these holders may help ETH regain stability and support a recovery above key psychological levels.

ETH Price Recovery Has Some Time

Ethereum trades near $2,997 at the time of writing after rebounding from recent lows around $2,870. Price now sits just below the $3,000 threshold, a level closely watched by traders. Holding this zone suggests downside momentum is weakening as buyers re-enter.

BlackRock’s acknowledgment of Ethereum’s tokenization role could act as a sentiment catalyst. Improved confidence may help ETH reclaim $3,085 as resistance. A sustained move higher could extend gains toward $3,188, allowing Ethereum to recover a meaningful portion of its recent losses.

Downside risk appears limited under current conditions. A bearish scenario would require ETH to fall below $2,925 or $2,885. Losing those supports could expose Ethereum to a drop to $2,796. For now, improving macro signals and long-term accumulation reduce the likelihood of such a move.

The post BlackRock Names Ethereum The “Toll Road” To Tokenization; Here’s What It Means appeared first on BeInCrypto.

https://cryptonewsz.com/feed/

https://www.newsbtc.com/feed/

Bitwise’s take on the final months of 2025 reads like a careful, hopeful note rather than a loud market call. Momentum on the chains rose even as prices stalled, and that gap is exactly what has traders talking. Some think it marks a bottom. Others say it’s too soon to be sure.

Crypto: On-Chain Activity Surges

According to Bitwise, Ethereum activity and layer-two transactions climbed to new highs, and decentralized trading grew markedly. Stablecoin supplies also swelled, with the total market cap passing the $300 billion mark in Q4.

Reports note that decentralized exchange volumes at times matched or exceeded those of major centralized venues. These are hard numbers. They are signs that real use and liquidity are expanding under the surface.

The latest Bitwise Crypto Market Review just dropped—and it’s the most important one we’ve ever published.

Why? Because it shows a tension in crypto markets that has historically signaled a bear-market bottom (see Q1 2023).

Receipts: During Q4 2025…

– ETH’s price fell 29% ……

— Bitwise (@BitwiseInvest) January 21, 2026

Why Prices Have Lagged

Bitwise’s chief investment officer, Matt Hougan, compared this setup to early 2023 when prices trailed rising fundamentals before a significant rebound took hold over the following two years.

The comparison makes sense on paper. Price can be stubborn. Market psychology often lags behind on-chain realities, and traders sometimes wait for a clearer macro story before committing capital.

Fundstrat’s Tom Lee offers a counterpoint, saying the year could be bumpy until late, with tariffs and political tensions weighing on risk appetite. That view keeps many investors cautious.

According to market data, flows into stablecoins accelerated, and fund inflows to crypto firms outpaced several other sectors in the stock market. DeFi use was no longer a niche metric; it was central to the Q4 narrative.

“That’s the type of divergence you get at the bottom of bear markets, when sentiment is down but fundamentals are up,” Hougan said.

Some infrastructure firms reported rising revenues. At the same time, trading volumes remained muted compared with the peaks seen earlier, which helps explain the mismatch between on-chain strength and sideways price action.

Why This Might Matter For 2026Bitwise highlighted 10 broad indicators it sees as health signs for the market, ranging from transaction counts to custody and fee trends. Progress on regulatory clarity was also flagged.

Reports say the Clarity Act could change how stablecoins are treated in the US, and a new US Federal Reserve chair could shift policy in ways that matter for risk assets.

Bitwise sees Q4 as a quiet period where things were improving behind the scenes, even if prices didn’t show it. The firm says this kind of gap between price and activity has happened before big rebounds. It doesn’t mean a rally will happen right away, but the market could be setting itself up for a stronger year ahead.

Featured image from Unsplash, chart from TradingView

Bitcoin’s role in the global financial system remains widely misunderstood, even at the highest levels of policy and finance. That disconnect surfaced during a major international forum, prompting a pointed clarification from a Coinbase executive. The moment centered on a fundamental question with growing relevance: what truly separates Bitcoin from central banks?

Bitcoin’s Structural Design Sets It Apart – Coinbase Executive

During the World Economic Forum in Davos, where global policymakers and financial leaders were debating the future of money and tokenization, Brian Armstrong, CEO of Coinbase, responded to remarks made by François Villeroy de Galhau, Governor of the Banque de France, who argued that central banks deserve greater trust than Bitcoin because they operate under democratic mandates and institutional oversight.

Armstrong’s response focused on how Bitcoin is designed. Bitcoin operates as a decentralized protocol with no issuing authority, no governing committee, and no single entity capable of altering its monetary rules. Its supply is fixed, its issuance is algorithmic, and its operation depends on a distributed network of participants rather than institutional oversight. This design makes Bitcoin structurally independent in a way no central bank can replicate.

By contrast, central banks sit at the top of national monetary systems. They control currency issuance, influence interest rates, and adjust monetary policy in response to political and economic pressures. Even when described as “independent,” they remain tightly connected to governments and fiscal policy. Armstrong highlighted that this link introduces discretion, policy shifts, and long-term currency debasement through money creation—a vulnerability Bitcoin was explicitly built to avoid.

This distinction becomes especially relevant during periods of aggressive deficit spending. Because Bitcoin’s supply cannot be expanded, it functions as a constraint rather than a tool. In Armstrong’s view, this makes Bitcoin a direct counterweight to systems where new money can be introduced at will, gradually reducing purchasing power over time. That structural constraint is the foundation of Bitcoin’s appeal as a hedge during periods of uncertainty.

Trust, Accountability, And Individual Choice

The exchange also exposed a deeper disagreement about how trust is formed. Villeroy de Galhau emphasized trust in central banks as institutions backed by legal authority and democratic systems. Armstrong countered by reframing trust as something derived from transparency and verifiability rather than institutional reputation.

Armstrong further positioned Bitcoin as an accountability mechanism. Because its supply cannot be adjusted to accommodate government spending, it imposes discipline by design. In this sense, Bitcoin functions less as a policy tool and more as a constraint—similar to how gold historically limited monetary excess. This characteristic has driven its growing perception as a store of value during times of economic uncertainty.

Importantly, Armstrong did not frame the relationship between Bitcoin and fiat currencies as a zero-sum battle. Instead, he described it as a healthy competition that leaves the ultimate decision with individuals. Users can choose between systems: one based on institutional control and policy flexibility, and another based on fixed rules and decentralization.